Jan

9

Pool Hustling 101, from Howie Eisenberg

January 9, 2012 | 4 Comments

Vic,

Vic,

I hope all is well with you and the family. I took an online course on writing autobiographies and thought you might enjoy the attached.

Happy new year.

Love,

Howie

—

"Never give a sucker an even break," uttered by W.C. Fields in the 1941 movie so entitled could well be the credo of the pool hustler. What does this have to do with me? Fleecing the less proficient at what is termed pocket billiards in some circles was a significant source of income for me from age 15 through college. It accorded me a much needed supplement to my meager allowance and/or the part time jobs that I held as a student.

At Brighton 5'th Street at the same level as the elevated subway train that runs along Brighton Beach Avenue, there existed a 2400 square foot den of iniquity that housed about a dozen pool tables. This sea of slate covered by green felt was not a billiard emporium by any means. In the mid 1950s, it was frequented by many of the neighborhood's young toughs and assorted characters like Mutt, Teddy the Twitch, Pittsburgh, the Guzzer, Sonny, Sam the Communist, Blackie, and Miguel. Sonny was a big muscular homosexual whom nobody messed with. Silver haired Sam was the best shooter in the pool room. Blackie a middle aged man was a close second as he ran rack after rack in straight pool, never taking off his hat. Miguel, a bookie who ran a cut poker game and was later shot to death after balking at sharing profits with the mafia was about as good as Blackie. Added to the mix were me and some of my school friends including Harvey Keitel, who later became a well known actor and Mark Reiner, a basketball star.

The pool room was a hustler's haven where we hung out after school until 1:00 A.M. closing when we weren't playing ball. Substituting time there for homework, our formal education may have been diminished but the street smarts we acquired were more than ample compensation. The proprietors were two diminutive men in their sixties, Izzie and Charlie, a pro boxer of some renown in the '20s. Despite their age and small stature they ruled their roost with an iron will. Roost was more than a figure of speech in this instance as there was a creaky stairway that led to the roof that housed Charlie's pigeon coop. He had preceded Mike Tyson in pugilistic affinity for our fine feathered friends by 4 decades.

The absolute power that Izzie and Charlie had over all of us was the specter of being barred from entry into this hallowed ground and being relegated to hanging out in less exalted venues. After learning the rudiments of the game, I gradually acquired a modicum of skill by observation, shared tips, and practice. Making a stable "bridge" with the non-shooting hand; keeping one's head down; and a smooth stroke were basic requisites. Learning where the object ball must be hit by the Q-ball to direct it into a pocket is essential. Although the ability to make difficult shots comes in handy, getting the Q-ball into position for an easy shot after making the preceding one is what distinguishes the more accomplished practitioners of the game.

"Position" is achieved using various methods. "Drawback" to make the Q-ball go back in the direction from whence it came after striking the object ball is accomplished by striking it low and snapping the wrist imparting back spin. "Follow-up" to make the Q-ball go forward is effected by striking the upper portion. Either of those techniques can be applied in conjunction with "English" to make the Q-ball go left or right after hitting a rail by striking it on the left or right side respectively. How hard the Q-ball is struck determines the distance it will traverse and its ultimate position..

Most games were played for money with the stakes ranging from "time", the 50 cent per hour charge for use of the table to many dollars. There were various handicaps given to supposedly level the playing field but after blowing my allowance a few times, I realized that you never play better players. They are not only better, they are more knowledgeable and better able to figure the "spot" that will still give them the edge.

Accomplished hustlers rarely play better than needed to win and frequently let the "fish" win for small amounts and reel him in when the stakes are raised. Another gambling precept was always put the money up with someone who can be trusted to pay off (the "house": Izzie or Charlie in most cases). This was especially important for me at 6' 1" and 150 pounds against many of my more burly adversaries.

I never became a great pool shooter but the level of proficiency was not nearly as important as applying these principles. The goal was always to have a "lockup" - a game where there is virtually no chance to lose. Another way of putting this is, "Never give a sucker an even break". As mentioned, hustling was a significant source of income for me during my school days. In actuality, outsmarting and outplaying my opponents was more important to me than the extra cash in my pocket. One of the greatest compliments I ever received was years later when I ran into a guy that I had known casually and he said, "I remember you. You used to make your living in the pool room".

P.S. In retrospect this sounds pretty crass but I didn't cheat anybody. Everybody was trying to get the edge. I was just more successful at it than most.

Jan

9

Harvard College: Squash & Scholarship, from Richard Kostelanetz

January 9, 2012 | 2 Comments

Richard Kostelanetz writes:

My friend Victor drafted this essay toward his autobiographical The Education of a Speculator (Wiley. 1996), only to obey his publisher’s command to reduce personal material, which he did, nonetheless leaving behind in his book a luminous opening chapter about growing up amid the handball courts in Coney Island, New York. Self-published in 1994, this essay inspired my own memoirs published here. Since Victor’s Harvard memoir is unavailable elsewhere, I'm pleased to reprint an excerpt of it, with his permission and my gratitude. I’ve omitted a few digressions in the original, while adding between brackets some clarifications. You can find the whole essay in my latest book.

HARVARD COLLEGE: SQUASH & SCHOLARSHIP

Victor Niederhoffer

Copyright c 1993, 1994.

Education at Harvard has always favored the dilettante, coddled the "gentleman's C" scholar and allowed those who concentrated on extracurricular activities such as football, computer programming or musical theater to survive. During my undergraduate years (1960-1964), of the 1,500 freshmen entering each year only a handful wouldn't graduate. To earn a degree with honors was as easy as getting a mosquito bite at a nudist colony; more than half the class received this token, even in those days When you consider that at least half the student body at Harvard hardly attends more than half of their classes, and most of the others are so totally committed to their extra-curricular activities that they have no time for reading the assigned course work, let alone any outside readings, the graduation rate becomes an example of noblesse oblige.

I was one of those students who would have been hard-put to survive in any other college. I have always had a reluctance to attend large lectures. And most of the popular undergrad courses were given by eminent professors in halls like Sanders and Emerson where 500 to 1,000 were in attendance, if not wakefulness. The smells in a lecture hall turn me off. I can't breathe well with all that carbon dioxide circulating back into the air. Besides, I like the idea of feedback. The ideal form of education to me has always seemed to be sitting on a log with some erudite professor on one end and me on the other, talking about areas of common concern. In this day of copiers and desk-top publishing, there is no reason why lectures should be delivered in a no-feedback format. Notes could be prepared in advance and distributed to students. This would force the instructor to be concise and accurate, as the printed word

demands more presentational logic and rigor than does the spoken lecture. I have found that only at prestigious universities and cabals do the lecturers balk at providing written notes.

During the 2 or 3% of the time in my waking life I have truly been interested in becoming educated I have garnered 99% of my learning. I suspect I am typical in this regard. The challenge to the educator, then, is to motivate the student to desire to learn, and then to figure out how to provide the product when it is desired.

On a more mundane level, I have always found it difficult to stay awake at morning activities after a strenuous day of exercise. And my mornings were invariably taken up with a squash match, and then a rush to finish up my homework. Having not yet developed the art of blindfold checkers or chess play, only way I could stay awake in class was to buy an advance copy of the Suffolk Downs Racing Form and handicap the races. Many of the professors seemed to me to have been coerced into teaching the undergraduate courses because they were over the hill. Others seemed more interested in the handful of attractive [Rad]Cliffies in the class than in engaging in dialogues with shallow Harvard youth.

I subsequently learned how right I was in this regard, at least with respect to the University of Chicago, where I read rhapsodic letters of recommendation for Michelle S., my sweetheart during my time there, of the professors independently wrote about how they looked at her constantly while lecturing for a feel for how it was going, and how uplifting it was to receive her approval when they delivered a particularly apt précis, how they valued the feedback she provided with her smile, frown and other body language. I noted that they found her body language equally uplifting outside of the lecture halls. She told me that once she was having a departmental dinner with four professors and four students at a table at the Faculty Club, and that three of the professors independently passed her notes to meet them afterward for a continuation. Needless to say, she graduated summa cum laude, one of two of her class (1966) to do so. As I was to learn some years later [while teaching] at the University of California at Berkeley, this incident was merely one example of a tendency endemic to academia.

