Apr

4

The main attribute for a successful CEO these days is to be a good beggar. The good beggar has to pretend that without the alms, he would be totally helpless. Also that he previously did very good work.

The main attribute for a successful CEO these days is to be a good beggar. The good beggar has to pretend that without the alms, he would be totally helpless. Also that he previously did very good work.

The big CEO's who clustered around the treasury and were able to beg trillions from the fed and the treasury to ward off bankruptcy in those days were masters at this. The training in beggary was not limited to the US CEO's who brought up the terrible calamity of the Reserve fund breaking the buck (with the potential unrealized loss of 100 million the holders of their 5 billion). But the Europeans were even bigger borrowers than the US banks and companies. The ability to pledge about a trillion of worthless assets to the Fed to get loans when they were on the ropes is something that will have repercussion undreamed of and unintended for many generations. Mainly it reduces incentives, and makes you want to throw in the towel.

The training for CEO's these days should be a course in how to beg. I'm told you have to pretend to be productive, willing to work, and well dressed. Presumably having been previously employed by the alms giver or having a job for him or his family in the future is also helpful (the palindrome always told me that whenever he went to Washington the first thing that the operatives wanted to know was whether their son made a good impression when he applied for a job). A reading of Bertold Brecht and listening to Kurt Weil in the Three Penny Opera would be recommended. A trip to India with a required visit to the museum of Thuggery, to study their methods would also be in order.

Wouldn't this be better than the required courses at the HBS that now displace so much more fruitful learning in how to beg that the most successful CEO's should take.

How could this all be quantified, and what profit making opportunities are suggested by this?

T. Humbert writes:

The above echoes some parallels about how the revenue model of the Church operates. In such, the pastor acts a "collector" of sorts, though his methodology of addressing (read: creating) accounts receivable is a little more subtle than that of the traditional practitioners of that old-world craft.

Rather than the overhand rights and nastily-swung bats of the rough-and-tumble boys, the most effective of the Roman collar guys eloquently whack one senseless if otherwise unscathed with the moral imperative thing to best ensure compliance with donation terms.

And always when others are around so as maximize peer pressure leverage of a most compelling nature.

P.S. I'm on an Amtrak tonight slowly rolling from NY to San Francisco. I don't mind flying at all, but I love trains. How it costs 3x more than a jet ride that could get one there in a tiny fraction of the time I have no idea….Oh, that's right, the government runs the trains…Silly me.

Tim Hesselsweet writes:

Different tax rates for different companies/industries and the nature of the provision/loophole that influenced it.

Subsidies for agriculture

Energy subsidies: see this link for 1995 article

Tax write-offs that support tech

Financial bailouts (overt payments + benefits to front-running fixed income in tarp etc.) + is there a cost of capital advantage to being to big to fail in public markets

I doubt there's much regulation of consumer related business, but there is for financial, energy, defense, health care. Quant measure would be federal agencies overseeing industry, the more oversight the more big cap favored over small cap.

Knowledge of legislation and tax treatment best. Tax rate is one proxy for legislative advantage but that doesn't account for subsidy or other measures that create unequal playing field.

Apr

4

Flexionic Rankings, from Victor Niederhoffer

April 4, 2011 | Leave a Comment

We need a systematic ranking of companies by the flexionism of their CEO's and then we can quantify and look at future performance which of course in the past is highly correlated positively, but with our baedecker maybe the situation will change.

We need a systematic ranking of companies by the flexionism of their CEO's and then we can quantify and look at future performance which of course in the past is highly correlated positively, but with our baedecker maybe the situation will change.

Gary Rogan writes:

Flexionism is a two-edged sword. As much as it helps companies, it also hurts some in a similar way that "low-income" welfare eventually ruins its recipients. I've never researched this statistically, but I concluded for myself early into the current flexionic golden age that sheer size matters more than before. A company has to have critical size to be able to protect itself against the government by fighting back, bribing, or pure flexionic behavior, and in a less significant way amortize the cost of compliance with regulations over a larger productive base. In the good old days size helped too by making the company stronger in many ways, but also hurt by making it a target and also reducing it's ability to react to change. All these things remain, but the necessity to deal with the aggressive, totalitarian-lite government is shifting the balance, in my opinion, towards very large companies.

Russ Sears writes:

When your worth is built on your political contribution, you can quickly be thrown under the bus when the winds change directions. Size brings more internal enemies and jealous and greater chance of collapse from within.

Gary Rogan replies:

True. My point really was that size is less fleeting than flexionism when the winds suddenly change. From this perspective I prefer Pepsi to GE: both are large and quite flexionic, but Pepsi will not collapse when the government turns away from wind turbines and financial bailouts.

I strongly agree that a large multinational has a lot of advantages these days, being able to escape the reach of the US government and not as exposed to its collectivist policies are more important than ever. Those who use flexionism as a defense strategy are preferable to those who are actually living the flexionic life at the core of their business. He who lives by flexionism will eventually die by it, but simply saying the right things in the right places is likely to be less traumatic long term, when things change, they'll start saying something else.

Apr

4

The Village Idiot, from Victor Niederhoffer

April 4, 2011 | 1 Comment

One is reminded of Victor Hugo's The Man Who Laughed where people in Spain, one believes in the 13th century, (albeit Cervantes didn't write about it) were purposely deformed and trained as deformed so that the rest of the population would not succumb to envy of the flexions or in general be unhappy with their relative lot. Perhaps Mr. Jov will set the record straight.

