Nov

13

Analogy of the Day, from anonymous

November 13, 2012 | Leave a Comment

Mumboism is to trade flexionics as Petraeus' wife is to Petraeus?

Available ex-ante mumboism mined trading signals is useful even to anti-mumboists?

Nov

8

Romney’s Campaign, from Dan Grossman

November 8, 2012 | 1 Comment

I voted for Gary Johnson, but come on, Romney didn't commit all kinds of blunders. He ran a decent, energetic campaign. Far better than McCain or Dole or probably even the Bushes. It took Romney until late in the campaign to hit his stride, but by the end he sounded far better on the stump than did Obama. And of course he won the debates.

I voted for Gary Johnson, but come on, Romney didn't commit all kinds of blunders. He ran a decent, energetic campaign. Far better than McCain or Dole or probably even the Bushes. It took Romney until late in the campaign to hit his stride, but by the end he sounded far better on the stump than did Obama. And of course he won the debates.

But every time Romney opened his mouth, the press crucified him for a blunder. When he made a very mild and presumably knowledgeable comment in London on preparations for the Olympics, the nationalist, socialist English press cried he had insulted their country and the US press piled on that his foreign trip was a disaster. When he happened to mention being supplied with binders of women, it was absolutely the worst, most anti-women comment anyone could every make. When he questioned the apologetic US reaction to the Libyan riots, the press said he was politicizing a tragedy. Meanwhile the President could ignore pleas to send support for our diplomats, resulting in the murder of our ambassador and shorted-handed former Navy Seal security team, and the press was totally uninterested in looking into or even reporting the matter.

But the real trouble was structural, as Vic pointed out. It is now, and certainly will be in the future, impossible for a Republican presidential candidate to win.

Based on exit polls, Romney won 58% of the White vote, Trouble for him was that Obama won 93% of the Black vote, 67% of the Hispanic vote, and 75% of the Asian vote. BTW Romney also won 60% of the married vote of all races — an incredible figure never mentioned in the blizzard of commentary about Romney's "war on women." These are figures that would have resulted in a landslide for Eisenhower or Kennedy or Reagan.

All in all, Romney won the traditional American vote. What Obama won could somewhat unfairly but not totally unreasonably be characterized as the anti-American vote — the alienated minorities, those on the dole given Obamaphones and such, the capitalist cronies, the lefties and naive young, the Hollywood dabblers, the academics and a large chunk of the intellectuals.

Nov

5

The 1% and Big Government, from Omid Malekan

November 5, 2012 | 1 Comment

Today's little relief mission to the hard hit Rockaways area was very telling. Fema and NYC relief crews were nowhere to be seen, and everything was being run by a local city councilman and an army of volunteers.

Today's little relief mission to the hard hit Rockaways area was very telling. Fema and NYC relief crews were nowhere to be seen, and everything was being run by a local city councilman and an army of volunteers.

The folks who run the public library down there had decided to turn it into a makeshift relief center, and we were able to get them a much needed generator and some other supplies. The most relief was provided by millionaire hedge fund manager Roy Niederhoffer, who in 1 day managed to put together an army of people to bring down cars and even a 26 foot u-haul truck with enough pre-sorted food to support 100 families of 4 people for days. Note he didn't just write a check, but he actually quarterbacked the entire operation (for the second day in a row).

Oh, and when we were leaving trucks for the New York Daily News (owned by billionaire Mort Zuckerberg) rolled up to drop off much needed blankets.

I wish Mitt Romney had written a check for $10 million bucks and called up his other wealthy CEO buddies who run companies like Costco or Home Depot and had them divert a bunch of trucks down to the hart hit areas. That would have been the best answer to the constant ridicule by liberals that he's just too darn rich.

Mick Tierney writes:

Just to provide a little balance to the "1% big government" post, here's a story I heard just this morning.

Our 73 year-old pastor takes three weeks off every Spring and Fall to re-visit small churches in Virginia, West Virginia, and North Carolina (a routine he established about 17 years ago). He takes another four weeks each summer for a church/school/medical facility he has established in Haiti (a project begun about 20 years ago).

This year he was asked to make a first visit to a small church (35) in the vicinity of the SETI Institute — obviously in the middle of Nowhere, WV. While there he and his wife were invited to dinner by one of the church members. After discussing various local issues, he asked if his hosts had ever met any of the SETI staff.

They replied that they had receive one visit. Late one afternoon a gentleman knocked at their door and announced that he had a heating blanket for them. They thanked him kindly but refused as they already had one.

He informed them that he was aware of this, but that their current blanket had developed a short. They checked and discovered he was right - without explanation he gave them the blanket and left.

Now you can return to the possibilities of election day computer hacking.

Nov

2

How to Tell if You Are the Target of Bullies, from anonymous

November 2, 2012 | 3 Comments

Bullies, as adults, generally abuse their authority. If you stand for excellence and have some success you will attract the attention of bullies. It has been my experience that bullies hate a good success story but despise the successful more for the attention and admiration of others than their success. The heroes of myths, Bible stories, and legends are often victims of the drummed up accusations of bullies. Apparently, most ancient cultures were gravely concerned with bullies in everyday adult life.

Bullies, as adults, generally abuse their authority. If you stand for excellence and have some success you will attract the attention of bullies. It has been my experience that bullies hate a good success story but despise the successful more for the attention and admiration of others than their success. The heroes of myths, Bible stories, and legends are often victims of the drummed up accusations of bullies. Apparently, most ancient cultures were gravely concerned with bullies in everyday adult life.

Here are several tells that a bully's complaint against you is a witch hunt rather than legitimate complaint:

1. You are singled out after publicity.

2. Many interviews are held and are fishing expeditions of your weaknesses.

3. In these interviews, there are two types of witnesses, those that routinely support the bully and those that are intimidated and gladly rat out their neighbor to get the bully to leave their doorstep.

4. The interviews are one sided.

(It is widely known that the bully and their cohorts have immunity for much more corruption. Interrogations do not happen for them. Romance, money and power are often a triangular core. The bully often is a mistress of the ruler in the stories)

5. The bully often will intimidate and harasses the friends and family who would give the moral support to the victim.

6. It makes no financial sense for the bully to waste so many resources pointing out your minor faults.

It makes sense to do whatever it takes to rid yourself of an organization that allows one to be bullied.

I wonder if the moral implication of the ancient stories is correct, that rampant bullying is a subtle sign of an empire or emperors impending sudden chaotic demise…

Nov

1

NYC Junto, from Victor Niederhoffer

November 1, 2012 | 1 Comment

The NYC Junto will still be meeting at the usual place, the Mechanics Institute, 20 West 44th Street New York, NY, at 7pm Thursday November 1, 2012 with Mr. Greg Rehmke delivering a talk on evolution of economic behavior.

The NYC Junto will still be meeting at the usual place, the Mechanics Institute, 20 West 44th Street New York, NY, at 7pm Thursday November 1, 2012 with Mr. Greg Rehmke delivering a talk on evolution of economic behavior.

Hope to see you all there!

Sincerely,

Victor Niederhoffer and Dailyspec

Nov

1

Flood Insurance, from Alan Millhone

November 1, 2012 | 1 Comment

I wonder how many homes are not covered due to lack of flood insurance or not being able to get coverage on Jersey Shores etc. ?

I wonder how many homes are not covered due to lack of flood insurance or not being able to get coverage on Jersey Shores etc. ?

Anonymous writes:

Flood insurance is easy to get. There is a "basic" version and an add-on. The basic version on our Jersey Seashore house cost $20 per $100k of coverage and the add-on was an extra $47, PER YEAR. It is subsidized by the Federal government, which is why it is so cheap. Only an idiot would not have it. And yes, there are idiots out there. If you are in a flood-prone area, you want as much insurance as you can get.

If you are not in the defined "flood plain" it can be difficult to get flood insurance because the Feds do not subsidize it. We also had a lakefront property that somehow managed to be out of the designated flood plain. Coverage for that property was about 3 times that of the beach house. And that property did have some minor flood damage, although I chose not to submit it.

Bill Herrmann adds:

Federally subsidized flood insurance is a very good example of government incentives pushing the economy in the wrong direction. Just as “Too Big to Fail” encourages some institutions to take larger risks then they would otherwise, federal subsidized flood insurance encourages building in the flood plain. (Which is generally not a good idea.)