Even with the policy of noblesse oblige, my education at Harvard was in jeopardy. Professor Williams, who taught my Introduction to Logic course, one day caught me in the act: he suddenly stopped his lecture, walked to my seat and grabbed my Racing Form, loudly upbraiding me in front of 500 eager scholars for my rudeness in handicapping races while he was droning on about such fascinating subjects as the difference between probabilities based on relative frequencies and degree of belief, and the Popperian view of probability as a revised estimate of one's knowledge based on various hypothetical experiments.

Since that time, I have found only one satisfactory motivation of probability. This was by Richard Hamming, a professor at the U.S. Naval Postgraduate School. Strangely enough many 'experts on probability theory have worked at military installations, especially in England. Hamming's view is that where you have events in a sample space, such as tosses of a die, that are symmetric, or interchangeable, the probabilities must all be equal. So if you take the number of events possible in the space, the probability of each event must be one divided by the number of events. As Hamming remarks in a typical passage, "Although very likely you have been interpreting many of the results in terms of frequencies, probability is still a measure derived from the symmetry of the initial situation." (The Art of Probability, 1991).

His extensions are sufficient to resolve all the philosophical questions that were the meat and potatoes of Professor Williams' class.

But first, I had to get through my classes without unduly antagonizing my teachers, as my performance on exams would never be sufficient to undo any bad impressions made on the professor, nor would I have enough sex appeal to barter for a good grade.

My solution was one of my masterpieces. I noted that most of my teachers were graduate students obviously down and out in terms of money, but who were teaching for the prestige and potential career advancement. When I saw them, they always seemed to be grinding away at their own course work in an effort to reverse their bad fortunes by garnering a job. Even then, Eastern Illinois University favored [hiring] assistant professors who had put in a stint as an adjunct assistant professor at Harvard earlier in their careers.

Now Harvard has always been masterful at maintaining low salaries among their employees. One of their techniques was to refuse to hire any of their graduate students until they had taught at some other school for at least five years. This policy was already famous in those days for having lost Paul Samuelson, the famed Nobel Prize-winning mathematical economist who popularized Keynesian economics in his best-selling textbooks of the 1960s, and who can still be counted on to trot out his theory favoring greater government spending and higher taxes for the benefit of any sitting or would-be President. Samuelson's doctoral thesis, written at Harvard in 1955, was entitled "The Foundations of Mathematical Economics", in which he quantified the interaction of the multiplier and the accelerator in fomenting government's impact on total output. This study is still considered one of the classics in the field, but it wasn't sufficient to break the Harvard taboo against hiring its own.

But there was a quid pro quo for the graduate students. In exchange for low wages, and no chance for tenure, the grad students were graded on a very high curve. The average grade in most of the graduate courses, A-, was considered quite good in those days before grade inflation, egalitarian marking, and numerous pass/fail courses — all of which have made most grade-point averages as meaningful as the chants of the whirling Dervishes.

I quickly realized that if I confined myself to graduate courses as an undergraduate, that even if I consistently copped the worst grade in the class, I would still be likely to pull a B+. And this would more than compensate for my bad study habits.

I was so successful at this approach that when the time came for a final class ranking of all the economics majors at Harvard I came in second out of 150. My technique did not pass unnoticed. Any time an undergraduate of apparently limited intellectual accomplishment took on a curriculum of mainly graduate courses he or she was said to be "Niederhoffering the curriculum." .

Years later, I ran into Professor Wassily Leontief, founder of input-output economics, at a [George] Soros party. Soros loves to stock his foundations with distinguished, collectivist emigrés from Eastern Europe and Russia. Leontief was at that time serving on the boards of some of Soros' foundations. He had been my professor in 1962 in graduate-level Microeconomics 201, where I had received a B+, the worst grade in the class. The Professor's basic idea, that there are fixed technological relations between the output of an economy and the raw materials necessary to produce them, makes about as much sense as the Russian notion that there are some genius master-planners in Washington responsible for all the wonderful variety of goods on American supermarket shelves. Nevertheless, Leontief had one of the sharpest minds I have ever encountered. He remembered me, after 25 years, and said, "Here you are Niederhoffering the commodity markets by picking up the detritus of Soros' trades, just as you did in my classes." As I was surrounded by government officials, foundation mavens, administrators, philantropists and other liberal types — as is the norm at a Soros party (and indeed at most other New York parties I have attended) — I held my tongue and played the respectful guest.

* * *

The Harvard Club of New York each year collects a scholarship fund for needy students with outstanding academic records. Somehow my credentials and my experiences at my high school, where the principal was actively working to keep me out of college, struck a responsive chord in some of the members of the scholarship committee, and I consequently was a beneficiary. Some of them, apparently, had also once been blackballed, and instead of working against me, my principal's active lobbying actually helped me. My experience coaching at Kaplan and the resulting improvement in my board scores didn't hurt either.

Even with the scholarship, my parents were making a heroic sacrifice to keep me at school. The then staggering tuition and board of $3,500 per year represented 25% of their pre-tax income. The balance of $1,000 they gave me for out-of-pocket expenses added further to their debt. It seemed only fair that I should reduce the burden by getting a job.

My first job at Harvard was in the Student Post Office. My duties were to sort the mail and run the route, delivering and picking up mail at all departments on the north side of the campus. The pay was the munificent sum of$1.80 an hour. After a few days on the job, I graduated to full-time mail carrier. My boss, an elderly Irishman with white hair and a Boston accent, was from the old school. His shoes were polished to a gleaming luster and his tie choked his neck in a perfect knot. As I left for a delivery one day in typical Boston fall weather, freezing rain with winds in the 50 mph range, he gave me some sharp advice. "Keep your head on your shoulders and whatever you do, don't miss picking up the mail at the Watson Laboratory in Biology. Since that professor won that Nobel Prize, he's thinks he owns the world, and when the mail isn't picked up twice a day, he calls up to complain. Last time we missed him, I found myself apologizing to a vice president of the corporation. "

Yes, Mr. McCarthy."

I have never been too good at sense of direction, and now, in retrospect, I see I was not well-suited to a career in mail carrying. My ideal career would probably be as the women's squash coach at a large university or director of research at a flavoring laboratory. But I needed the money from that mail job badly. Perhaps I was distracted by the rain, the secretary, or my studies, but I did manage to forget to pick up at Watson's lab. My boss's dismissal of me was abrupt.

"You're fired. How they let incompetents like you into Harvard, I'll never know. You don't even have enough sense to get out of the rain and come inside to pick up at the one place I told you over and over again not to forget. Get the Hades out of here and never come back."

I was crestfallen. This was the final blow. No way was I going to ask my parents for more money. It looked like I would be going back to Brooklyn College after all. Life seemed hopeless, so I called my father up and gave him the bad news.

"Don't worry about it. This could be a blessing in disguise. Remember what happened to Winston Churchill, as a young man in the British Army, on his arrival in India. Eager to disembark from a small boat that was tossing on the waves, he grabbed an iron ring fastened to the pier just as the boat fell sharply, and dislocated his shoulder. This injury stayed with him the rest of his life, and plagued him in every physical activity he undertook from then on, from polo games, to speaking in Parliament, to war.

"But as he says in his book, My Early Life, the injury probably saved his life during the battle of Omdurman. He was the only one in his cavalry to be unable to swing his sabre; but knowing his shoulder might give out at any time, he had purchased one of the newly-invented Mauser automatic pistols, and had practiced with it assiduously in preparation for the campaign. In one cavalry charge, he saw most of his colleagues cut to pieces around him by the dervishes' scimitars in their fierce resistance. But his skill with the Mauser saved his life, and he wrote of the experience, that one never knows when some apparent misfortune might actuaJly save one from something much worse.

"So remember, what seems to be a tragedy might actually be a lifesaver"

(to be continued).