One is reminded of Victor Hugo's The Man Who Laughed where people in Spain, one believes in the 13th century, (albeit Cervantes didn't write about it) were purposely deformed and trained as deformed so that the rest of the population would not succumb to envy of the flexions or in general be unhappy with their relative lot. Perhaps Mr. Jov will set the record straight.

Art Cooper writes:

Here is a link to the Monty Python skit in which John Cleese plays an Oxford-educated village idiot. When a villager walks by, Cleese acts like a mentally-defective clown. When no one else is around, Cleese speaks to the camera in a highly educated tone, explaining the importance & usefulness of the traditional village idiot to the mental well-being of other villagers.

Bo Keely writes:

One must study the village idiot to discover just what cards he holds. Every town has its hunchback, dwarf, ostensible retard or combination who is the resident savant. Here in Toba, Sumatra it is a cerebral-palsied man sitting next to me doing the town accounts on the computer. In your post 'Grassroots Jungle Economy' the village idiot poisoned the town like Sweeney Todd with coconut sweets from his sewage fed coconut tree. In 'Village Idiot' the hunchback in the key Surfactio, Mexico RR junction is the secret liason to a daily dozens of illegal Central Americans riding the Mexican freights to milk the USA economy. Anyone pushed by a physical or mental deformity from out under the Bell Curve is to be seriously reckoned with.

Apr

2

The Million Dollar Story, from Victor Niederhoffer

April 2, 2011 | 2 Comments

The musical and movie Billy Elliot is the perfect musical for our age. In terms of its guaranteed to make a million nature. Here are the main characteristics.

The musical and movie Billy Elliot is the perfect musical for our age. In terms of its guaranteed to make a million nature. Here are the main characteristics.

It shows Margaret Thatcher and conservatives to be mean spirited and stupid. It portrays business in a very bad light, as all the coal companies seem to be interested in is profits and exploiting the workers. Despite the plight of the workers, the coal company tries to displace attention by claiming it's a clean energy company. It portrays gender equality and cross dressing in a highly favorable light. It has kids in the first scene and last scene dancing and singing. The music and dance flows naturally out of the activity because the story is about a kid who wants to be a dancer. It has raucous loud music by Elton John that is part and parcel of the generation that wears ear phones all day to listen to rock music on their phones or computers. It shows the workers to be kind hearted souls, who would sacrifice anything to do a good turn, like giving up their meals to send Billy to the royal ballet tryouts. It is anti police, showing them beating up the strikers for no reason. It is pro union showing that the picket lines are a defense against extreme cruelty and child labor, not an attempt to prevent other non-union workers from working there. It has a million spinoffs in the form of merchandise and promotions for sale that buzz from the 100% good reviews can tap into.

No wonders that aside from Jersey Boys this has to be the most successful show on Broadway of recent years.

Apr

1

What a Personage, from Victor Niederhoffer

April 1, 2011 | 2 Comments

Amazing arrogance in D'Antoni: "I have no problem with Stud and Antony looking for each other as long as they don't overdo it." My goodness, what a personage.

Amazing arrogance in D'Antoni: "I have no problem with Stud and Antony looking for each other as long as they don't overdo it." My goodness, what a personage.

T.K Marks writes:

In a pre-game tv interview D'Antoni did something that the certain star player(s) could very easily take as a gratuitous and not-so-subtle slight. Pointedly claimed that the Knicks' recent bouts of ineffectiveness originate from a lack of "intensity" in the lockerroom, whose custodian of such is presumably part of the job description of one or both of the two guys getting paid $20m/per, and not his own on-court strategies and schemas. That would seem to invite antagonism between himself and certain parties. Found it unduly undiplomatic.

Must say though Uncle Howie is rather perspicacious in these NBA matters. He's been touting the potential of the Nets' nucleus all along. As I had not seen the Nets perform at all yet this season couldn't get over the stellar talent of their big kid, Lopez, and that newly acquired point guard, Deron Williams. That team would appear to be a few players away from being a very formidable outfit.

Mar

31

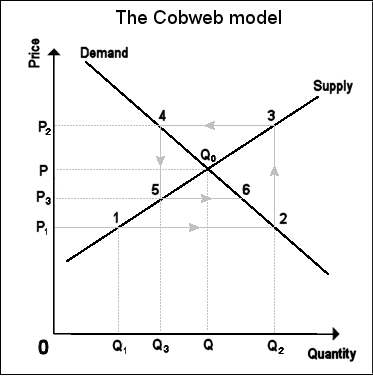

Cobweb Economics, from Victor Niederhoffer

March 31, 2011 | 4 Comments

There's an interesting exercise in cobweb economics setting up in grains.

There's an interesting exercise in cobweb economics setting up in grains.

The idea being that farmers plant for next year based on this year's crop. And when this years price is high, they increase the supply for next year. Thereby lowering the price for the next year. Then they plant less. Prices move in cobweb.

Lorie wrote his PHd thesis on this. Wanted most of all to be a cattle rancher. May corn this year at 6.93 a bushel limit up but December 2012 corn at 5.77.

I took a speculation in honor of Lorie and Watson in the cobweb yesterday and today.

Gary Rogan writes:

Palindrome is taking charge: George Soros making a move to control food and grain production:

Financier and progressive activist George Soros is formulating a move to control food and grain production by purchasing grain elevators in late March in several parts of the United States through his Soros Managment Fund's backed Gavilon Grain . With purchases made in March, Gavilon Grain will become the third largest grain company behind Cargill, and Archer-Daniels Midland.

With strong ties to the Obama administration, Soros now has both the economic, and political clout to begin consolidation of purchasing and shipping domestic agriculture around the world.