Oct

18

Truck-care, from anonymous

October 18, 2012 | Leave a Comment

I took my aging beloved 100k plus mile truck to her certified primary care provider (dealer) recently and they identified $5000 worth necessary procedures which they printed in a very nice report. With same report I got a second opinion from a smaller family run care provider (garage) who I trust, at one fifth the cost. Since I am paying this is out of pocket I opted for the cheaper one. If another party was paying this for me I would have been indifferent.

I took my aging beloved 100k plus mile truck to her certified primary care provider (dealer) recently and they identified $5000 worth necessary procedures which they printed in a very nice report. With same report I got a second opinion from a smaller family run care provider (garage) who I trust, at one fifth the cost. Since I am paying this is out of pocket I opted for the cheaper one. If another party was paying this for me I would have been indifferent.

anonymous comments:

For those going on Medicare, the death panels are not panels but cost containment measures put into place.

What has changed treatment the most in the last few year is "adverse" reaction to treatment. The Doctors have to pay for treatment out of their own pockets if after initial treatment, the patient has an adverse response within set time periods based on the condition.

The doctor not wanting to risk the lose of income and time, therefore will only accept the most physically fit for hip replacement or even cardio operations.

"He is a smoker that overweight, what does he expect if his hip goes out…we don't guarantee miracles." is a typical response felt if not said.

One wonders if this will actually cause the working poor and lower class to receive less treatment than before, at least at their most critical point in their lives, as these are often are the people with the highest probability of "adverse events".

an anonymous person comments:

Well, what are some thoughts around the notion that if individual people are more financially responsible for their own health care, they will take better care of themselves?

anonymous responds:

This I believe is the most insidious part, most people that get medicare trust the government way too much to question that they will be getting less care not more, under a medicare plan. Handouts are seen as "free money" without consideration for their second order effects on incentives and motivations.

This is especially true amongst the working poor class in my opinion. It will be generation X and Y before the "lesson" (they need to take better care of themselves) will be accepted. By then either medicare will be cut so far back or rationed to a point where by the time you are 65, everyone, if they have half a brain, becomes a "Medicare conservative" because they have seen Government work.

Oct

3

October 4th Junto, from Dailyspeculations

October 3, 2012 | 1 Comment

Tomorrow night, Thursday, October 4th, is the Junto.

It will be held at the General Society Library,

on 20 West 44 St., between 5th and 6th Aves.

Gary Hoover will be giving a talk called Think Like An Entrepreneur.

The talk will begin promptly at 8pm but we will socialize beginning at 7pm.

All are welcome.

From Victor and Dailyspeculations

Oct

2

The Value of One Vote, from Pete Earle

October 2, 2012 | Leave a Comment

If the average welfare recipient receives something on the order of $43,000/yr, and the average American's salary is $46,000/yr, the personal discount rate is approximately 6.52%.

If the average welfare recipient receives something on the order of $43,000/yr, and the average American's salary is $46,000/yr, the personal discount rate is approximately 6.52%.

There's no initial capital laid out to get on welfare, just a lot of forms and standing in line; But many welfare recipients don't really forgo income to stand in line, so I'm using $0.

Given that the Presidential term is 4 years, the total welfare benefit over those 4 years is $172,000; applying the simple NPV, is a single vote "worth" approximately $156K?

Gary Rogan writes:

A single vote, for some specific person, is worth ANY amount of money to that person if they aren't the ones paying for it. The now violent riots in Spain and the free phone lady and the $16 trillion deficit are all consequences of that one simple fact.

Sep

28

The Value of a Bachelor’s Degree, from anonymous

September 28, 2012 | 7 Comments

She had wanted to go to Wesleyan. It had everything she was after–small liberal arts school with lots of on campus activities, a strong record of graduate/work placements, small size, and a school where parties were not the rule of the day. Oh, and that it was on the other coast, away from my wife and me, only increased her interest in the school. She was also looking at Wellesley, Colby, Bowdoin, Carleton, Grinnell, and so on. Some public ivies too–U Wisconsin Madison, U Washington, and even some of the U of Californias, though the latter is her safety school.

The problem with the liberal arts colleges is that they now cost a fortune. Generally north of $45K a year and often north of $50K. The situation with the ivies isn't much different–they also cost a small fortune. The out-of-state tuitions for many universities (including the public ivies) are in the mid-20K range, and the chances of finishing in 4 years when attending them is diminishing by the semester. Needing to attend a U of Cal for 6 years to finish a major used to be a rarity. Not anymore. And there is no reason to think the status quo will improve any time soon. Here in California, the system developed by Pat Brown (the current governor's father) had the U of California system, the Cal State system, and then regional community college system. Not only are these systems struggling to find some way of increasing their capacity, but they are doing so at a time when the state government is cutting funding for education throughout the state, including these three post-secondary systems. This problem is not limited to California. In the SUNY system, all tuition goes to Albany, and the state legislature decides how much goes back to the individual campuses, rather than looking at each campus as a P&L center (as U of C campuses do).

Why bring all this up? My daughter is now contending with the question of what's the best value for getting a college education rather than what's the "perfect place" for her. So far, so good. This was what we discussed last night at dinner, and it got me thinking about the post-secondary education system here in the US. At the college level, that system has been in place for three centuries or so. At the graduate/professional level, the current system came into being during the mid-to-late 1800s. The problem is that with the current levels of tuition, the cost of a baccalaureate is rapidly becoming (if not already there) out of reach for much of the middle class population. Using loans is rapidly becoming untenable in the face of college grads unable to find jobs and one-in-twelve of the workforce unemployed. (I won't get into the loan fiasco as regards professional grads–the average medical student having debt north of $150K and for more than a third, it's in excess of $200K.) For many of the existing loans, it seems likely that someone other than the college grad will be left paying the bill. That's debt of about $1.2 trillion at risk. The bottom line is that the current system is rapidly becoming–if it is not already–unsustainable.

The question must be asked about what is the value of a bachelor's degree. I ask the question because it is becoming easy to have access online to some of the outstanding courses available at many of America's premiere universities. Will a degree really have much value when an employer is interested in what you have learned somewhere–online or in person? It used to be that the only way to obtain the knowledge was to attend a college or university in a degree program. The degree was a proxy for knowledge. But there are now other sources for obtaining that knowledge–does spending the money on a college degree make sense any longer?

The situation is even more daunting when you consider that during the mid-1970s, when I went to Johns Hopkins, tuition was about $3K a year. That was also the price of a Chevy Nova car at that time. A Chevy Spark now costs under $15K, and has a MSRP of $12K and change. Tuition at Johns Hopkins today? $50K.

All those contributions to one's alma mater are prolonging the day of reckoning for a system that will need to undergo extensive reform, and that reform will need to accommodate other forms of education rather than only in-person class attendance. Western Governor's University (www.wgu.edu) may be one example, but insofar as it is built around actual degrees, I'm not sure that it's the only type of solution.

An educated workforce is a major prerequisite for a competitive United States, yet the education system is in the middle of a crisis about which there is precious little discussion. That has to change.

Richard Owen writes:

Education is becoming the quintessential branded luxury, taking a commodity input and stamping it with a brand.

Markets are made at the margins: the price driver has been (i) the rising share of wealth located abroad and (ii) the higher percentage of production available to the best paid domestic workers. The West is importing the GINI ratio of the Emerging Markets when it comes to high end property, education, etc.

Take British public schools: fees are now $45k/yr for the full school life, rather than just a terminal three years at college. For three children that's $135k/yr post-tax wage dollars. 7% of the UK is privately educated historically, yet the former figure is well into the 1% income range. Whats made up the marginal demand? Wealthy foreigners with untrammeled, untaxed, EM boom dollars. London is undergoing a reverse colonization. Hence in some bijou streets in the capital, residential is up 40% in two years, (having fallen not at all during the crisis, so that's not a bounce off the lows).

Carder Dimitroff adds:

I have two daughters in their 20s. Both have Ivy-league degrees. Frankly, I'm not sure Ivy matters.

There are wonderful state and private colleges. Most decent universities offer inquiring minds incredible opportunities. If a student is looking to learn and grow, most "average" universities can dish out more than most students can handle.

A good example is my cousin's daughter. She attended a low profile public college in Florida. She went in with the attitude of learning and developing. She and several of her classmates became Fulbright Scholars. Now she is Ph.D. candidate at Duke.