RIchard Kostelanetz Books on Amazon

Richard Kostelanetz eBooks on Kindle

Dec

22

10 Things You Can Learn About the Market from Greek and Roman Times and Myths, from Victor Niederhoffer

December 22, 2011 | 2 Comments

1. There is a critical point in the market, a critical decision that the market gods weigh on a scale like Zeus with his balance scale deciding whether Achilles or Hector will win, that determines the market fate, and it is key and should be the focus of all news stories and market considerations but never is.

1. There is a critical point in the market, a critical decision that the market gods weigh on a scale like Zeus with his balance scale deciding whether Achilles or Hector will win, that determines the market fate, and it is key and should be the focus of all news stories and market considerations but never is.

2. Never trust anyone but your family and best friend because everyone is disloyal in a pinch. Peleus was left for dead by his father in law after killing his brother in law to become ruler and this led to the Trojan war. Caesar trusted his best friends but they turned on him when an opportunity for power, money, and romance reared its ugly head.

3. Deception is key. The most successful Greek was the Deceiver Odysseus, and he tricked everyone he dealt with as the market tries to trick you with Odyssean power.

4. The goal is always to come home. Odysseus went home, as does the market. The only loyal ones were the wife and son and the best servant. The market retraces and comes home to break even an inordinate number of times.

5. Never mix romance with business or the market. The Trojan was was started by Paris intervening in romance and being swept off his feet by Aphrodite, and Achilles killed tens of thousands and prolonged the war by 10 years when Menelaus stole his mistress.

6. Don't try to walk with the Gods. Peleus married a half God and married her the last time the Gods and mortals mingled at a celebration and it caused him to be the most distressful of men. Trying to emulate Soros or the other greats is the seed of destruction.

7. Okay, give me the rest. And correct and tighten the above. I'm out of my depth but wanted to get the gist across.

Ken Drees comments:

Like using a mirror against Medusa, one must plan against the adversary and sometimes use their expected attacks to beat them. Like shielding oneself from the siren song, one must be totally prepared, seek council before the journey (the trade) about what dangers are expected.

Like using a mirror against Medusa, one must plan against the adversary and sometimes use their expected attacks to beat them. Like shielding oneself from the siren song, one must be totally prepared, seek council before the journey (the trade) about what dangers are expected.

Also, it seems every entity in mythology had a weak spot. It's probably best to note these weaknesses in your thinking and in your emotions, not how can I beat the market, but how can the market beat me today?

Bill Rafter writes:

The greatest two rules:

(1) nothing to excess and (2) know yourself.

Pete Earle writes:

One lesson from mythology which resonates with me is the oracles/prophets/predictors almost always forecast correctly, but rarely in an obvious or immediately relevant way. The predictions made are usually realized, but not before taking extremely circuitous, and usually counterintuitive ways to reach fulfillment.

In my experience, predictions regarding the direction of equities or commodities inferred from option markets so often prove accurate…but only after traveling in the most wrong, most unanticipated ways.

Alston Mabry responds:

Pete, I think of that as "shaking the tree", i.e., we're gonna get there, but we're gonna shake out as many weak hands as we can along the way.

Pete, I think of that as "shaking the tree", i.e., we're gonna get there, but we're gonna shake out as many weak hands as we can along the way.

Peter Earle replies:

Absolutely. Stop-running and the like as the "gods" way of seeing who's "worthy"; who can withstand the flood, the fire, the sturm und drang.

Jim Lackey writes:

In 2008 I learned from Ryan Carlson– Sisyphus. There is a little useless book Wit and Wisdom from Wallstreet. So many of the quotes are the exact opposite from 3 pages ago… yet for a day they are seemingly sage advice. Worse for the long term. It's all good advice, yet in the mean time we must eat, and in the long term we all end up dust in the wind.

Traders lament when we miss profits. We are miserable when we lose. If we are not careful we are never happy. I have the habit of having to work myself up into a fury to win a race, pass a test or trade. My wife calls it "business mode" everyone else calls it being a jerk. Finally this year I have the ability to take a loss and this week miss a glorious rally and profit… yet at 4:20 PM its over. I am done pushing the boulder back up the hill for the day. I will return at 1:30am or by 7am, all but two business days a year. It can be torture if you do not like to trade, but if you love it…

Here is a quote from my kids music, "This is Our Science" by Astronautalis: "Our work is never done/ We are Sisyphus".

p.s I notice that if I don't like the rap beats I miss quite a bit of new poetry. I hear my teenagers say random lines and say what! That is amazing. Then I hear the song and say no wonder I never heard that line before. Damn drum machines.

Jack Tierney adds:

Recently I've been reading up on complexity, system dynamics, and the unpredictable consequences that occur when tinkering with non-linear systems. The markets seems subject to all and, if I'm even remotely correct in interpreting the literature, there's only one certainty: expecting linear consequences (e.g, provide banks with more liquidity, bringing about an increase in business borrowing, resulting in a resurgent economy) is rarely, if ever, realized.

Instead, the unseen effects on unimagined factors, almost always derails the logic train. A source I've referred to on occasion is "Cassandra's legacy." Appropriately enough, the custodian of that site provides an interesting historical allegory, in the form of Goth Princess/Roman Empress, Galla Placidia, and her part in the demise of the Roman Empire. It's a very lengthy read and, unless history like this interests you, tough going. So, a few highlights:

"Managing any large structure is difficult and we tend to do it badly; a whole empire may be an especially difficult case. To do it well, we would need to use a method what I mentioned before: system dynamics; which is a way to describe systems and the relation of the various elements that compose them.

"…every time that the Romans fought the Barbarians, they could win or lose, but each battle made the Empire a little poorer and a little weaker. The empire was using resources that could not be replaced; non-renewable resources, as we would say today….the solution was not more troops but less troops. It was not more imperial bureaucracy but less imperial bureaucracy, not more taxes but less taxes.

"In the end, the solution was right there and it was simple: it was Middle Ages. Middle ages meant getting rid of the suffocating imperial bureaucracy; it meant transforming the expensive legions into local militias; have people paying taxes locally, in short transforming the centralized empire into a decentralized constellation of small states. Without the terrible expenses of the Imperial court and of the Imperial bureaucracy, these small states had a chance to rebuild their economy and start a new phase of prosperity, as indeed it happened during the Middle Ages.

"What Placidia could do as an Empress was, mainly, to enact laws….It seems that Placidia was acting according to her style; ease the unavoidable, don't fight it….Placidia forbade the coloni, the peasants bound to the land, to enlist in the army. That deprived the army of one of its sources of manpower and we may imagine that it greatly weakened it. Another law enacted by Placidia, allowed the great landowners to tax their subjects themselves. This deprived the Imperial Court of its main source of revenues."

Stefan Jovanovich comments:

As much as King George's scribbler Edmund Gibbon despised Christianity, he had the Middle Ages even more because its bureaucracies were the worst of all — local and mean and stupid.

Professor Bard should revise his history. What he wrote here — "Middle ages meant getting rid of the suffocating imperial bureaucracy; it meant transforming the expensive legions into local militias; have people paying taxes locally, in short transforming the centralized empire into a decentralized constellation of small states. Without the terrible expenses of the Imperial court and of the Imperial bureaucracy, these small states had a chance to rebuild their economy and start a new phase of prosperity, as indeed it happened during the Middle Ages." - is nonsense.

The Roman Empire's tax collections were always "local"; that is why Roman politicians were willing to pay such enormous bribes to be appointed provincial governors. The legions were also "local"; the Empire's expansion came from granting "foreigners" - i.e. the people we would today call Spaniards, French and Syrians - the privileges of citizenship, which meant they were also qualified to serve in the local legions. This was equally true under the Republic; "crossing the Rubicon" would not persist as a bad metaphor if Rome's soldiery had been centralized.

As for economics, whatever the "terrible expenses of the imperial court", they were nothing compared to the ravages of coin clipping. The solidus of the Eastern Empire maintained an unchanged weight and measure for 4+ centuries - a record that is likely never to be broken. (It exceeds the span of sound money for the British Empire and the United States of America put together.) After Princess Placida's day coinage, under the wonderful decentralization of the Middle Ages, effectively disappeared.