U.S. grain firm Gavilon Grain said on Thursday it will buy Union Elevator and Warehouse's 16 grain elevators in the Pacific Northwest , the company's second big purchase of U.S. grain facilities in the last six months.The purchase of 16 elevators at 12 locations in eastern Washington will expand Gavilon's grain capacity by 8.4 mbu.

"The addition of Union Elevator's grain facilities and origination capabilities position us well to support the growing Pacific Northwest export wheat market and serve the Columbian Basin feed grain market," Greg Konsor, VP and GM of Gavilon Grain, said in a statement. The PNW is the No. 1 wheat export terminal in the United States. - Reuters

When food brokers consolidate into just a few large companies controlling the majority of a market, then prices can be set not by supply and demand, but by corporate decisions and manipulation of supply. If the price for food is too low in the United States, then grain can be shipped to other markets for sale, causing then an artifical supply problem in the country that produced the grain itself.With George Soros's making this move in backing Gavilon Grain's purchases to control food and grain distribution in the United States, and becoming the third largest grain company in the country, it will lead to the same results that we see in the energy markets as oil is controlled by a small group of corporations, and the price can be dictated by an artificial control over its supply.

Jeff Watson comments:

Gavilon Grain is just the latest resurrection of Peavey Grain. I expect them to have a big presence in the grain markets as they are true "Grain People." Still, being third place IN THE US behind C@rgill might as well be 50th place. I would not expect the Palindrome to make a dent in C@agill's action, as C@rgill is as politically well connected as anyone. The grain companies were always small in number, and historically were known as the "Big 5." The Big Five were, until the 80's, C@rgill, Continental, Louis Dreyfus, Bunge, and Andre with those companies controlling 75%+ of the world's grain trade and food supply. The big companies still control 75-90% of the grains and food supply, not caring what the prices are as long as they make the deal and don't lose market share. Until recently, most large grain companies were private, family owned corporations. The aforementioned five companies are still private, and huge, but companies like ADM, Ralston Purina, Conti-Commodies, General Mills, Pillsbury, Ralston-Purina, etc are all part of or are public corporations. Despite the small number of grain companies, the profit margins are microscopic, the business is cutthroat, and there is healthy competition between companies, without meaningful quid pro quo's between them. One overlooked aspect of the grain elevators and warehouses is that they are a license to print money if run correctly , which is a reason the big grain companies prefer to remain private, obscure, and below the radar. If C@rgill was a public corporation, it would easily rank in the top ten of the Fortune 500 companies and this is the scale of most of the really big grain companies operations.

Mar

31

A First, from Ken Drees

March 31, 2011 | 1 Comment

I never saw a resigned CEO on fin tv before doing some "splainen"– Sokol. Nice of them to invite him on.

I never saw a resigned CEO on fin tv before doing some "splainen"– Sokol. Nice of them to invite him on.

Victor Niederhoffer writes:

What was his explanation for those who don't have the luxury of a tv? Did it seem to be favorable to the sage by indirection? Or seem to indicate that it's the kind of thing that the sage wouldn't do (any more)?

Ken Drees writes:

It was pro buff– and you would have like the analogy used by the talking heads– buff wouldn't have anyone on his staff that wasn't playing directly in the field of play, a tennis analogy that he doesn't tolerate behavior in the organization that is even close to the line but in play. So the dealings by Sokol in lub stock were technically ok, but really not up to full standards of mount st buffet and really it had nothing to do with him "resigning" anyway.

So why all the chatter about the stock dealings if it didn't matter? Sokol wants to be a mini buff now career wise. Thank goodness he didn't resign to spend more time with his kids. The whole thing is odd.

Mar

30

One played a game of checkers with someone likely to be a front runner for president in a few months, and we discussed the importance of Tom Wiswell's proverb "moves that disturb your position the least disturb your opponent the most". In checkers, I think it means not to break up your foundation, not to have too many infiltrator single men far removed from the bulk of your pieces. Not to have too many holes in your position. Not to have too many of your forces divided by big spaces. Maintain your dike which is a solid row of checkers on a diagonal of at least 4 or better 5 or 6. In general, make sure you have near neighbors for all pieces. I got to thinking how this applies to markets. It seems very applicable. Don't put all your chips at one price. Do things on a scale down or up. Don't move into other markets with big positions when you have the bulk in one position. Keep your positions at approx the same size. Don't throw all your chips in at a certain time, but gradualize into positions. Don't get out at close or in at open. Maintain a constant capital stream. Be humble.

One played a game of checkers with someone likely to be a front runner for president in a few months, and we discussed the importance of Tom Wiswell's proverb "moves that disturb your position the least disturb your opponent the most". In checkers, I think it means not to break up your foundation, not to have too many infiltrator single men far removed from the bulk of your pieces. Not to have too many holes in your position. Not to have too many of your forces divided by big spaces. Maintain your dike which is a solid row of checkers on a diagonal of at least 4 or better 5 or 6. In general, make sure you have near neighbors for all pieces. I got to thinking how this applies to markets. It seems very applicable. Don't put all your chips at one price. Do things on a scale down or up. Don't move into other markets with big positions when you have the bulk in one position. Keep your positions at approx the same size. Don't throw all your chips in at a certain time, but gradualize into positions. Don't get out at close or in at open. Maintain a constant capital stream. Be humble.

What else would you say? How would it apply to life? Don't move into new investments unrelated to what you do without much reflection and gradualization. No staccato in your movements into your second childhood? What else?

Anatoly Veltman writes:

To add: a grandmaster can't use the same sole opening pattern all the time. High level competition will adopt– and they will no longer be disadvantaged. So while it's important to stick with your successful patterns– see if those patterns can be validated for situations arising out of a different opening sequence.