If you look at Ph.D. candidates at the nation's leading research institutions, you may notice most of them never attended Harvard, Yale or Princeton. The same can be said for many business, political and military leaders.

Each school has its own culture. In my opinion, a key to a parent's success is matching the college with the student's personality. If the student love the place from day one, all is good.

Sep

27

The Diaoyu/Senkaku Islands Dispute, from Craig Mee

September 27, 2012 | Leave a Comment

For anyone who is interested…it seems this event involves quite a bit of he said she said, with some good old miscommunications, and selected curve fitting thrown in for good measure.

For anyone who is interested…it seems this event involves quite a bit of he said she said, with some good old miscommunications, and selected curve fitting thrown in for good measure.

"The Inconvenient Truth Behind the Diaoyu/Senkaku Islands" :

My research of over 40 official Meiji period documents unearthed from the Japanese National Archives, Diplomatic Records Office, and National Institute for Defense Studies Library clearly demonstrates that the Meiji government acknowledged Chinese ownership of the islands back in 1885.

Anonymous adds:

In the current drama of this event, the very ownership of the island, though seemingly at the core, is actually a very secondary issue. What is worth watching are the following.

1) In a country where there is zero tolerance for demonstrations and even public gatherings, how come there were suddenly so many demonstrators on the streets?

2) Why is there is so much resemblance between the main slogans, banners and pictures? Who made them?

3) During some demonstrations in front of Japanese embassies, why weren't passersbys allowed to join in? Who were those allowed?

4) Of the people leading most of the violence in the streets, how come many are short-haired, tan-faced, strong-muscled, young and well-coordinated? How come they had no fear of the police when doing the violence?

5) At a time when Bo Xilai is being judged and when the Party leaders are fighting in closed doors for who will take charge in the future, is all this just a coincidence?

Sep

21

What the Hell is Happening in the World, from Peter Tep

September 21, 2012 | 1 Comment

Afternoon esteemed (daily)specs,

I haven't done any research on the data and the numbers but even a fool like me can observe world wide stock markets, look at the release of data of economic indicators and see that something fishy is going on. I'm referring particularly to the Australian market and the release of the Chinese PMI Manufacturing numbers, and the dropping of iron ore prices.

Ready to take notes…..

Sep

20

i got 104 points in scrabble, from Aubrey Niederhoffer

September 20, 2012 | 3 Comments

i almost beat your record points in scrabble with 104 points with disquiet. i scored bingo points and triple word score and double letter score on my u. love, aubrey

i almost beat your record points in scrabble with 104 points with disquiet. i scored bingo points and triple word score and double letter score on my u. love, aubrey

Uncle Roy replies:

WHOA!! Good work! I can't wait to play with you sometime. Here are some helpful tips:

Make sure to think about having even numbers of vowels and consonants in your rack after you play your word - so on your next rack you won't have all vowels or all consonants.

Leaving double letters in your rack for next turn is usually bad, except E which is only a little bad.

Try to score at least 60 points with each blank you get.

Learn all the 2 letter words (there aren't that many") and play words parallel to each other for extra points.

On your first move, if you don't score 18-20 (including the double word), pass and draw new tiles to try to get a bingo if you think you're close.

QI and ZA are very useful… and don't forget trying to use X on a triple in two directions which scores 52 at a minimum.

Think about what you "leave" in your rack for next move. If these letters are "good" letters like ETAION SHRDLU (the most common letters in English words), you're likely to draw some more of them, and then be able to make a bingo.

Unless you have two S's,don't use an S unless it is an above average score (for you) - usually average is about 20 so try to make S really count.

Good players get an average of 1.5 bingos per game. You should be getting at least an average of 1 for now… and 1.25 when you learn some more words as you get older.

At the end of the game, think whether the other player has a Q, Z or X. If they do, don't get let them play them by making ZA or QI or QAT.

Here is a list of two and three letter words which is worth learning.

I love you! See you very soon!!!!

Love Uncle Roy

AA AB AD AE AG AH AI AL AM AN AR AS AT AW AX AY BA BE BI BO BY DE DO ED EF EH EL EM EN ER ES ET EX FA GO HA HE HI HM HO ID IF IN IS IT JO KA LA LI LO MA ME MI MM MO MU MY NA NE NO NU OD OE OF OH OM ON OP OR OS OW OX OY PA PE PI RE SH SI SO TA TI TO UH UM UN UP US UT WE WO XI XU YA YE YO

——————————————————————————-

AAH AAL AAS ABA ABO ABS ABY ACE ACT ADD ADO ADS ADZ AFF AFT AGA AGE AGO AHA AID AIL AIM AIN AIR AIS AIT ALA ALB ALE ALL ALP ALS ALT AMA AMI AMP AMU ANA AND ANE ANI ANT ANY APE APT ARB ARC ARE ARF ARK ARM ARS ART ASH ASK ASP ASS ATE ATT AUK AVA AVE AVO AWA AWE AWL AWN AXE AYE AYS AZO

BAA BAD BAG BAH BAL BAM BAN BAP BAR BAS BAT BAY BED BEE BEG BEL BEN BET BEY BIB BID BIG BIN BIO BIS BIT BIZ BOA BOB BOD BOG BOO BOP BOS BOT BOW BOX BOY BRA BRO BRR BUB BUD BUG BUM BUN BUR BUS BUT BUY BYE BYS

CAB CAD CAM CAN CAP CAR CAT CAW CAY CEE CEL CEP CHI CIS COB COD COG COL CON COO COP COR COS COT COW COX COY COZ CRY CUB CUD CUE CUM CUP CUR CUT CWM

DAB DAD DAG DAH DAK DAL DAM DAP DAW DAY DEB DEE DEL DEN DEV DEW DEX DEY DIB DID DIE DIG DIM DIN DIP DIS DIT DOC DOE DOG DOL DOM DON DOR DOS DOT DOW DRY DUB DUD DUE DUG DUI DUN DUO DUP DYE

EAR EAT EAU EBB ECU EDH EEL EFF EFS EFT EGG EGO EKE ELD ELF ELK ELL ELM ELS EME EMF EMS EMU END ENG ENS EON ERA ERE ERG ERN ERR ERS ESS ETA ETH EVE EWE EYE

FAD FAG FAN FAR FAS FAT FAX FAY FED FEE FEH FEM FEN FER FET FEU FEW FEY FEZ FIB FID FIE FIG FIL FIN FIR FIT FIX FIZ FLU FLY FOB FOE FOG FOH FON FOP FOR FOU FOX FOY FRO FRY FUB FUD FUG FUN FUR

GAB GAD GAE GAG GAL GAM GAN GAP GAR GAS GAT GAY GED GEE GEL GEM GEN GET GEY GHI GIB GID GIE GIG GIN GIP GIT GNU GOA GOB GOD GOO GOR GOT GOX GOY GUL GUM GUN GUT GUV GUY GYM GYP

HAD HAE HAG HAH HAJ HAM HAO HAP HAS HAT HAW HAY HEH HEM HEN HEP HER HES HET HEW HEX HEY HIC HID HIE HIM HIN HIP HIS HIT HMM HOB HOD HOE HOG HON HOP HOT HOW HOY HUB HUE HUG HUH HUM HUN HUP HUT HYP

ICE ICH ICK ICY IDS IFF IFS ILK ILL IMP INK INN INS ION IRE IRK ISM ITS IVY

JAB JAG JAM JAR JAW JAY JEE JET JEU JEW JIB JIG JIN JOB JOE JOG JOT JOW JOY JUG JUN JUS JUT

KAB KAE KAF KAS KAT KAY KEA KEF KEG KEN KEP KEX KEY KHI KID KIF KIN KIP KIR KIT KOA KOB KOI KOP KOR KOS KUE

LAB LAC LAD LAG LAM LAP LAR LAS LAT LAV LAW LAX LAY LEA LED LEE LEG LEI LEK LET LEU LEV LEX LEY LEZ LIB LID LIE LIN LIP LIS LIT LOB LOG LOO LOP LOT LOW LOX LUG LUM LUV LUX LYE

MAC MAD MAE MAG MAN MAP MAR MAS MAT MAW MAX MAY MED MEL MEM MEN MET MEW MHO MIB MID MIG MIL MIM MIR MIS MIX MOA MOB MOC MOD MOG MOL MOM MON MOO MOP MOR MOS MOT MOW MUD MUG MUM MUN MUS MUT