"Dearth of provisions, too, increased by degrees, and the scarcity of good money was so great, from its being counterfeited, that, sometimes out of ten or more shillings, hardly a dozen pence would be received. The king himself was reported to have ordered the weight of the penny, as established in King Henry's time, to be reduced, because, having exhausted the vast treasures of his predecessor, he was unable to provide for the expense of so many soldiers. All things, then, became venal in England; and churches and abbeys were no longer secretly, but even publicly exposed to sale." - William of Malmsbury wrote this in 1140 AD - the period that Professor Bard praises so highly for its progress over the degeneracies of the Empire.

Hume deserves the last word on this and most other subjects that interested him.

"Mankind are so much the same, in all times and places, that history informs us of nothing new or strange in this particular. Its chief use is only to discover the constant and universal principles of human nature."

Easan Katir adds:

The Greeks have fooled people since the Bronze Age. Instead of a horse, they now have Trojan bonds.

Steve Ellison comments:

Jack, the Atlantic had an article about why projects that had successful pilots often failed when rolled out to the general population.

Why Pilot Projects Fail– Here are some excerpts:

Promising pilot projects often don't scale … Rolling something out across an existing system is substantially different from even a well run test, and often, it simply doesn't translate.

Sometimes the 'success' of the earlier project was simply a result of random chance …

Sometimes the success was due to what you might call a 'hidden parameter', something that researchers don't realize is affecting their test. Remember the New Coke debacle? …

Sometimes the success was due to the high quality, fully committed staff. …

Sometimes the program becomes unmanageable as it gets larger. You can think about all sorts of technical issues, where architectures that work for a few nodes completely break down when too many connections or users are added. …

Sometimes the results are survivor bias. This is an especially big problem with studying health care, and the poor. Health care, because compliance rates are quite low (by one estimate I heard, something like 3/4 of the blood pressure medication prescribed is not being taken 9 months in) and the poor, because their lives are chaotic and they tend to move around a lot … In the end, you've got a study of unusually compliant and stable people (who may be different in all sorts of ways) and oops! that's not what the general population looks like.

Dec

22

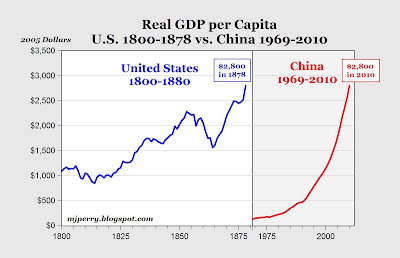

An Interesting Chart, from Leo Systrader

December 22, 2011 | Leave a Comment

I wonder if there is anything economic to be learned from this chart from Mark Perry's blog. The per-capita growth from 1810 to 1850 was more than 120% in 40 years. According to the wiki, by 1860, manufacturing (primarily limited to the Northeast) accounted for 30% of the nation's income, with cotton cloth production the leading industry. This indicates that some strong contrast/conflicts between the industrial northeast and the farming south existed.

I wonder if there is anything economic to be learned from this chart from Mark Perry's blog. The per-capita growth from 1810 to 1850 was more than 120% in 40 years. According to the wiki, by 1860, manufacturing (primarily limited to the Northeast) accounted for 30% of the nation's income, with cotton cloth production the leading industry. This indicates that some strong contrast/conflicts between the industrial northeast and the farming south existed.

Is it reasonable to believe that these economic conflicts were among the underlying causes for the eventual war?

Obviously the economic conflicts were the result of a fast and an uneven development. Perhaps it serves as a very valuable indicator for today.

Dec

16

Are Introverts More Gifted? from Leo Systrader

December 16, 2011 | Leave a Comment

I have heard that about 25 percent of the population are introverts, but as many as 60 percent of gifted children are introverts.

I have heard that about 25 percent of the population are introverts, but as many as 60 percent of gifted children are introverts.

I don't find this strange. But our understanding about the brain is too minimal to explain for instance the intrinsic links between being an introvert and being gifted. In addition, the concept of being gifted is very vague– it perhaps simply means that he/she can perform something somewhat better than an ordinary human.

With all these unknowns, many wonders often appear to us.

Dec

16

Housing, from Duncan Coker

December 16, 2011 | 1 Comment

One particularly nasty feature regarding the housing market which I am surprised to have seen no writing on is the treatment of capital loss. Losses on primary residences can not be deducted from other capital gains. What you eat, so to speak, you must pay tax again on making that capital back. Using a 20% tax rate of say 6 trillion in lost housing capital, that is roughly $1.2 trillion that the public will have to pay in incremental tax. (true if housing rebounds the loss may not be realized or incurred. Also true that some of the capital loss may be transferred to the banks if owner walk on the loan) But thinking like a politician and using government finance should they not include this potential for windfall tax receipts over the next decade or so as new "revenue". And why not just bring it all forward to 2012 and solve the whole budget gap for next year.

One particularly nasty feature regarding the housing market which I am surprised to have seen no writing on is the treatment of capital loss. Losses on primary residences can not be deducted from other capital gains. What you eat, so to speak, you must pay tax again on making that capital back. Using a 20% tax rate of say 6 trillion in lost housing capital, that is roughly $1.2 trillion that the public will have to pay in incremental tax. (true if housing rebounds the loss may not be realized or incurred. Also true that some of the capital loss may be transferred to the banks if owner walk on the loan) But thinking like a politician and using government finance should they not include this potential for windfall tax receipts over the next decade or so as new "revenue". And why not just bring it all forward to 2012 and solve the whole budget gap for next year.

Dec

15

The Legend of Bo Keeley Grows, from Art Shay

December 15, 2011 | 1 Comment

Here's a link to my article about Bo Keeley "The Legend of Bo Keeley grows". They or I got the photo credits goofed up. Sorry. Story comes out in NYC, SF, LA, Seattle, Austin, TX, DC, Chicago, Shanghai, London. Welcome home.

Here's a link to my article about Bo Keeley "The Legend of Bo Keeley grows". They or I got the photo credits goofed up. Sorry. Story comes out in NYC, SF, LA, Seattle, Austin, TX, DC, Chicago, Shanghai, London. Welcome home.

Ken Drees sends us a poem to honor Bo's welfare:

.

.

.

Bo Left Us Dead

(Written after reflection on good news of Bo Keely's safety)

Finished Bo's book, just put it down,

Next thing I hear

Sad tragic news,

Keely's not to be found.

No, not in anytown,

Got himself killed this time 'roun.

Them Mex think he's undercover narc,

Down there, too tall and off white

He sticks out,

One too many rides in the dark.

DocBo, The speculator surmises,

Has run plum out of lucky devices.

No facebook, email or phone, G*d please help Bo,

Sadly, its over for him;

No more of his stories, and that grin.

Please bring him back whole.

But if he's truly dead Lord,

Least his soul's in your yard.

Praying is over, Bo left us dead,

No more tales, rails or boxes

To inspire, tranfix,

To dazzle our heads.

Keely has jumped one reefer too far,

Somber, even the bulls at roundhouse bar.

And then like rain that drought licks for,

Bo's Alive for sure. For sure!

Been in the desert, all this time,

Playing with spiders, rocks, and slime.

Those mental puts on Bo expired,

Luckily not the man, that a freight train sired.

So comes the end of this tiny tale

Let the celebration begin,

Dead, now alive, its all win-win.

February's, cruel winter's gale,

Will no doubt herald,

A cupid hearted Hobo, quite undead sans peril.

Dec

14

Another Explanation for Webvan, from a Doctor Who Researches Stocks

December 14, 2011 | Leave a Comment

Some one was telling me they thought "shutting down Hillarycare gave us about 15 years of safety from the cancer that is big government intrusion into our lives. Repealing Obamacare could protect us for, possibly the rest of our lives."

Some one was telling me they thought "shutting down Hillarycare gave us about 15 years of safety from the cancer that is big government intrusion into our lives. Repealing Obamacare could protect us for, possibly the rest of our lives."