Nigel Davies writes:

I agree with Anatoly. Actually I've often given up opening systems at the height of their success; waiting crocs plus loss of vigilance etc.

Jordan Neuman writes:

There is a similar thought in baseball strategy. In a situation where one's move will lead to countermoves, it is sometimes best to do the opposite of what your opponent wishes you to do given his perception of his own countermove options.

This is all under the general category of putting yourself in someone else's shoes. I find it very easy to see where others have messed up their or their children's lives. I would say my "win percentage" is much higher in those cases, prospectively, than in my own life. Perhaps the Wiswell proverb describes depersonalizing decisions as a way to make them less emotionally difficult.

Henry Gifford comments:

Regarding the above about ruining the lives of one's children, my uncle used to say he ruined the life of his son, who was a heroin addict.

Looking at what he said from the other side, if what my uncle said was completely true, then parents have the power to stop their children from doing drugs or partaking in other ruinous activities, something many parents are frustrated to know is not true.

This perspective can ease the pain in some situations in life, and maybe in trading losses also.

Allen Gillespie writes:

On the violin to play fast one must leave fingers down for the return.

Mar

30

Proverb of the Day, from Victor Niederhoffer

March 30, 2011 | Leave a Comment

One of Tom's favorite proverbs on the "moves that disturb" point was "take care of the draws and the wins will take care of themselves." I like the Greek proverb "little strokes fell great oaks" and of course Sondheim in his hateful way takes that song in Company and makes it "it's the little things you do together… that make marriage a joy," as he shows two couples fighting like cats and dogs.

One of Tom's favorite proverbs on the "moves that disturb" point was "take care of the draws and the wins will take care of themselves." I like the Greek proverb "little strokes fell great oaks" and of course Sondheim in his hateful way takes that song in Company and makes it "it's the little things you do together… that make marriage a joy," as he shows two couples fighting like cats and dogs.

It would be interesting to see if Nigel agrees that "moves that disturb chess positions the least" are best. I believe Art Bisguier told me to try not to break the tension of a position, and I've also been told that once you give away which side of the board you're likely to castle from, the handwriting is on the wall.

Ken Drees comments:

Sultan Khan an Indian native master player from the 1930s used to wait very long to castle and sometimes not at all since castling was not a legal move option in India where he was schooled in chess. It seems like everychanging strategy and recycling (switches) always is necessary to stay competitive, and fresh. Playing against the unorthodox– like the basketball team full court press (Mr. Watson's recent post), or the uncastled king that seems content in the center with a closed position game illustrates the need to be able to counter the strange or unusual opponent. Get a "book" player out of his book and then your fundamentals will hopefully give you an edge. The emotions that occur when faced with the unorthodox style are one more element that the aggressor has in his favor and one more item that the level headed player must tamp down and counter internally.

As for building and constructing ever more powerful latently strong positions–Nimzovich comes to mind as a chess stylist who always made incrementally stronger and stronger tactical moves. This tension naturally releases at some point in the game and then the gameboard takes on fresh vistas of open lines and changed landscapes. Seeing the new and powerful layouts well ahead of your opponent is key to the entire buildup process.

Mar

29

Greenspan and Government Activism, from Paolo Pezzutti

March 29, 2011 | Leave a Comment

We have discussed the role of government in the economy and during crisis many times on this site. Greenspan writes about this topic with the paper "Activism" that I recently read. He writes:

We have discussed the role of government in the economy and during crisis many times on this site. Greenspan writes about this topic with the paper "Activism" that I recently read. He writes:

The current government activism is hampering what should be a broadbased robust economic recovery, driven in significant part by the positive wealth effect of a buoyant U.S. and global stock market.

Equity values, in my experience, have been an underappreciated force driving market economies. Only in recent years has their impact been recognized in terms of 'wealth effects'. This is one form of stimulus that does not require increased debt to fund it. I suspect that equity prices, whether they go up or down from here, will be a major component, along with the degree of activist government, in shaping the U.S. and world economy in the years immediately ahead."

Considerations about the wealth effect are in my view interesting, but well known to those who tried (and managed) to steer a recovery from the crisis.

The wealth effect has supported the economy so far. How much compared to the "stimulus" is hard to say however. "Manipulation" of markets in order to favor a continued move to the upside concerted by strong hands was (and is) in the interest of many forces who have a prominent role.

Victor Niederhoffer writes:

The wealth effect was very big in the 1960s and before, and Latane had good papers on it. Everyone at the Fed has believed in it for 70 years, to the exclusion of looking at interest rates themselves. And Bernanke often times his qualitative announcements with market lows or highs. A good way to trade.

Phil McDonnell writes:

Most of the so called wealth effect is really artificially induced by the QE programs. If the price of your stock rises but the value of the dollars the stock will fetch falls then are you really wealthier? How rich do the folks in Zimbabwe feel?

Jeff Watson writes:

One only has to look at the Weimar to see how the business class in Rhodesia feel. In 1913, the German stock market was at 126. Fourteen years later, the German stock market was at 26,890,000. At the index peak, the value of the Daimler company was only worth 327 of its cars. Interest rates were 900% and the exchange rate went from 4-5 marks per dollar in 1913 to 4+trillion marks per dollar in 1923.

Ian Brakspear writes in:

My portfolio in 1994 was worth aprox ZIM$10 million in 2005 worth ZIM $ 44 billion.

Victor Niederhoffer comments:

What they did to the farmers makes one cry. Brakspear is the guy that posted the funniest spec post ever. He ordered 2 beers for lunch. It was 10 million Zimbabwe. Then by the time he finished lunch, he ordered two more. The price had risen to 15 million Zimbabwe.