NAB NAE NAG NAH NAM NAN NAP NAW NAY NEB NEE NET NEW NIB NIL NIM NIP NIT NIX NOB NOD NOG NOH NOM NOO NOR NOS NOT NOW NTH NUB NUN NUS NUT

OAF OAK OAR OAT OBE OBI OCA ODD ODE ODS OES OFF OFT OHM OHO OHS OIL OKA OKE OLD OLE OMS ONE ONS OOH OOT OPE OPS OPT ORA ORB ORC ORE ORS ORT OSE OUD OUR OUT OVA OWE OWL OWN OXO OXY

Sep

14

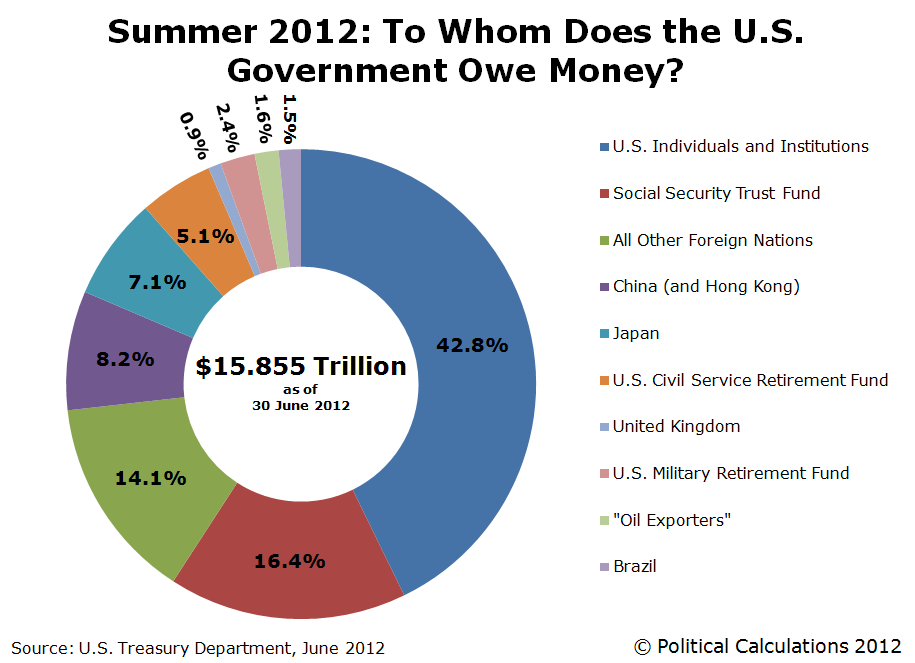

To Whom We Owe Much, from Carter Dimitroff

September 14, 2012 | Leave a Comment

I saw this chart on the esteemed Political Calculations web site. I notice the graph shows Japan, U.K. and Brazil holding some of our debt. How much debt does the US hold in other nations? If that debt were added, would a net debt picture look better?

Aug

31

Five Steps to Critical Thinking, from Bo Keely

August 31, 2012 | 3 Comments

Graham Greene wrote in The Quiet American, "Innocence is like a dumb leper who has lost his bell, wandering the world, meaning no harm."

Graham Greene wrote in The Quiet American, "Innocence is like a dumb leper who has lost his bell, wandering the world, meaning no harm."

For me at ten years the loss of innocence was trying to look out the Idaho living room window one evening with a light on inside and snow outside and I was surprised to see my reflection. For an instant there was confusion to who I was: the reflection or what it saw. I moved slightly to feel my body and determined thereon to be the person inside it.

A second mindful decision occurred twenty years later in a Michigan kitchen alone reading and a sentence from Carl Jung´s Memories, Dreams and Reflections. I looked up abruptly from archetypes as universal thoughts, symbols, or images having a large amount of unconscious power, and are shared… and it popped into my head from that point on to control my own thoughts. With willful effort I practiced the multiplication tables for ten minutes until the answer to 2 x 2 did not arrive until I caused it.

The third grave verdict that has shaped my life took place in a Michigan basement while reading Lewis Carroll's Through the Looking Glass where the page turned to the hideous monster poem ´Jabberwocky´. It´s written in mirror text, and it doesn't matter that I was reading in a coffin lined with electric blankets against the icy wind whooshing through the wall cracks, or that I was reading with an Edmond Scientific top grade mirror to reverse the text so the Jabberwocky came alive from left to right. Suddenly it dawned on me that I could turn the book upside down to cause the print to flow right to left and dispense with the mirror and monster. That´s how I´ve read hundreds of book to date, and the reason is to balance the body, eyes and brain to a more perfect symmetry to think better critically.

The fourth waypoint on the road to objective thinking was learning the chessmen and their moves that is as much a model as computers for the thought process.

The fifth rest stop is quotations that has become a lifelong study, and one of the best on critical thinking (that is attributed to no one) is "Critical thinking is thinking about your thinking while you're thinking in order to make your thinking better."

So in a long march to discovery of self along the best road I know how, in the first step I determined the body manufactures the thoughts; in the second that I could control the thoughts, on the third that the body must remain healthy and symmetrical to think better; on the fourth to use models to understand how the mind functions, and at the fifth to stand on other´s shoulders and pass along their advice.

Howard Zinn said, "History can come in handy. If you were born yesterday, with no knowledge of the past, you might easily accept whatever the government tells you. But knowing a bit of history- while it would not absolutely prove the government was lying in a given instance- might make you skeptical, lead you to ask questions, make it more likely that you would find out the truth." I might add this is not only true of government but of medicine, business, sports and anything else worth thinking about. The trick is to balance being skeptical and open. If you are only skeptical then no new ideas filter through to you and nothing new is learned. On the other hand, if you are open to the stretch of gullibility without an ounce of skepticism, then you won´t be able to distinguish the useful from the worthless.

The one skill everyone on the planet needs is the ability to think with objectivity. If we are prepared to think for ourselves, and learn how to do it well, there is little danger of becoming slaves to the ideas and values of others that is taking the earth and limiting self-potential. The list of core critical thinking skills includes observation, interpretation, analysis, comparison, evaluation and explanation

There are some training workouts: math, read Sherlock Holmes, logic riddles, and conversing with other critical thinkers. The number and direction of steps up from fuzzy thinking to a height of acute awareness varies from person to person. The ultimate step a quantum leap because no problem can be solved from the same level of consciousness that created it.

The adventure of critical thinking is the finding of self. You develop insights into what is and can be. I´ve found as much as possible, and the chase goes on.

Aug

31

Hurricane Isaac was Over Hyped, from Sam Marx

August 31, 2012 | 2 Comments

I've lived in southeast FL for 13 years and have gone through Category 2 & 1 hurricanes and a borderline Category 2/3 hurricane.

I've lived in southeast FL for 13 years and have gone through Category 2 & 1 hurricanes and a borderline Category 2/3 hurricane.

Category 2 can cause severe damage, Categories 3 & 4 can be disastrous.

With some preparation, Category 1 can be slept through.

Tropical storms can cause inconveniences such as road flooding but not much damage. Isaac has been a tropical storm and a Category 1 . As such it has been overhyped.

I suspect there was a political reason for this.

Jeff Watson writes:

At the beach, on the Gulf side, even a direct hit from a Cat 1 is frightening, and that's why we have to evacuate even from a 1. Storm surge at high tide is a sight to behold.

Sam Marx comments:

People who live at the water's edge should be prepared for hurricanes or shouldn't live there at all.

Outside of the water's edge, a Cat 1 hurricane does not do much damage , except, inland, for road flooding and damaging some houses built under the very old building codes.

Isaac became a Cat 1 over water and quickly dropped to a tropical storm over land. It should not have received the excessive media coverage it got.

Tradercraft adds:

Tell that to the half a million people in New Orleans who are sweltering without air conditioning right now, and their frozen foods spoiling (can be several hundred dollars worth of food), and unlikely to get power back for a week, Entergy announced. Not something one can easily sleep through.

Sam Marx writes:

I believe there never has been so much media coverage over a Cat 1 hurricane or tropical storm in the past as given to hurricane Isaac.

Gibbons Burke writes:

The fact that it followed a path very similar to that of Katrina, and actually hit New Orleans on the seventh anniversary of that storm had something to do with the attention it received. But the fact that it was early on slated to hit Tampa during the RNC convention certainly got the media's interest in the storm going, and once they get started on something, they often like to beat it to death.