Our medical colleagues may not believe that. Insurance companies picked up the ball that Bill/Hill dropped (the meme that health care is too expensive) and turned free enterprise medical care into civil service (for the insurance companies).

The insurance bloc is government too.

Dec

7

No Lost Decade for S&P EW, from Kim Zussman

December 7, 2011 | Leave a Comment

Small cap stock out-performance explains at some or all of the equal-weighted SP500 out performing the cap-weighted version. The attached is the ratio of two tradeable ETF's: IWM (Russell 2000 stocks) and SPY (SP500 cap weighted), from May 2000 to present.

On a weekly-return basis, though IWM was was more than 2X higher than SPY they were not significantly different:

Two-Sample T-Test and CI: IWM week, SPY week

Two-sample T for IWM week vs SPY week

N Mean StDev SE Mean

IWM week 601 0.0016 0.0341 0.0014 T=0.6

SPY week 601 0.0006 0.0271 0.0011

Though as expected IWM did have significantly higher volatility:

Test for Equal Variances: IWM week, SPY week

95% Bonferroni confidence intervals for standard deviations

N Lower StDev Upper

IWM week 601 0.0320 0.0341 0.0364

SPY week 601 0.0254 0.0271 0.0289

F-Test (normal distribution)

Test statistic = 1.58, p-value = 0.000

Levene's Test (any continuous distribution)

Test statistic = 24.34, p-value = 0.000

Dec

7

Paying the Bill, from Anonymous

December 7, 2011 | 1 Comment

Nov

30

The Junto, from Alex Castaldo

November 30, 2011 | Leave a Comment

Economist David D. Friedman will be speaking on the use of free markets to solve difficult problems not usually thought of as market problems, on Thursday December 1, 2011 at General Society Library, 20 West 44 St., NYC, between 5th and 6th Aves, approx 7:30pm.

Nov

25

Grist for the Chair, from Scott Brooks

November 25, 2011 | 1 Comment

Vic recently stated that we were not in a range bound market. I have held that we are in a long term secular bear market since at least 2000, and one could make an argument that we've been in a bear market since 1998.

Vic recently stated that we were not in a range bound market. I have held that we are in a long term secular bear market since at least 2000, and one could make an argument that we've been in a bear market since 1998.

When I look at the S&P monthly closing values starting in Dec. 1998, I see a figure of: 1229

When I look at the S&P monthly closing values through October 2001, I see a figure of 1253

Eyeballing the chart, I see a high of around 1549 and a low of around 735 during that time frame. I see the high approached several times and the low approached several times.

How can we trade in the above range for the last decade+ and it not considered to be a range bound market?

I've always contended on this list that secular bear markets and secular bull markets each have certain characteristics that you see to help you recognize them.

Bulls have lower volatility and have a general upward trend. They do have pullbacks and crashes (i.e. the bull of 1982 - 2000 had the 1987 crash). But as a general rule of thumb, you can set your sails and just ride the bull winds to profits.

Examples of secular bulls include, the roaring 20s, the 1950s/60s, the 1980s/90s.

Bears have higher volatility (often much, much higher). They shot up and down but basically end up where they started and often end up where the started several times. You need to pull your sails down, turn on your engine and use a lot of energy to navigate the rough waters of the bear.

Examples of secular bear markets include, the Dust Bowl Years, the Great Depression, the 1970s, 2000 - ?

Not being a counter or someone with great math or statistical skills, I'm sure that there is a way to refute my point. I'd be interested in better understanding where I'm wrong and where I might be right.

Steve Ellison writes:

Mr. Brooks has suggested that it is better to invest when stocks are in an upward trend with low volatility and to stay away when stocks are in a downward trend with high volatility.

Since Mr. Brooks is talking about very long periods, I used S&P 500 index data back to 1950 and Dow Jones Industrial Average data from 1928 to 1949. For each day I calculated a sort of normalized 1-year VIC: the average of the daily absolute percentage changes over the past year. Beginning on the day after Pearl Harbor, I determined the median 1-year volatility of all the previous dates. Thus, using data that could theoretically have been known at the time, I classified the 1-year volatility each day as high or low.

If the index was higher than a year previously, I categorized the trend as up; otherwise the trend was down.

I considered a bull market to be in effect if the previous day's close was higher than the close a year earlier and the previous day's 1-year volatility was below the historical median. I considered a bear market to be in effect if the previous day's close was lower than the close a year earlier, and the previous day's 1-year volatility was above the historical median. I considered all other days to be neutral.

By this method, a bull market was in effect continuously from March 12, 1992 to March 30, 1994. The market then flipped several times between bullish and neutral as volatility was low, but prices in 1994 sometimes dropped below year-earlier levels. The market was then continually bullish from February 7, 1995 to March 31, 1997. The market then moved to neutral status as volatility rose. Except for two days in October 1998 when a bear market was in effect, the market was neutral until November 10, 2000, when it moved to bearish. It stayed bearish for all but 6 days until June 2003. There was a continuous bull market from July 12, 2004 to October 26, 2007.

There was a continuous bear market from January 14, 2008 to October 7, 2009. Then the market was neutral (up trend but high volatility) until August 9, 2011. It was bearish for one day and then flipped back to neutral. There have been a few more flips between neutral and bearish, and after Wednesday's close, this indicator has again flipped from neutral to bearish.

Using this method to contemporaneously identify bull and bear markets, I got the following results since 1941.

Number Average Value of $1000

Type of market of days daily return invested on these days only

Bull 8118 0.034% $16335

Bear 2872 0.018% $1695

Neutral (downtrend 2163 0.004% $1094

but low volatility)

Neutral (uptrend 4463 0.031% $3933

but high volatility)

It does appear that investing in contemporaneously recognizable bull markets is better than investing in bear markets. But wait–is that just by random chance? For example, see the following graph of the cumulative results of 300 coin flips. The underlying process is completely random, but there appeared to be a long heads trend, followed by a Fibonacci retracement.

To answer this question, I ran 500 simulations in which I randomly chose 8118 of the daily returns since 1941. I then compared the total returns of these random selections to the total return of the 8118 bull market days. The actual return of the bull market days was in the 82nd percentile of the randomly generated 8118-day returns. Thus, I estimate the outperformance of bull market days has p=0.18 and falls short of statistical significance.

Charles Pennington writes:

I think Scott is saying that the market has been bounded ON THE UPSIDE, never going much above 1500 at any time over the past >10 years, although bumping up against that level a few times.

"Range bound" should mean that the market is tightly bound both on the upside and the downside–it has a tight RANGE. I think that when Vitaliy wrote his book, he was expecting that the market would have a true tight range going forward, and his readers might fairly have concluded it would be a good idea to sell some puts and calls to capitalize on the forthcoming tight range. Instead, of course, the market fell 50%. So Vitaliy re-interpreted his prediction to mean "bounded on the upside".

Victor Niederhoffer comments:

Yes. The professor has captured the gist of the promotion and huckstering and conversion of property and putting on the pretty face to hook the rich so typical of those raised in that environ that caused one to boot him off the site.

Anatoly Veltman writes:

May I twist the subject slightly…

We all remember Greenspan's only explanation of unusually long subdued inflationary pressures over the 90s decade and into the 00 decade: super-efficiency, labor achievements. And then came the real-estate bubble.

Bernanke's issue appears more deflation than inflation. However, the redistribution of means achieved politically creates somewhat of an asset bubble relative to real economy.So remembering that market is never favorite to go down, I'm still struggling with these fears: what if market's only nominal robustness is purely a devaluation phenomenon? Is equity investment then justified, or is some sort of hard-money is just as well (not gold necessarily– maybe oil, gas, agri commodities)?

Paolo Pezzutti writes:

Hmm…. Maybe gold or oil? It does not seem that for the moment gas is appealing to investors. That is why I decided to buy it, contrarian as usual, and UNG went down from12$ to 8$. And when I bought it I was thinking that it could not possibly go lower given the steep fall already printed. After all gas is something tangible and oil was relatively much more expensive. Who knows, may be things will change when someone will demonstrate that shale fracturing techniques damage the environment. If this downtrend continues soon they will gas for free at the corner of the Streets…

Bruno Ombreux comments:

I don't understand this concept of "investing" in a commodity.