Kim Zussman asks:

So does inflation illusion work? What does it feel like to be a billionaire?

Ian Brakspear comments:

I have in my wallet 2 fifty billion dollar notes, a one hundred billion dollar note and one ten trillion dollar note-worthless.

Today the main currency in the streets of Zimbabwe is the US$– how all these US$ notes got here is anyone guess.

They are cleaned regularly in washing machines to prevent the spread of diseases– and hung out to dry on washing lines– always with someone on guard.

Mar

28

"It is common to think of individuals to use genes to make more individual, but from the gene's eye view of evolution, its the other way around. Genes use individuals to make more genes. The chicken is the egg's way of making more eggs". p. 114 The Seventy Great Mysteries of the Natural World edited by Michael Benton.

"It is common to think of individuals to use genes to make more individual, but from the gene's eye view of evolution, its the other way around. Genes use individuals to make more genes. The chicken is the egg's way of making more eggs". p. 114 The Seventy Great Mysteries of the Natural World edited by Michael Benton.

Yes, and its the digits of the prices way of replicating itself to make individual market players create more of those digits. (I wrote about this before here).

The digit 0 plays a big part in the replication game, and it makes individuals sacrifice themselves to create more 0's.

One notes for example that the double digit 00 in 1300 on the sp has been broaches from below on a closing basis from Feb 03 on three times and gone from above to below on three times.

Similarly for the triple digit 000 in 12000 on the DJI. The DAX crossed the triple digit 7000 on Jan 3rd from below, went above below then above then below on Jan 07, then crossed to 7097 on Jan 13 but stayed above 7000 until March 14, then fell to 6436 on March 16, a decline of 10% for the year, and now for the first time on March 25 hit a high of 7006 but failed to close above 6981, a fact which must cause great disennu to the triple 0's in 7000 and they must be inducing much political change in Germany as we speak to achieve that level.

Similar analysis relates to the Nikkei at 10000 which crossed below 10000 on March 11 briefly, but closed at 100075 and then on the following two days declined 20% captures by the triple 000 at 8000 as its low was 7790, a decline of 25% from its mid December levels of 10300.

A similar analysis could be made with the grains especially corn which has shown a similar affinity to 700 as the Dow to 12000 and the SP to 1300.

Instead of taking closing prices for granted we should ask how the digits themselves influence our actions so that we can make them reappear over and over again.

Kim Zussman writes:

A simpler version of this is the opposite of the usual "the market did Y today because of X": We say X because it did Y and we need why.

The evidence is that for many similar X there are many dissimilar Y.

Price is selfish because its impact demands explanation.

Gay Rogan comments:

I'm having trouble understanding any of this. Genes are selfish in the following sense: if genes don't propagate, they disappear, so the only genes that are here today are proven propagators. How can prices or digits permanently disappear? And why would 0's propagate more than other digits? How do these explanations provide more clarity than simply saying people's brains are attracted to numerical markers, and in the absence of other alternatives they chose round numbers?

Steve Ellison comments:

One possible line of reasoning is that people are more likely to put limit orders at round numbers. People often put stops near round numbers, too, but the research I have seen suggests stops are more likely to cluster on the opposite side of a round number from the current price. Here, then, is a hypothesis: if the last two digits of the S&P 500 closing price are above 90 or below 10 (i.e., near a 00 round), the change the next day is likely to be in the opposite direction as today; if the last two digits are above 10 and below 90 (i.e., away from the 00 round), the change the next day is likely to be in the same direction as today.

Checking the last 1584 trading days of the futures,

Near 00 round:

N: 366

reversal next day: 194

unchanged next day: 3

continuation next day: 169

% continuations excl unch: 46.6%

Away from 00 round:

N: 1200

reversal next day: 592

unchanged next day: 15

continuation next day: 593

% continuations excl unch: 50.0%

The percentage of reversals was higher near rounds, but the difference was not significant.

What was significant was the number of closes near the rounds. One would expect a close within 10 points of a round about 20% of the time, but 23% of actual closes were within 10 points of a round, p=0.0006.

Victor Niederhoffer writes:

Here is an interesting paper on round numbers for individual stocks. It doesn't look at expectations, but does look at bid

asked.

Russ Sears writes:

I believe that this paper could be expanded measure this effect on high volume versus low volume stocks. Therefore its stated cost may not be as large as expected on all stocks. My guess, needing testing is the small stocks have this more frequently than the large stocks, that are often computer traded.

Mar

25

Reminds Me of the Boy Wonder, from Victor Niederhoffer

March 25, 2011 | Leave a Comment

The moves in Ford where it breaks through a round number and then opens at the high, and goes straight down reminds me of the incorrigible boy wonder who loved to buy a stock like Anaconda when it wend above 200 for first time, and then to scale into it on a pyramiding basis as it went up.

The moves in Ford where it breaks through a round number and then opens at the high, and goes straight down reminds me of the incorrigible boy wonder who loved to buy a stock like Anaconda when it wend above 200 for first time, and then to scale into it on a pyramiding basis as it went up.

The boy wonder must have enjoyed much pleasure from the follies Bergeres girls on his payroll during those moments before he was led into bankruptcy again with such activity.

Jay Pasch writes:

And what better place to open it than right on the 15.18 gap…

Mar

24

One Raises the Razor Blade, from Victor Niederhoffer

March 24, 2011 | 2 Comments

One raises the razor blade and puts some lather on the face and checks the prices at 7am and notes many markets near local extremes including stocks, fixed income, oil and the beard is still there, as well as the shaving cream.