Victor Niederhoffer writes:

The wisdom of Gann in predicting confusion and uncertainty and volatility during the anniversaries of vivid events is underlined.

Anton Johnson adds:

Tips for live coverage of minimal hurricanes.

1. Wear loose-fitting rain gear, preferably with an open hood to better accentuate wind gusts.

2. Stand with feet sholder width apart and knees bent. Lean torso and head into the direction of the wind for effect.

3. Use minimal wind-screen on microphone, speak loudly as if straining.

4. Position shot to include a fluttering small diameter palm, and a dilapidated structure with flapping corrugated metal.

5. Adjust light filter for gloomy effect.

6. Cut to animated overly-enhanced color radar during lulls.

7. Pan to blowing fronds, leaves and trash if possible.

Aug

31

On Leaking News, from anonymous

August 31, 2012 | Leave a Comment

The increase in leaked govt news releases coincides with the rise in curated "machine readable" dedicated news feeds hawked by the various data mongers. Everyone in that product chain has an incentive to front-run. And it would make sense that the robot news traders would have the same moral compass as the quote-stuffing HFT crowd.

Aug

31

Family Ties, from Russ Sears

August 31, 2012 | Leave a Comment

Last year I visited Spain, visiting a friend who came to the states for education and then went back. He has a job in the Ag Dept. What he said was that family and tradition run deep. He said it was rare for young people to even think of doing what he did, graduate studies abroad outside Europe.

My impression was that family was the safety net beyond the government. Besides the Gypsies and hostel tourists, there were few homeless people. Few drug addicts or winos on the streets. I asked and he said the families take care of them for the most part.

I suspect that those not in denial may think the government cannot be counted on but surely their families will hold together.

Aug

31

Surfonomics, from Jeff Watson

August 31, 2012 | Leave a Comment

This is near to my heart, approaches 100% correct, and is the right way to approach any environmental issue.

"Surfonomics Quantifies the Worth of Waves"

Aug

28

Free Probabilistic Graphical Models Course, from Linden Doerr

August 28, 2012 | Leave a Comment

I found this excellent Stanford course recently and wanted to share it with the site.

Probabilistic Graphical Models

Daphne Koller, Professor

"In this class, you will learn the basics of the PGM representation and how to construct them, using both human knowledge and machine learning techniques."

Pros:

-online

-respected teacher

-no money cost for course

-textbook is $85 at Amazon (or $100 less discount through MIT Press)

-time cost (8-10 hr/wk for 11 wks)

-prereqs: one programming language, access to Matlab or Octave, and the ability to do some abstract thinking

Aug

27

How to Start Trading, from Lars Gutt

August 27, 2012 | 13 Comments

Dear Mr Niederhoffer,

Dear Mr Niederhoffer,

I really like your website dailyspeculations. There are a lot of fascinating and interesting articles that lead to new ideas and inspiration.

I read in the "About V.N & L.K" section that you trained some very successful traders and hedge fund managers. I am a student of business administration in Germany and want to work as a trader in the future.

It would be interesting to know how the training of your traders was structured and what were the most important things you focused on during the training? If you were now in my age (25 to 30 years), how would you start and where would you try to get the sufficient education for this business?

I hope that you can help me with your insights.

I wish you all the best and hope you will continue to share your insights on the markets.

Kindest regards,

Lars Gutt

Victor Niederhoffer writes:

This is a good question. Does anyone have a good answer besides reading a good statistics book like [the old] Snedecor, Horse Trading by Ben Green, Bacon's Professional Turf Betting, and starting a hypothetical trading account, and doing some hypotheses testing from a field they know something about?

Jeff Watson writes:

A big question is why you would want to trade. Trading is a pretty thankless job, very tough, and maybe you only see the media presentation, or you want to tell people at a cocktail party, "I'm a trader," but I'd like to see a why.

Having a good mentor, someone that you can apprentice to, is the most important thing in learning how to trade. A good instructor is much more important than Ivy League Degrees, how to manuals, internet chat rooms, books, systems, gurus, the financial media, and all the other mind numbing stuff out there.

My mentor when I first started was an 85 year old guy who was first trained by Art Cutten. He learned well from old man Cutten, and taught me how to keep out of trouble. The main lesson to learn in trading, more than anything else, is how to keep out of trouble. Manage to keep out of trouble, keep your own counsel, and the mistress might give you a second or third date.

George Coyle writes:

Series 3 study guide is a great (relatively brief) overview of the commodity futures industry. It touches on styles of trading as well as goes through lots of the unexciting but important details (order types, etc.). (Outline of material covered in exam [pdf]). (Online version of Study Guide by Investopedia).

From there the Market Wizard books are good to look at the different styles to see which sounds the best to you.

If quant focused I would say read something on how casino games work (odds and such–Richard Epstein's Theory of Gambling and Statistical Logic book is good) and think of how that might be applied to markets with the trader acting as the casino. Focus on keeping it simple, think of what is practical and possible when working with data.

Read your books of course. Read interviews with William Eckhardt. Larry Williams' recent book (LT Secrets for ST Trading) does a good job of outlining how quant works specifically, as does Charles Wright's Trading as a Business. Livermore's How to Trade in Stocks is a good one too (less popular than Reminiscences but more of a "how to" manual).

Deitel and Deitel C++ How to Program is the best C++ manual out there in my opinion. I dodged it for years but it is crucial and so useful. www.thenewboston.com is a great website to watch youtube vids on various languages to get your feet wet (but Deitel is necessary if you really want to learn the specifics).

And just start trading. The best teacher is experience. Even if equipped with all the great logic from above it seems real experience is necessary to actually follow the rules.

Craig Mee writes:

Understand valuation. Get a handle on all things that move a market price. Maybe have an 8 week internship of your own making with 8 different dealers. Corn farmer, art dealer, financial dealer, car dealer, importer, etc, and understand that whatever you're trading, you potentially should be able to move in theory from one to the other seamlessly. You are a valuer first and foremost, and if you value it wrong, you will also see how most of these choose to cut their positions. This might help to keep in the forefront of your mind what your mission actually is.

George Parkanyi writes:

Well if you can get past the fact that he finally went bust and blew his brains out, I found Reminiscences of a Stock Operator, about Jesse Livermore, to be quite useful. The most notable things I remember are (1) "making the most money when he was sitting, not trading" – meaning a position needs time to make really big money, and (2) to Jeff's point about staying out of trouble – averaging UP a position once its already showing a profit, and never averaging down a losing position. (The latter is especially important when trading with leverage.)

Ultimately, it still comes down to a style you are comfortable with – keeping the staying out of trouble part in mind; however you do that. And this may or may not involve the things mentioned above.

David Lilienfeld writes:

Go through some psychology texts–learn to understand human behavior and get to know one's own temperament. Understanding on an intellectual level doesn't help much if one's temperament is suited to trading. I have an old friend from high school who was on the Solomon trading in the mid-to-late 1980s. He hated it, often spent the weekends sweating his positions, etc. He moved on to be a buy side analyst, became the portfolio manager for a number of funds that succeeded pretty well under his direction and prospered. He had no trouble sleeping as a portfolio manager, and as I said, his funds did very well. A college roommate became a sell side analyst and was bored as could be doing his job. He did OK with it, but not great. He changed employers (at one point he thought about leaving the industry if he wasn't hired by someone to do something other be an analyst), started in its training program and found himself on the trading floor. He enjoyed it immensely and retired last year (I'm still not sure if he "retired" or was retired by his employer; looking at his homes, it's not as though he's wanting for much, so maybe he really did retire–but it's also not been a topic open to discussion, at least not with me). My guess is that just about everyone on this list has friends with similar stories. The bottom line: You have to know your temperament. You can learn the math, but if you don't have the fortitude, the math doesn't much matter.

The psychology part is understanding what people are about. Understanding gambling is about the mathematics of risk. Important stuff to be sure. But people matter too, and understanding what they are all about is also important.

Those are my recommendations. Lucking into a good mentor helps, but observing for a while is also one of the best teachers.

Aug

20

Air Fees, from David Lilienfeld

August 20, 2012 | Leave a Comment

I'm headed to Barcelona on Tuesday for a week of business meetings. I decided to start using my old US Air FF miles for the trip (with more than a 1.2 million miles and given that I've stopped using USAir back in 2008, this seemed like a good use of them). Imagine my surprise to open my email this morning and find US Air's wonderful missive offering me citrus-marinated chicken skewers or vegetarian Portobello mushroom tortellini for the lovely price of $20. (I assume since this will happen somewhere over the Atlantic, there's no tax.)