A commodity is meant to be produced then consumed. How can anyone invest in that? It does not pay an interest or a dividend. You eat it, burnt it… Just taking one extreme: power. It is not storable. Supply must equal demand all the time.

I cannot think of anybody idiot enough to invest in commodities except hedge funds, who are really idiots.

No?

p.s. Gold is the only exception. Some people say it is a commodity. I do not agree but let us accept this to avid a semantic debate. You cannot invest in it but it is money. So you can buy it and keep it. But you don't really "invest" in gold.

Just to be clear, one can "speculate" in a commodity, as long as it is storable. As Keynes brilliantly showed, the economic role of the speculator is storage. So not only can you "speculate" but also you make the world a little bit better. But "invest"? Come on…

Gibbons Burke replies:

Gary North, in an ebook he provides for free on his website, has an interesting description of times when commodities become money:

Gary North, in an ebook he provides for free on his website, has an interesting description of times when commodities become money:

Now let’s take a real historical example, the famine era in Egypt. Joseph had warned the Pharaoh of the famine to come, and for seven years, the Pharaoh’s agents had collected one-fifth of the harvest and had stored it in granaries. Then the famine hit. The crops failed. The people of nearby Canaan also suffered. No one had enough food.

And Joseph gathered up all the money that was found in the land of Egypt and in the land of Canaan, for the grain which they bought; and Joseph brought the money into Pharaoh’s house. So when the money failed in the land of Egypt and in the land of Canaan, all the Egyptians came to Joseph and said, “Give us bread, for why should we die in your presence? For the money has failed” (Genesis 47:14-15).

What did they mean, “the money has failed”? They meant simply that compared to the value of life-giving grain, the money was worth nothing. Why would a man facing starvation want to give up his remaining supply of grain in order to get some money? What good would the money do him? He wanted life, not money, and grain offered life.

Because the money “failed,” it had fallen to almost zero value. Thus, in order to buy food, the people had been forced to spend all of their money. Now they were without food or money.

And Joseph said, Give your livestock, and I will give you bread for your cattle, if the money is gone. So they brought their livestock to Joseph: and Joseph gave them bread in exchange for the horses, the flocks, the cattle of the herds, and for the donkeys. Thus he fed them with bread in exchange for all their livestock that year (Genesis 47:16-17).

Were the Egyptians foolish? After all, all those cattle and horses were useful. But animals eat grain. The grain was too valuable during a famine to feed to animals. All that the animals were worth was whatever they would bring as food, and in Egypt, the meat wouldn’t last long. Dead animals in a desert country don’t remain valuable very long. Why not trade animals for grain, which survives the heat? The only reason the Pharaoh had any use for the animals and money is that he knew he had enough food to survive the famine. He knew that it would eventually end. Thus, he would be the owner of all the wealth of Egypt at the end of the famine. For him, the exchange was a good deal, but only because he had the food, and the army to defend it, and he also possessed what he believed to be accurate knowledge concerning when the famine would end. Joseph had told him it would last seven years.

Because he had a surplus of grain beyond mere survival, and because he had “inside information” about the duration of the famine, money and animals were valuable to the Pharaoh, even though they were not valuable to the people. Thus, a voluntary exchange became profitable for both sides. The Pharaoh gave up grain for goods that would again become very valuable in the future. The Egyptians gave up goods worth very little to them in the present in order to get absolutely vital present goods. Each side gave up something less valuable in exchange for something more valuable. Each side improved its economic position. Each side therefore gained in the transaction.

Notice here that we are not dealing with any so-called “equality of exchange.” This theory says that people exchange goods only when the goods are of equal value. It is true that in the marketplace, they may be of equal price, but they are not of equal value in the minds of the traders. What we are always dealing with in the case of voluntary exchange is inequality of exchange. One person wants to possess what the other person has more than he wants to keep what he already has. Because each person evaluates what the other has as more valuable, a voluntary exchange takes place.

Egypt’s money failed. In fact, grain became the new form of money, although the Bible doesn’t say this explicitly. What it says is that everyone was willing to trade whatever he had of former value in order to buy food. But if some item is what everyone wants, then we can say that it’s the true money.

The Properties of Money

Why would grain have served as money? Because it had the five essential characteristics that all forms of money must have:

1. Divisibility

2. Portability

3. Durability

4. Recognizability

5. Scarcity (high value in relation to volume and weight)Normally, grain doesn’t function as money. Why not? Because of characteristic number five. A particular cup of grain doesn’t possess high value, at least not in comparison to a cup of diamonds or a cup of gold coins. The buyer thinks to himself, “There’s lots more where that came from.” Normally, he’s correct; there is a lot more grain where that came from. But not during a famine.

Why divisibility? Because you need to count things. Five ounces of this for a brand-new that. Only three ounces for a used that. Both the buyer and the seller need to be able to make a transaction. The seller of the used “that” may want to go out and buy three other used “thats” in order to stay in the “that” business, so he needs some way to divide up the income from the initial sale. This means divisibility: ounces, number of zeroes on a piece of paper, or whatever.

Portability is obvious. It isn’t an absolute requirement. I have read that the South Pacific island culture of Yap uses giant stone doughnuts as money. They are too large to move. But they are a sign of wealth, and people are willing to give goods and services to buy them. Actually what are exchanged are ownership certificates of some kind. Normally, however, we prefer something a bit smaller than giant stone doughnuts. When we go to the market, we want to carry money with us. If it can’t be carried easily, it probably won’t function as money.

Durability is important, too. If your preferred money unit wears out fast or rots, you have to keep replacing it. That means trouble. A barrel of fresh fish in a world without refrigeration won’t serve as money. But there are exceptions to the durability rule. Cigarettes aren’t durable the way that metal is, but cigarettes have functioned as money in every known modern wartime prison camp. Their high value per unit of weight and volume overcomes the low durability factor. Also, they stay scarce: people keep smoking their capital.

Recognizability is crucial if you’re going to persuade anyone to trade with you. If he doesn’t see that it’s good, old, familiar money, he won’t risk giving up ownership of whatever it is that you’re trying to buy. If it takes a long time for him to investigate whether or not it’s really money, it eats into everyone’s valuable time. Investigations aren’t free of charge, either. So the costs of exchange go up. People would rather deal with a more familiar money. It’s cheaper, faster, and safer.

So what we say is that any object that possesses these five characteristics to one degree or another has the potential of serving a society as money. Some very odd items have served as money historically: sea shells, bear claws, salt, cattle, pieces of paper with politicians’ faces on them, and even women. (The problem with women is the divisibility factor: half a woman is worse than no woman at all.)

Rocky Humbert disagrees:

I'm not going to waste everyone's time articulating why Mr. Bruno is wrong. (You can find that in any reasonable textbook.) I will simply note that ALL investments (including commodities) have many complex and related attributes, including replacement cost, store-of-wealth, scarcity value, Graham & Dodd "margin of safety," and of course, cash flow and future expected value. (If Bruno doesn't understand how to derive cash flow and future expected value from a commodity and/or commodity futures investment, I'll be more than happy to tutor him at an hourly fee that appropriately compensates me for my annoyance in having to deal with a pompous windbag.) Whether one is "investing" (or "speculating") in a start-up company in someone's garage, in a T-bill (with a negative real return), in natural gas (which is trading below its fully-loaded marginal cost of production), in aluminum (which may have a worldwide supply deficit), in Groupon (because eventually they will make a profit), in BAC (because it's trading below Book value)….etc, etc, etc., the discipline, analysis and approach are consistent.

I have to hand it to Mr. Bruno — he now has two things in common with my brilliant wife. They both enjoy fine French wine, and they both think I am an "idiot." (The similarities end there — since my wife knows that California produces some wines that embarrass the French Premier Cru's — and she also knows that those with an IQ between 51 and 70 are "morons;" whereas "imbeciles" possess an IQ between 26 and 50. She sadly knows that as a hedge fund manager, I live in the "tail" of the distribution — as "idiots" have an IQ between 0 and 25.