Mar

24

Briefly Speaking, from Victor Niederhoffer

March 24, 2011 | 2 Comments

I used to love to play an opponent who couldn't win because he was trying to do something that would definitely lose. Like setting his feet leaning towards the left and hitting to right, or hitting me a drop shot when I was always fast enough to return it regardless of where it went. The Knicks are like that. They can't possibly win regardless of what they do, or how good the players are, because their system is bad. The 7 seconds shoot doesn't work. It's not percentage play.

I used to love to play an opponent who couldn't win because he was trying to do something that would definitely lose. Like setting his feet leaning towards the left and hitting to right, or hitting me a drop shot when I was always fast enough to return it regardless of where it went. The Knicks are like that. They can't possibly win regardless of what they do, or how good the players are, because their system is bad. The 7 seconds shoot doesn't work. It's not percentage play.

Fortunately some others seem to realize it now and the coach says "with all the problems I have, I am not going to comment on others problems". Hopefully he realizes it's his problem not the players.

It reminds one of my friend Joe Yuhas, the Christmas tree guy, who tapped out on a silver trade, from the long side below $ 4 and I said, "you shouldn't have been so big" and he said "but I keep thinking what would have happened if I had been short. I could have made as much as I lost" and I said, "but Joe, it didn't matter whichever way you went, you would have lost either way".

Many systems that people use for markets are like that. And those who day trade and give an implicit vig of a few 100% a year, are in similar positions in the main. They play against people whose costs are 1/10 of theirs, capital 1000 times as great, (and they can borrow from a fairy godmother at 0 % also ), and who have much better equipment and speed. And if all those advantages fail, they can force one out at the close, only to move back to where the profit would have been realized at the next open. And yet, the game must continue.

There is hope if D'Antoni trades places with the fake doc as I asked the sullen Patrick Ewing to do who would consign the Knicks to eternal crossings of the river Styx if he were to get back. There is hope for day traders if they go stay overnight.

Jay Pasch writes:

Words of wisdom on the treachery of daytrade margin as the rope seller is glad to offer plenty of product with which to fashion one's own noose…

Kim Zussman comments:

Don't think it's all the broker's fault. Blame EMH. E.g, if all the rational, logical, comfortable, patternistic things are bid every tick, the only things left are irrational, illogical, uncomfortable, and non-patterned. The only people who thrive like that are successful traders and schizophrenics.

Mar

22

Parasites, Edges, and Trading Success, from Craig Mee

March 22, 2011 | Leave a Comment

You think you don't have an edge in the market, well, if you don't have this you may just have one…… Toxoplasmosis:

You think you don't have an edge in the market, well, if you don't have this you may just have one…… Toxoplasmosis:

Around 15 to 20 per cent of Americans are infected with the parasite, according to a study by the U.S. Centres for Disease Control and Infection (CDC).

The study suggests that male carriers have shorter attention spans, a greater likelihood of breaking rules and taking risks, and are more independent, anti-social, suspicious, jealous and morose. The behaviors observed, if caused by the parasite, are likely due to infection and low-grade encephalitis, which is marked by the presence of cysts in the human brain, which may produce or induce production of a neurotransmitter, possibly dopamine, therefore acting similarly to dopamine re-uptake inhibitor type antidepressants and stimulants.

Femi Adebajo:

There we go again so many conditional verbs and clauses… suggests….likelihood….if….likely due to….may produce..or induce the production of…possibly dopamine… a flimsy theory built on a speculative (not in a trading sense) foundation.

Victor Niederhoffer explains:

Okay. The mice make themselves sexy so they be eaten by cats. Then the cats spread the mice around through the sewerage system. The breakout occurs and the trend followers jump in (one can now say this with much greater impunity than the last year), and then the trend followers and pivot boys and breakout boys spread their genes, I mean money, around to the locals and the homeostasis boys when they get out. In former days the locals played a role in the detritovore works.

Anon writes:

[I hate ladies with too many cats.] The scented candle, mystical music, flavored coffee crowd always that has the de rigeur loofah brush hanging somewhere in the shower. It's all part of the Bed, Bath, and Beyond archetype.

Russ Sears replies:

Considering the alternative Bed, Bath and Beyond is to be praised. Besides John Adam's compassionate pining over his alcoholic son, another major difference between David McCullough's book [John Adams ] versus the mini series movie version was his relationship with Ben Franklin. It was not the moral filth of Franklin's mistress that Adams wrote his wife about that he could not stand, it was the literal smell and filth of the pets of this mistress. This filth was hard for Adam's to get past.

Comparing the movie version to the books is a good lesson in the necessary pandering to the liberal stereotyping needed in a movie this days. Let the historical facts be damned.

Mar

22

Always Remember, from Victor Niederhoffer

March 22, 2011 | 1 Comment

One must always remember Slansky's admonition which is that you have to take account of whether you're a winner or loser, and what your average rate of win is relative to the distribution of losses. If you're a good player, never accept a bet with a small edge if it might subject you too close to gambler's ruin, or getting stopped out of you position even if you have an edge. Many a good player doesn't call bets in one's favor if it has too high a variability relative to his bank roll. Many a t-grade should not be taken when the variables like an announcement put the normal tit and tat into jeopardy. I hate to force a weaker player, (assuming I might ever have that luxury again) into making a good shot. Board players are the same way. They can sometimes create a crisis, a tension where if the weaker player makes the rite move, he might pull out a draw or victory. Much better to grind the poor sinner or market into oblivion.