I'm headed to Barcelona on Tuesday for a week of business meetings. I decided to start using my old US Air FF miles for the trip (with more than a 1.2 million miles and given that I've stopped using USAir back in 2008, this seemed like a good use of them). Imagine my surprise to open my email this morning and find US Air's wonderful missive offering me citrus-marinated chicken skewers or vegetarian Portobello mushroom tortellini for the lovely price of $20. (I assume since this will happen somewhere over the Atlantic, there's no tax.)

And the airlines wonder why people complain about air travel?

It would be good if someone took a look at how much the airlines are actually making off of their baggage fees, too. Yes, it's revenue, but the consequence is that everyone who can brings their luggage as walk-ons. While it took maybe 15 minutes to board a plane in the 1990s, these days it's at least 30 minutes and often longer. That's time lost from being in the air, which is after all what the airlines are in business for in the first place. I don't know anymore which I dislike more–air travel or airline stocks.

Aug

12

Cold Reading and the Art of Fishing, from Craig Mee

August 12, 2012 | Leave a Comment

Cold reading has much in common with market charlatans:

Cold reading has much in common with market charlatans:

"There seem to be three common factors in these kinds of readings. One factor involves fishing for details. The psychic says something at once vague and suggestive, e.g., "I'm getting a strong feeling about January here." If the subject responds, positively or negatively, the psychic's next move is to play off the response. E.g., if the subject says, "I was born in January" or my mother died in January" then the psychic says something like "Yes, I can see that," anything to reinforce the idea that the psychic was more precise that he or she really was. If the subject responds negatively, e.g., "I can't think of anything particularly special about January," the psychic might reply, "Yes, I see that you've suppressed a memory about it. You don't want to be reminded of it. Something painful in January. Yes, I feel it. It's in the lower back [fishing]…oh, now it's in the heart [fishing]…umm, there seems to be a sharp pain in the head [fishing]…or the neck [fishing]." If the subject gives no response, the psychic can leave the area, having firmly implanted in everybody's mind that the psychic really did 'see' something but the subject's suppression of the event hinders both the psychic and the subject from realizing the specifics of it. If the subject gives a positive response to any of the fishing expeditions, the psychic follows up with more of "I see that very clearly, now. Yes, the feeling in the heart is getting stronger."

Jeff Watson writes:

Here's a great how-to" book on cold reading.

Bill Egan writes:

A complementary resource I recommend is "The Definitive Book of Body Language" by Allan and Barbara Pease. Always watch peoples' body language and compare it to their words, and watch how both change over time. For example, when the fraud thinks he has you, there is often a split second where he will shift his body position and display a chilling facial expression like a fox looking at a chicken. That half-a-second is real important to you.

Jim Sogi writes:

Trial lawyers look for cues in the jury's race, clothes, hair styles, books or magazines, shoes, apparent class, education, prior experiences who they speak with, their background information on their questionnaires to get a read on how they might decide a case. Trial consultants use broader data on how similar groups might react to similar situation. During Voir Dire, a short question and answer period, the lawyer can ask the prospective juror some questions that might shed light on the juror's prejudices that would justify being removed from the panel or dispose the juror against the lawyer's client. Again, all forms of cold reading.

A fun game I like to play while people watching in restaurants, or on the street is to look at people and try to figure out without anything more than watching from a distance, where they are from, what they do, what the relationships are between members of the group, what they might be like. Family groups on vacation are a pretty easy read as well as their internal family dynamic. Old couples are straight forward. Groups of young people tend to send strong signals. Groups of business men, groups of tourists, newlyweds all have characteristic mannerisms. The next level to try discern their relationship, what they are like and get an idea about them from only external signals.

Aug

3

Wave Action, from Jim Sogi

August 3, 2012 | Leave a Comment

Even granting the the Elliott stuff is garbage, the opposing linear forces of buyers against sellers subject to a vig forms wave like patterns. All other waves can be modeled. Why not market waves?

Even granting the the Elliott stuff is garbage, the opposing linear forces of buyers against sellers subject to a vig forms wave like patterns. All other waves can be modeled. Why not market waves?

Leo Jia writes:

I'd love to hear others' comments on this. My take is as follows.

The market waves are actually constantly measured and modeled by market participants. These people then use their models to conduct trades on the market. This very action, as performed by many, then causes the underlying market wave to change its attributes, which then fades the models in use and causes the people using the models to lose money. This gives many the impression that market waves can not be modeled.

Perhaps akin to Heisenberg's uncertainty principle, which was initially mistaken as the observer effect, the above view of the market might be misconstrued. The uncertainty principle was later understood to actually state the matter-wave dual nature of quantum objects, regardless of the observation.

Aren't market participants very similar to quantum objects in this sense? What is the dual nature of people? Can't we say greed-fear?

Jeff Rollert writes:

I would argue the periodicity, or perhaps wavelengths, vary as do ocean wave patterns reflect long distance, off shore storms.

Long ago, I read somewhere that polynesian males hung over the side of boats naked, so their "sack" could sense current vs waves for navigation.

Perhaps the model should include waves and divergent currents.

Aug

1

Article of the Day, from Victor Niederhoffer

August 1, 2012 | Leave a Comment

"Geithner Urges U.S. Congress, Europe to Spur Economic Growth"

"Geithner Urges U.S. Congress, Europe to Spur Economic Growth"

A shot across the bow before the Wednesday announcement?

Garrett Baldwin writes:

I'm out at Indiana this week for my Purdue residency, and the first thing that I heard out of the trade econ professor's mouth is KEYNES, KEYNES, KEYNES justification…

Time to break out the spoons and start digging. We'll eventually make it to China so we can pay them back.

I am attempting to justify a question on this. How do you print or borrow the size of a stimulus you want… at trillions… and expect our economic and political system to somehow get the targeted stimulus that they proclaim possible? There will be buy-offs, write-offs, handshakes, and so one… And by the time we get down to it, the very areas they want to stimulate that have any economic merit will be 3 percent of the money spent. I'd rather just go with the helicopter plan.

Jul

18

The Real Class Warfare, Garett Baldwin

July 18, 2012 | 4 Comments

Here's the brewing problem that I think about every day: "The Real Class Warfare is Baby Boomers vs. Younger Americans".

Here's the brewing problem that I think about every day: "The Real Class Warfare is Baby Boomers vs. Younger Americans".

I'd claim it drives me to drink, but do I really need excuses?

While my parents worry about my future… I worry about the solvency of the programs that their generation built… and how 14 percent of my freelance revenues might as well be lit on fire because (let's be honest) my social security and medicare taxes are not coming back with the same purchasing power or benefits guarantees (The healthcare system in 2053 will be tremendous, I'm sure).

These programs obviously need some means testing, as Pelosi's generation and anyone with 20-30 years of business experience will likely be much better off in the U.S. at their age then my generation will at 50 through 70, given resources, expanded competition from abroad and so on.

I personally feel sorry for anyone under the age of 27.

I graduated in 2004 (in a bad job market) and was still just able to sneak out and get 4-5 years of solid experience before the bottom fell out in 2009. Then I was able to go onto grad schools…I think I barely escaped. But it appears that fewer and fewer in 2008-2011 undergraduate classes are able to get the practical experience before they hit 30.

I spend a lot of time researching the impact of the recession on MBA education, and I'm seeing the ages go up, and applicants 22-27 being shown the door before they even get a chance to say hello. How we're going to sustain and educate our next crop will be a new gap. I am interested to see if there will be a significant pay gap between individuals 30-40 today, and individuals 30-40 in ten years.

Every day, Australia looks better and better to me for a 2014-2015 move. Too bad the IRS will meet me at the docks once I get off that slow boat.

Ralph Vince writes:

Garrett,

Thanks for your posting. Your post deserves comments from the more geezerly here. Permit me to be the voice of those despised boomers.

I agree with you on inter-generational warfare notion. I hear it incessantly from the younger (<35) crowd, and not that it is without merit, I find it's rather one-sided. I am left wondering, despite the miserable economy and resultant job market of recent years, why the animosity? I, for one, twice your age, having been paying into the Ponzi schemes at over 18% per year for over 4 decades of my working life. Most in my circle seek to dismantle these Ponzi social programs, and agree the place to begin is clearly through means testing. I too don't expect to see a dime from these systems (not that I would qualify under means testing, but I would prefer we stop the Ponzi nonsense and consolidate it all under Welfare. Actually, I would prefer they do away with it entirely for that matter!)