Bruno Ombreux replies:

I am not going to retract. I think the hedge funds who say they invest in commodities are idiots. If they are not idiots they are crooks which is even worse.

You cannot invest in a commodity. If you present it as an investment, there are two possibilities:

1) You do not know it is not an investment, and then you are an idiot.

2) You know it is not an investment, and then you are a crook.

And I am sorry, I met many people from hedge funds. It is true they are nice people and sometime extremely clever, if often a bit naive. But the are not competent in trading commodities. They are clever marketers. That is they are clever at raising money. But most of them suck as traders or investors.

I wouldn't blame them if they took exception to your comment and demanded that you be keelhauled then ordered to buy a round of drinks for all. I know a couple hedge fund managers on the list and they seem to be the smartest people I've ever had the occasion to know.

Nov

22

US Debt and Europe, from P. Humbert

November 22, 2011 | 2 Comments

A debt-reduction committee with special powers that was supposed to dissolve congressional gridlock in Washington is instead on the brink of failure, setting the stage for $1.2 trillion in automatic spending cuts.

A debt-reduction committee with special powers that was supposed to dissolve congressional gridlock in Washington is instead on the brink of failure, setting the stage for $1.2 trillion in automatic spending cuts.

Finally. Hopefully the US will show the Europeans that solving the economy problems by just issuing new debt is not an option. Markets have just reacted printing higher prices for EURUSD. It seems that the Euro continues to be relatively strong despite the situation in Europe.

How long can the markets be blind and not see the obvious?

Signed,

a frustrated short on the Euro.

Nov

8

An Strange Question, by Kim Zussman

November 8, 2011 | 2 Comments

Why would people PAY the government to take their money?

WSJ: Paying to Give U.S. Money? Some Like Idea [registration may be required]

By MIN ZENG

With yields plummeting on U.S. government bonds, the Treasury Department has quietly asked some banks if they would agree to buy new short-term bills offering yields below zero.

Effectively, the Treasury is asking investors if they are willing to pay the government to take their money. And some big banks have answered, "Yes."

It may sound crazy, but yields on Treasurys of less than three-month maturity are already occasionally trading below zero in the secondary market. Under current auction rules, though, the Treasury can't sell so-called T-bills with a negative yield. In the bond market, however, higher yields mean lower prices, so the Treasury is effectively losing out every time it sells bills with higher yields than the prevailing level in the market.

The question was included in a questionnaire the Treasury delivered on Oct. 14 to the 22 primary dealer banks that are obligated to bid on primary auctions of its debt.

[…]

Gibbons Burke comments:

It is just another form of protection racket. For a small tribute, you can keep your money.

Victor Niederhoffer comments:

The banks are so indebted to the government for their survival and bonuses and trading and purchase of distressed assets, and redeeming of sovereign debt, and capital at the funds rate, and bailouts, and investments et al , and freedom out of hotels that they are happy to accommodate their masters on the Hill with any emoluments like paying the master a fee for the privilege of holding the master's…

Oct

19

Comparing Two Mountains, from Victor Niederhoffer

October 19, 2011 | 7 Comments

Dear Steve,

Hope you are well. A statistical problem has come up. The idea of comparing two charts, in this case Netflix and Green Mountain Coffee. I wonder if statisticians have a way of handling this problem. I've seen some books on statistics on place but never this problem of comparing two mountains as to their similarities. I wonder if you could refer me to the proper area. I asked a geologist whether they have a way, and apparently they take into consideration many physical factors. I am going to enclose the chart separately.

Stephen Stigler replies:

Hi Vic,

Any statistical model would have to have a dynamical model for the mountain. It could be an empirical model, like if you had a sequence of mountains, as with predicting sunspot cycles or tides. But it would either need a number of examples (not just two) or a very strong math hypothesis. You might be able to generate a set of examples if you focus on a telling feature, like one day descent of x% after trading within + or - y% for z days.

Hope all is well with you & yours!

Best,

Steve

Pitt Maner comments:

A geomorphologist would have to consider many factors in trying to interpret how the hills and valleys were formed, the timing of such, and what they might look like in the future. Erosion is a key but it can occur at differing rates within a range of timescales based on rainfall, climate, vegetation, composition and homogeniety of the rocks, fractures, landslides, river sediment carrying capacities and as noted in the article below—Slope . There are instances, however, where the rate of erosion at the surface is offset by the continuing forces of uplift (denudational isostatic rebound for word lovers).

There are rules of thumb— with the higher slopes and steep mountain ridges eroding quite quickly —E. Himalayas at a whopping 2 to 3 mm/yr, as example. But those erosional rates will change over time to meet new equilibrium requiremen ts.

"I don't think we'll ever find the single smoking gun of erosion," says Portenga, "the natural world is so complex and there are so many factors that contribute to how landscapes change over time. But as this method develops, we will have a better sense of what variables are important — and which are not — in this erosion story."

For example, it has been a truism of geology for decades that rainfall is the biggest driver of erosion. Semi-arid landscapes with little vegetation and occasional major storms were understood to have the greatest rates of erosion. But this study challenges that idea. "It turns out that the greatest control on erosion is not mean annual precipitation," says Bierman. Instead, look at slope.

"People had always thought slope was important," Beirman says, "but these data show that slope is really important."

Oct

17

Deception Theory, from Victor Niederhoffer

October 17, 2011 | 10 Comments

I am reaching a point where I am frequently asked to give lectures on markets, a point usually related to about 3 to 5 years before one receives a bevy of awards, which is usually a year or two from the awarder's estimate of your death. I think I will try to develop a theory of deception from biology and game theory that will substitute for my usual talk on music and markets, which takes tremendous physical and financial resources, and is similarly poignant to the audience.

Alan Millhone comments:

Dear Chair

Most master checker players notate (record moves) while playing. A few would write down the wrong move and let their opponent see what they record on their game sheet — then they move elsewhere. I can see where this might disrupt their opponents thoughts.

Are there traders who position one way for all to see then do otherwise ?

Sincerely,

Alan

Anatoly Veltman writes:

Within the 1980s COMEX floor hierarchy, there was the Price Committee. Say, Gold traded 364.0-364.5 closing range. If I were going home short, I'd ask my influential broker, who was on that committee, to make sure day's settlement price is fixed at 364.2; if I were Long, I'd ask for 364.3. Sounds trivial– but when I carried 3,000-lot positions, it would put instant $30,000 in my pocket, day into day. I can only imagine shenanigans in the OPTIONS after-pit, where they settled hundreds of different strikes daily– and some might have carried 50% price discretion!

In any case, here comes the punchline: shrewd floor operators, who didn't carry overnight positions but loved to push Gold around during pit trading– kept tab of post-bell haggling. One fateful day, seeing Gold gap way against my position, they kept pushing the trend all day just to cause me margin liquidation. That one-day loss swallowed all of the settlement-print windfall collected for the year.

Jordan Low adds:

In Blink by Malcolm Gladwell, a game of chance drew cards from two piles. The bad pile that lead to losses was avoided at some point consciously, but the subconscious detected that pattern before the conscious. I, of course, tried to measure my sweat, heart rate etc before each trade. Am I deceiving myself on an opportunity when I am just trying to get a gambler's high? I couldn't find anything useful except that hearing the news is negative to my process. Reading subtitles and skipping the music is probably better. Perhaps there might be technology to read the general emotions on TV using facial recognition one day.

Jack Tierney, the President of the Old Speculator's Club writes:

This idea of yours, Victor, reminded me of a book I recently finished, River of Doubt. It's an interesting account of Teddy Roosevelt's post-presidential, near-fatal adventure into unknown portions of the Amazon. While much of the story revolves around the encounters, challenges, and actions of the discovery team, significant portions tell an interesting story of Amazonian flora and fauna adaptations.