One must always remember Slansky's admonition which is that you have to take account of whether you're a winner or loser, and what your average rate of win is relative to the distribution of losses. If you're a good player, never accept a bet with a small edge if it might subject you too close to gambler's ruin, or getting stopped out of you position even if you have an edge. Many a good player doesn't call bets in one's favor if it has too high a variability relative to his bank roll. Many a t-grade should not be taken when the variables like an announcement put the normal tit and tat into jeopardy. I hate to force a weaker player, (assuming I might ever have that luxury again) into making a good shot. Board players are the same way. They can sometimes create a crisis, a tension where if the weaker player makes the rite move, he might pull out a draw or victory. Much better to grind the poor sinner or market into oblivion.

Anatoly Veltman comments:

This is very right about chess and checkers. Grandmasters often lose sight of this good advice: forcing a weaker opponent into a series of the only possible moves on his part - will not necessarily lead to your definite win; but it will certainly prevent your opponent from making a poor move of his own!

Mar

22

Lesson for a Day About How to Lose from the Knicks, from Victor Niederhoffer

March 22, 2011 | 2 Comments

The Knicks inevitable loss to Boston even though they were leading by double digits in the fourth quarter, and their being ground into certain oblivion by a team with a better system has many lessons. Sometimes when you're playing a sport and the other guy gets ahead of you but does it with much non-percentage play or luck, one believes that one will be able to win by just playing more fundamental play and running a little harder and defending a little harder and one isn't too worried about the opponent being ahead. Especially if you know that on an average play you're better than the opponent, and the opponent can only make a point by luck. Such is the situation whenever a team plays the Knicks. They know that they can surmount any reasonable deficit in the fourth quarter as Boston knew.

The Knicks inevitable loss to Boston even though they were leading by double digits in the fourth quarter, and their being ground into certain oblivion by a team with a better system has many lessons. Sometimes when you're playing a sport and the other guy gets ahead of you but does it with much non-percentage play or luck, one believes that one will be able to win by just playing more fundamental play and running a little harder and defending a little harder and one isn't too worried about the opponent being ahead. Especially if you know that on an average play you're better than the opponent, and the opponent can only make a point by luck. Such is the situation whenever a team plays the Knicks. They know that they can surmount any reasonable deficit in the fourth quarter as Boston knew.

Same thing in a market that hovers a little below unchanged near end of day when it's ready to move to lead.

p.s. the talk from the estimable Carmelo, like a robot: "we got to play the system. We have to play the system. Everyone in league knows that D'Antoni system if great for offense and that we have to stick with it. Just take your shots within it" reminds one of the song from Damn Yankees: "you got to play the game". You got to play the game. Of course, Melo is being loyal which is good. But even he couldn't believe that they should play with that terrible system so demoralizing to all the players who have to work to get in position only to see a freak luck shot by a Toney Davis or the celebratedly departed still Gallo for a three tossed up to the basket. One is reminded of Grandpa Martins' letter to Coach Ryan: "when you have an All American like Artie in the game who has made every catch and every tackle… why give the ball to anyone else. no hard feelins either way."

Mar

22

The Accrual Anomaly, from Victor Niederhoffer

March 22, 2011 | Leave a Comment

One wonders whether such past anomalies found as the "the accrual anomaly" based on large accruals in non-cash assets, like inventory and receiveables, which are manipulatable, that flow into earnings are overstating the persistent ability to profit, such as this, are still profitable. A quote in Malkiel–, "I have never seen a back test that I didn't love, but devil take the hindmost when you try to use it" comes to mind, but such studies that look at the balance sheets seem less likely to have been exploited.

Paul Hendry comments:

The basic thrust of the paper is that individual equity investors with limited attention are fixated on accounting profitability while neglecting cashflow profitability. The primary cause of mispricing is the net operating assets anomaly or "balance sheet bloat".

Reading over this 50 page study which is highly technical but has a few interesting points:

-They do not believe that mutual funds who identify the mispricing take out all the arbitrage opportunity.

-Most equities with high accruals on the books are typically small size, low price, low liquidity but high systematic risk. Traits not appealing to funds.

-High institutional ownership reduces accrual mispricing.

-Growth orientated mutual funds outperform benchmarks.

-Funds that concentrate of fewer industries perform better after adjusting for risks and styles.

-In general, mutual funds underperform the market by 0.6% to 1%. Transactions costs are significant.

If you accepted their findings then a mutual fund investor should go into an aggressive growth fund, that goes both long and short, low transaction costs, specializing in one or few industries. To capture the mispricing would take consistent analysis that a fund has the resources to do..

Mar

22

A Book Review I did for Barrons, from Victor Niederhoffer

March 22, 2011 | 2 Comments

History Lessons for Investors

History Lessons for Investors

A Thrice-Told Tale, All in One Book

Reminiscences of a Stock Operator, Annotated Edition

by Edwin Lefevre and

Jon D. Markman,

With a Foreword

By Paul Tudor Jones

Wiley

423 pages

$34.95

Reviewed by Victor Niederhoffer

Imagine that master novelist and chess aficionado Vladimir Nabokov wrote a fictional memoir by Capablanca—the 1920s world champion who never made a mistake on the board—and that Bobby Fisher then published an updated and annotated version, incorporating all of the important developments of modern chess strategy, along with a foreword by Anatoly Karpov. A similar multilayered feast on investment is now available, with minor differences. Edwin Lefevre's Reminiscences of a Stock Market Operator is a novel told in the first person by a character inspired by legendary trader Jesse Livermore. This classic is now graced with extensive annotations by investment advisor Jon Markman, and includes a foreword by hedge-fund manager Paul Tudor Jones.

The result is big and beautiful, cutting across two centuries of booms and busts and market and economic history, with a myriad of vintage historical photos and instructive historical charts throughout.