Don't forget, roughly half of us boomers have been relentlessly voting against any of this nonsense our entire lives, and have sought to have it dismantled, but we have been outnumbered by the handout crowd — I believe your generation fear the boomers now becoming the handout crowd, an understandable concern given the demographic imbalances. Here is what they evidently don't teach in grad school (and I don't say this with condescension, rather because I find a conformity in perspective among the < 35 crowd). Straight-line forecasts into the future never work. The image presented to those your age — the straight line, cause and effect, demographically created scenario — that demographic doomsday isn't going to happen. Things always, invariably, descend from outside the system, rendering the straight-line forecast of the masses substantially wrong.

I don't know precisely WHAT those outside influences will be, but I'm pretty certain they will be severely pro- economic growth. This will have profound and far-reaching economic effects on the generation of workers now < 35. I'm not talking in the distant future either, but rather this decade. Don't be surprised to see home values surge, 200 to 300 percent over an 18 month stretch — when people least expect it. Don't be surprised if we need to bring in a few million qualified tradesman, or real competition among medical services in the US, wrought from outside the US. Don;t be surprised with plentiful, inexpensive oil and electricity. There are a myriad of factors now conspiring to create an enormous economic boom. Don't buy the "We are going the route of Japan" scenario. We are not Japan. Don't be surprised by double-digit GDP growth at some point this decade. The ground is shaking right now, and the < 35 crowd is unwittingly standing atop a mountain of opportunity for those who can shed the yoke of perspective that has been sold to them.

Lastly, Australia? Forget about it. Throughout my entire adult life, I have been of the mind that the US is really NOT the place to be if one wants opportunity and economic growth. I believe that is now flipped, and the states very likely presents the prospect for great growth and opportunity in the coming decade. This is a time to sit tight, take chances, and if things soften more, risk more, buy into it.

That's my two cent take, I wish I was young enough to capitalize on it the way a young man could, but I'll stake my future entitlements on it.

Jul

17

Loss Leaders, from Stefan Jovanovich

July 17, 2012 | 4 Comments

We had a recent debate on the economics of medicine that — unfortunately– veered over into the realm of politics. I hope these facts will be considered solely as a question of how the business of medicine has evolved recently for hospitals:

According to the NEJM ED (emergency department) visit rates increased by more than a third between 1997 and 2007…The number of hospital admissions increased by 15.0%, from 34.3 million in 1993 to 39.5 million in 2006; admissions from the ED increased by 50.4%, from 11.5 million to 17.3 million.

The proportion of all inpatient stays involving admission from the ED increased from 33.5 to 43.8%.EDs have become the primary growth area for what all hospitals must have in order to make money - a supply of patients who stay for more than 1 night and have a major procedure.

Jeff Watson writes:

I suspect the hospitals realize Stefan's observation. All around my town, Doctor's Hospital has billboards up with a real time wait numeric display for the wait time of the emergency room posted. If they say that the ER an 11 minute wait, a 2 minute wait, or a 30 minute wait, and they advertise this all over town, is it really an emergency room? FWIW, they also have smart phone apps doing the same thing.

Dan Grossman writes:

I doubt anyone who has received or seen a hospital emergency room bill in recent years would regard it as a loss leader.

It is a mystery to me why Medicaid, Medicare and other programs do not encourage patients to go, if possible, to one of those for-proftt medi-quick clinics for a $150 bill, instead of to a hospital emergency room for a $1,500 bill.

Bud Conrad writes:

I fell off my bicycle. (In Calf.)

I was strapped to a board and taken against my will to the Stanford hospital where I was in a neck brace for hours and was X rayed. Cat scanned and get this: given a sonogram! I guess they thought I might be pregnant. The 10 minute ride to the hospital was $1500 the emergency room about $15,000, and a couple of days later in a different hospital the surgery for a broken arm was $103,000 - not including the doctor, anesthesiologist, nurse or follow up care.

This system is broken beyond repair and a disgrace. From my point of view a POX on the whole lot of doctors, lawyers and government sponsored payments system!

Jul

15

It Is Interesting to See, from Victor Niederhoffer

July 15, 2012 | Leave a Comment

It is interesting to see that the sage was the one that blew the whistle on their competitor AIG, in a so typical gesture of deflection, self-servingness, sanctimony, and fellow travelership. How many others beside Sobel and Greenberg has he deflected.

Mr. Krisrock comments:

Buffett hates hedge funds, high tech, anyone who has lots of money and like him hasn't created foundations that pay no cap gains or ordinary taxes…he doesn't buy new cars, he gave up his reinsurance insurance CEO…he is truly the last angry man.

Jul

13

Facebook, from David Lilienfeld

July 13, 2012 | 1 Comment

Perhaps someone can explain this one for me:

Perhaps someone can explain this one for me:

Facebook is valued at an astronomical amount. Its revenue base is, basically advertising. But FB is sustained, use-wise, by kids and young adults ( <30 ), who at one time had a fair bit of purchasing power and/or influenced significantly what a typical family bought.

Today, however, that demographic group doesn't have that kind of purchasing power. So what's the appeal for advertisers in supporting FB? Is there any data to suggest that ad buys on FB have a higher ROI than other media venues?

If not, is FB just a lousy investment, or a good one because these things are temporary?

Anatoly Veltman writes:

Also, consider the theory of reflexivity in the case of FB, of self-perpetuation. I notice that my 11 y.o. daughter has gained self-confidence (and self-absorption) via FB-ing.

Those kids flaunt their "social edge" over the older purse-holders, and pull on purse-strings with ever-increasing zeal.

Like Henry Ford said, "I'll pay my workers enough to buy my cars", FB is fostering its own consumer channel.

Gary Rogan writes:

The hope with large end-user software companies has always been that they (a) create dominance in their particular specialty (b) use this dominance to figure out as yet unpredictable way to monetize way beyond their current valuation (c) use this dominance and their speed of execution to stay ahead of adverse end-user trends. If often hasn't worked out this way, but of course when it does you get outsized returns.

Stefan Jovanovich writes:

For the most recent quarter FB generated roughly $.5B in EBITDA - the same result that my favorite submarine with screendoor investment - AMAT - produced. FB did it with 1/4th the number of employees and 40% of the revenue. Does that justify a valuation 5 times what the market now pays for Applied Materials? Yes - if the belief continues that network effects will predominate in social media as they have in paid search. The world will need the production of foundries - both steel and silicon - but it will only pay a premium for businesses that promise that their profit margins will increase on marginal sales because there is no used/distressed inventory out there to compete with the "new" products. The answer will be No only if the world of corporations and teenagers decides that Google+ is a better way to sell their virtual images to the world. (Note to file: since those of us here at Chaos Manor now buy and own stocks as if they were cars and houses - i.e. once we find one we like well enough to buy, it is usually a decade and more before we even think about selling, these comments are only for people - all 3 of you - still willing to attend early morning mass at the church of Buy and Hold.)

Peter Tep adds:

Above all else, Facebook is just a huge time sink and besides being a networking tool, is another place for people to gloat and boast or climb the social hierarchy — meant in a non negative way. With so many kids using it and literally connected to it 24-7, it's probably going to be a good investment if Facebook finds more ways to market to it's users on an even more emotional level. Has anyone seen the series posted on Ritzholtz blog about this?

I guess it is a great investment because it keeps people emotionally connected, like a great movie is playing out in front of them and they are part of it. If Facebook refines its marketing strategies even more using its users' data, then I guess the sky's the limit.

Jack Tierney writes:

David asks some important questions regarding FB and its value. I agree that the current price is astronomical, but have very little knowledge of the operation — I am not a member and, barring any unforeseen developments, will not join. I have followed FB for sometime and have not joined because of the incredible amount of information they can gather regarding your personal history, preferences, and affiliations.

That very knowledge, though, explains why this could be a very rewarding investment. Back when I was still employed I did some work with the "research and marketing" groups. One of the first puzzling discoveries I made while going over some data was that, although our newspaper regularly received a huge amount of national food advertising, the relatively small markets covered by the Miami Herald and the Milwaukee Journal, received more.