Some of these occur over large portions of the region, others might exist in an area measured in square yards– almost all, though, occur with incredible rapidity and are developed to attack very specific prey. As one might expect, within another very short period of time, it, too, is the prey of a newly evolved predator.

Of the different adaptations briefly encountered in the book, the one that aroused my curiosity the most is called "masting." I had never before heard the term and subsequently looked it up and did a little research:

Mast is a noun… that refers to the accumulation of various kinds of nuts on the forest floor that serve as food for… animals. The process… is known as masting…. it is not a continuous process, but rather is cyclic. Approximately every three to five years certain trees produce prodigious quantities of nuts; in between the "masts" they will produce almost none. "There are two elements of the economy of scale hypothesis for masting variability: First, predator satiation - by producing a gargantuan nut crop, the predators become satiated [and enough] nuts will survive to succeed in propagation. The predator population is held in check during the non-mast years. Second, [p]ollination efficiency - masting trees are wind-pollinated…from staminate to pistillate flowers, a rather precarious and random process…it is therefore advantageous for them to fill the air with pollen from many trees at the same time.

The masting trees' surreptitious and unpredictable flowering, as well as the feast-or-famine results experienced by its "predator" classes might parallel some of the actions/consequences of the flexions as they periodically feed and starve the lesser fuana.

Oct

17

Big Reversals, from Kim Zussman

October 17, 2011 | Leave a Comment

In SP500, the last two calendar weeks rose about 8.2% and the prior two weeks dropped by almost 7%. Going back to 1950, identified 14 instances in which two consecutive up-weeks gained at least 5% (for two weeks), and the prior two weeks were both down and lost at least -5% (for two weeks).

For these 14 big reversals, here are the following two week returns:

One-Sample T: dip 2W

Test of mu = 0 vs not = 0

Variable N Mean StDev SE Mean 95% CI T P

dip 2W 14 0.0183 0.040 0.0106 (-0.0046, 0.0412) 1.73 0.108

10/14 up, but NS vs zero due to high variance. One notes the prior instance marked a long term bottom March 2009:

Date dip 2W

03/16/09 0.096

01/28/08 -0.033

10/14/02 0.019

10/01/01 0.002

10/19/98 0.066

12/14/87 -0.008

08/16/82 0.085

10/05/81 -0.023

12/22/80 -0.023

10/14/74 0.022

07/13/70 0.005

10/17/66 0.034

12/02/63 0.004

07/02/62 0.011

Oct

17

Thoughts on HFT, from Gordon Haave

October 17, 2011 | 3 Comments

How is it a boon to investors to get screwed on every transaction by people with better information? Mind you, it's not that they worked harder for more information about a companies prospects, they just paid a lot of money to get an unfair edge.

I know the standard response is "liquidity" but I also know that such liquidity disappears the second the "liquidity providers" aren't guaranteed profit. The normal justification for the money earned for providing liquidity is that it is a service and that risk is incurred.

With HFT it's just a guaranteed screwing over of everybody.

And people wonder why investors are buying gold and silver.

Oct

17

IBM THINK Exhibit at Lincoln Center, from Chris Tucker

October 17, 2011 | Leave a Comment

For those New Yorkers that haven't seen it, there is an interesting IBM exhibit in Lincoln Center.

For those New Yorkers that haven't seen it, there is an interesting IBM exhibit in Lincoln Center.

Located on Jaffe Drive at Lincoln Center in New York, the THINK exhibit combines three unique experiences to engage visitors in a conversation about how we can improve the way we live and work. Data wall

Visitors approaching the exhibit are drawn in by striking patterns displayed on a 123-foot digital wall. The wall visualizes, in real time, the live data streaming from the systems surrounding the exhibit, from traffic on Broadway, to solar energy, to air quality. Visitors discover how we can now see change, waste and opportunities in the world’s systems. Immersive film

Inside the exhibit space, visitors step into a media field composed of 40 seven-foot screens. As the screens come to life, visitors discover a 12-minute immersive film. A kaleidoscope of images and sound surrounds them. They are enveloped in a rich narrative about the pattern of progress, told through awe-inspiring stories of the past and present. They are inspired to think about humankind's quest for progress, and about making our world work better, today. Interactive experience

At the conclusion of the film, the 40 media panels become interactive touchscreens, transforming the space into a forest of discovery. Visitors can explore our quest to see more—from clocks and scales to microscopes and telescopes, RFID chips and biomedical sensors. They learn how maps have been used to track data, from early geographical maps to the most recent databases and data visualization platforms. They interact with the models used to understand the complex behaviors of our world—from weather prediction algorithms to virus spread simulations. They hear from leaders of world-changing initiatives about how they built belief. And they read about some of the most inspiring examples of systemic progress around the world. Each touchscreen also gives visitors the opportunity to provide their point of view and learn what others are thinking.

Oct

17

Article of the Day, from Jeff Watson

October 17, 2011 | 1 Comment

This is an article about a 100 year old man completed a full marathon in Toronto. What more can one say about this uplifting, heart warming feat.

Oct

17

Life Expectancy Indicator, from Victor Niederhoffer

October 17, 2011 | Leave a Comment

A good way of estimating someone's life expectancy is by the frequency and number of awards he receives.

Gibbons Burke adds:

A friend observed, after my uncle, international champion at the age of 20 and an Olympic Gold Medalist (Sailing, Acapulco, 1968), tactician for Ted Turner, drinking pal of fellow Star-boat sailors the kings of Greece and Spain, and frequent collector of silver trophies in Gulf Coast regattas his entire life, dropped dead one Monday morning of a heart attack at the age of fifty:

"Everyone is allotted a certain number of heartbeats… Buddy lived in such a way that he used up his quota."

Oct

17

The Film Indicator, from Stefan Jovanovich

October 17, 2011 | Leave a Comment

The Three Musketeers (1921 film), a 1921 silent film version starring Douglas Fairbanks

The Three Musketeers (1921 film), a 1921 silent film version starring Douglas Fairbanks

The Three Musketeers (1935 film), a black and white RKO version featuring Walter Abel

The Three Musketeers (1939 film), a comedic version starring Don Ameche and the Ritz Brothers

The Three Musketeers (1948 film), an MGM production starring Gene Kelly, Van Heflin, Lana Turner, and June Allyson

The Three Musketeers (1973 film), and The Four Musketeers (film) (1974) a two-film adaptation starring Michael York, Oliver Reed, Frank Finlay, and Richard Chamberlain

The Three Musketeers (1993 film), a Disney production starring Charlie Sheen, Kiefer Sutherland, Chris O'Donnell, Oliver Platt, and Tim Curry

The Three Musketeers (2011 film), a 3D version of the film starring Logan Lerman, Ray Stevenson, Luke Evans, Christoph Waltz, Orlando Bloom, Milla Jovovich, Matthew Macfadyen.

Oct

17

Carolina Gold Rush, from Pitt Maner III

October 17, 2011 | Leave a Comment

It is conceivable that many long forgotten mineral and metal prospects in Georgia and Alabama and other southern states are now undergoing re-evaluation given improved techniques for assessing the extent, composition, geometry and economic value of ore bodies.It would seem to be a highly speculative field not without significant risks. Not an area for persons susceptible to hyperbole.

1) "A Canadian mining company and a tiny South Carolina town are leading what could be a modern gold rush to the southeastern United States."

These technical reports give an idea how these gold and metal deposits (some abandoned during the gold rush to California in 1849) are looked at today.

3) Chris Tucker mentioned mica and I remember quite vividly as a boy seeing large areas of ground near Rockford, AL shimmering with light reflected from small pieces of muscovite while hunting mine "spoil piles" for beryl crystals with my father.

There are "potential" pockets of minerals (pg 25 of linked document) all within and along the southern end of the Appalachian Mtns. Various regulations probably impact whether some of these deposits can be mined for profit.

http://www.gsa.state.al.us/documents/misc_gsa/IS64RMinerals.pdf

Oct

5

Bloomberg: U.S. Stocks Rise as S&P 500 Jumps in Final Hour, by Steve Ellison

October 5, 2011 | Leave a Comment