It was explained to me that both cities were unique in that they were split almost evenly demographically. The wealthy, well-to-do, and upper middle class occupied one half of town, those not that well off, the other. This gave General Mills, Coca-Cola, Proctor & Gamble, etc. ideal platforms from which to launch new products, different packaging, innovative couponing programs, size and container preferences (12 oz. cans vs. 16 oz. bottles).

These two cities gave marketers some valuable insight into buyer preferences…yet it was no where near good enough. The Holy Grail, what each individual preferred, was not only impossible to discover, but impractical to reach. That may now be achievable with FB.

While many who are members argue that they reveal very little about their preferences, few are aware of how much their "friends", directly or indirectly, reveal about them. The most memorable story sent to me regarded an English woman who had been "on the dole" for a couple of years, receiving whatever that country's monthly stipend is for an unmarried, unemployed woman with two children. Someone from Inland Revenue (apparently the equivalent to our IRS) decided to check up on her. Rather than checking her page, he started with the pages of some of her friends.

He happened to come across one that featured a several month old picture of the woman in question, relaxing on a beach in some exotic, expensive European resort — with her new husband. Her friend also happened to mention how fortunate she had been to have an employer who let her take a month long paid vacation.

Well, the outcome was not a pretty one. But the story illustrates that if a "friend" should just happens to mention you're a pizza lover, expect to get an uncommonly large number of pizza promotions - from Pizza Parlors in your very own neighborhood. (How did they know???)

If FB plays this right, they could pull in billions. Marketing has always been about reaching the maximum number of potential buyers for the least cost. From what I've read about FB, this is within their reach. If they follow through, or allowed to follow through, their reach is incredible and I would consider buying.

J.T Holley writes:

I'm 41. I choose to "like" The Jefferson Theater so that I could see the feeds/updates of concerts that were being booked. I got notice that they were having a Southern Rock Band "Blackberry Smoke" play on July 25th. They also said that if you "liked" the announcement then you would be put into a drawing for free tickets. I won. I have two free tickets and allowed them (they asked) if they could say that I won.

GM and all others that don't understand the power of FB are foolish. It reminds me of A. Miller's "Death of a Salesman" and Charley's wise words:

"The only thing you got in this world is what you can sell. And the funny thing is that you're a salesman, and you don't know that." Charley

and he best double negative ever to be used in writing when Charley addresses Willy (foreshadowing).

"Nobody's worth nothin' dead." Charley

Google became the yellow pages.

FB is becomin' greater than the yellow pages.

It's a tectonic shift that many aren't willin' to accept or grasp. I'm nobody and humble and I get it.

Dylan Distasio writes:

While I think your example is a good one of what Facebook COULD monetize, they are far behind Google on most advertising metrics and have a very low click through rate on the ads they do allow. It's understandable, Google is in the business of ads and has been at it for longer. Zuckerberg seems hesitant to admit or embrace the fact that FB is also in the business of advertising.

And the fact that Google is a yellow pages should not be scoffed at. It is a large part of why their ads in search work and demand higher prices. They are for things people are looking for and highly targeted.

I think with the amount of personal data Facebook has, they have great potential to monetize ads. The big question is whether they are interested, and if so, will they be able to execute.

The current issue of MIT Technology Review has a great article on a team at FB that is looking at the bigger picture in sociological terms of what they can do with the data. While their explicit goal is not focused on monetizing the data, some interesting techniques for doing so may come out of it indirectly.

Facebook has to be careful about how far they go in using people's data in the interest of monetizing it, and has to build a more sophisticated toolbox of ad types and techniques if they want to compete with Google. While they have certainly reached what appears to be critical mass as a social network, people can be fickle with their allegiances, and are happy to jump ship to something else when they get bored or feel slighted. FB will be forced to walk the same tightrope Google does if they want to seriously compete with them.

It should be an interesting couple of years watching this unfold. That said, I think based on the current view of things, FB is tremendously overvalued unless they are willing to start heavily exploiting the data in their possession. I'm not sure Zuckerberg is willing to, and he controls the company with 51% of voting shares. He's now a billionaire and can run his own agenda for quite awhile at the shareholders expense. As an example, I would question his acquistion of Instagram for $1 billion dollars but I guess time will tell. It will help them in the mobile space where FB is currently very weak, but we'll see if it was worth a billion to buy a company with no revenue.

Jul

13

Home Construction, from David Lilienfeld

July 13, 2012 | Leave a Comment

There are those, like Doug Kass, who are pounding the table and screaming about the dawn of a multi-year housing boom in the US.

There are those, like Doug Kass, who are pounding the table and screaming about the dawn of a multi-year housing boom in the US.

Yet I remember reading in Barron's a few years back that the major determinant of long-term housing trends is the formation of new households. Many kids, who have had trouble finding a job that pays sufficiently for them to run their own household or not having a job at all, have moved back in with their parents (the boomerangers). We've deported a lot of folks, too (who might otherwise form households), and there's been no increase in immigration quotas. In general, it's only the middle-aged and elderly that are growing in size, and those age groups aren't known for lots of new (or net) household formations.

So where's the increase in households going to come from to drive that boom in the market? What makes me even more confused is the comment on the Toll Brothers call that the company finally has pricing power in 16 or its top 20 markets.

Something's not right here.

If there is a boom, or even a boomlet, do you go with Toll? Lennar? Ryland? Or the suppliers (small caps like Lumber Liquidator or large caps like Home Depot)?

Thoughts, ladies and gentlemen?

Jul

6

The market continued its inexorable advance while I was away in Ocean City, New Jersey, one of the finest resorts I have even been privileged to be in. A reason for its harmony is the absence of alcohol. I have been reading Master and Commander again, and find many fantastic insights in it–Nelson always said that since you were always five minutes and a few pieces of wood away from a terrible disaster, you had to be eternally vigilant. What will the employment figures look like tomorrow. There will not be as much pressure on the employees to adjust them upward one would think with the favorable supreme court ruling to them.

Jul

6

Stocks vs. Bonds Again, from Victor Niederhoffer

July 6, 2012 | 2 Comments

I was thinking while away that someone is going to make the case soon that stocks should be 10 times higher than they are now, because they are comparably volatile to bonds, and yield 10% return on equity + growth of 5% versus 2% on bonds via the Gordon model or some such.

Jul

4

Happy Fourth, from Alex Castaldo

July 4, 2012 | Leave a Comment

A Happy Fourth of July to all our readers. Enjoy the fireworks.

Jul

1

To Add to the Debate, from Duncan Coker

July 1, 2012 | 1 Comment

Some non partisan predictions based on the ACA implemented as it appears it will be. Simple supply and demand tells me with an additional 30-50m people having subsidized access it must drive up health care costs. If there was a pure index on health care costs I would go long. Premiums on average will go higher as the costs are just passed through and the incentives are structured to consume more not less heath care.

Health insurance only companies I think will be driven out of business by two factors; they can no longer perform their basic function which is actuarial expertise. Second their gross margins are capped at 20% and most margins will be lower as premiums won't be able to keep up with the rising cost. I would not want to be in that business.

However, the more diverse companies like Wellpoint and United Health have a valuable asset. This is decades of health care record on millions on individuals. So these companies and other like them will convert themselves to care providers, administrators of self insured plans, and offer diagnostic or preventative care services. These I see as big growth areas. Retail companies with direct access to consumers like Walmart will expand further into providing heath care services to meet rising demand.

From the market reaction this week it seems the ruling was a non event. The added burden to large Fortune 500 companies will be passed on to employees in the form of higher co pays. As long as the expense deduction is there, providing health insurance is still a good way to transfer compensation to employees void of taxed. The middle range companies (50-100 employees) will do the same or can opt our entirely and pay a fine. Of all the articles I read in last two weeks I found Sowell and Asness had some insightful writings on the subject.

Stefan Jovanovich adds:

The Armed Forces have been privatized. Conscription is no longer -politically - available. Intraservice competition among what are now 4 branches of the service - Army, Navy, Air Force and Marines - and the effective abolition of the draft have forced the official dealers in death and destruction to continue to innovate. It no longer requires 55,000 bullets to kill a single enemy (that was the effective kill ratio in the Viet-Nam war). If we had the "single payer" system David wants and the one Truman wanted for the defense department as well as for American healthcare, we would have seen the U.S. follow the disastrous path the Canadians and Europeans and now - sadly - even the British have followed. The budgets would have remained largely intact (as they have for NATO), but the ability to break things would have disappeared.