One of Lefevre's favorite adages is that there's nothing new on Wall Street. The similarity between the financial panic of 2008 and the 1907 panic recounted in the book is a prime example.

The numerous squeezes, manipulations, insider trading, government hauling in of scapegoats and frauds settled for pennies on the dollar that Lefevre and Markman recount are horses that are found as well in the modern stable.

The book can be divided into three parts: 1. The bucket-shop era from 1890-1910, when Livermore was able to make easy money by taking advantage of the bid-asked spread on inactive stocks with leverage of 100 to one. 2. His days as a stock trader on the New York Stock Exchange from 1910-1920, when he went bust over and over again, despite his abilities and insights, because he used too much leverage. 3. His career as a stock manipulator in the 1920s, where the fees he charged were 25% of the market value of the manipulated stock.

But there is a fourth part of the story, which happened after Lefevre wrote Reminiscences of a Stock Operator. Markman fills in the details. Livermore went bankrupt for at least the fourth time in 1934. His excess liabilities of $2 million included promised payments to the dancer Lucille Ballantine for keeping him "cheered and amused," and a liability for breach of promise to a former secretary.

Despite having amassed a fortune of $100 million by 1929, Livermore was back where he started at 16. He did not seem to learn from his mistakes. The excessive spending that put him in the hole over and over again was part of a much bigger mistake that he repeated throughout his career. He traded with so much leverage and generated so many commissions and gave away so much slippage in his bid-asked spreads that even a small move against him, one almost certain to occur in a season, would be enough to create ruin and worse. After losing his fortune or going bust at least six times, Livermore committed suicide in 1940 at the age of 63 at the Sherry Netherland Hotel in Manhattan.

The original book is replete with sensible suggestions for making money. The problem is that many are untested and contradictory. It took a man of sagacity and respect—a trader and shrewd, prize-winning journalist like Jon Markman, to separate the wheat from the chaff.

The appendix contains 100 main tenets of the Livermore method, which are just as profitable for today's traders as they were for Livermore–provided they are tested and used without improper leverage and transactions costs.

This book will live forever.

Mar

21

Briefly Speaking, from Victor Niederhoffer

March 21, 2011 | Leave a Comment

1. The return of Gallo to the Denver Lineup, and his previous absence must be the reason that they were winning before and can be expected to lose now. Such a new beginning should be used in markets to determine the distributions after a new event like the first up opening in x days or the first red or green in the colored co-movement chart that Doc updates on daily spec.

1. The return of Gallo to the Denver Lineup, and his previous absence must be the reason that they were winning before and can be expected to lose now. Such a new beginning should be used in markets to determine the distributions after a new event like the first up opening in x days or the first red or green in the colored co-movement chart that Doc updates on daily spec.

2. I have always eschewed the development of systematic methods based on anomalies for making an extra buck in individual stocks for a different reason than Richard Roll who finds that they never do half as well in real life as they do on paper. My reason is that by the time you consider the extra 2 or 3 percentage points you can make from them at the best, your customers if you have any couldn't cover the cost of their fees and be left with anything good. And if you don't have customers like me, then the return you could possibly make from them would never be sufficient to cover your expenses.

3. Louis L' Amour in The Iron Marshall has written a great Horatio Alger story that has almost as much accurate stuff about New York City in the 1850s in it and great Titanic Thompson con man stuff in it, as does his usual Western fare, always written with a topographical map at his side. However, I repeat that his constant emphasis on boxing technique as the deciding factor in who gets ahead and his inability to flesh out the endearing personal nobility of relations between friends the way O' Brian or Schaeffer can makes much of his work very shallow.

4. The overreactions in the market last week show how waiting without trading for the time when you normally would have been squeezed out, but then going in big is a viable strategy. The main problem with this is what would have happened to you if you did this the day in October 2008 the market anticipated the inevitability of the community organizer's election and dropped 20% in two days.

5. It is always amazing to me to read the GaveKal analysis of the influence of world events on stock prices. They invariably come to the same conclusions as me, almost always in favor of the long term drift, and almost always taking a contrarian approach to investing. They have a good essay on why they are bullish on Japan now. Based on such things as that their market is underweighted and undervalued relative to other markets, and their own history, it is likely that easing will occur, and that the nuclear crisis was much more contained than fearful reports made it out to be. I have never seen a GaveKal analysis that I didn't agree with except for one of their favorite hobby horses about how the inexorable and unbeatable new type of virtual company arising a la Carefour that can make an infinite rate of return et al.

T.K Marks comments:

The fade Gallo system of basketball handicapping reminds me somewhat of a client that we used to have when I first started out on the floor. There was this direct line phone to a brokerage concern that would ring all day long with order entries. Nothing particularly noteworthy of having with having a busy client, but it was the type of orders that piqued my novice interest.

You see, every order that was entered was a cross: Buy and sell equal amounts at the same price, whether above or below the market, or at the market. As I obviously found the net result of all these transactions to be unduly homeostatic in terms of P&L, after about a week of observing this curious phenomenon I finally mustered up the temerity to ask a grizzled sort twice my age what was the purpose of this.

He just looked at me blankly for a moment before succinctly advising, "Don't worry about it."

So about two weeks later, and after I had passed his vetting process I guess, he out-of-the-blue explained what all those crosses from particular brokerage house's crosses were about.

Their experience being that the equity of most retail accounts having short half-lives, their thinking was to take the other side of every one of their customers' orders.

It was my first exposure to any sort of trading system. And although it was as regimented and rigidly fixed as could be, those characteristics had nothing to do with mathematical calculations and everything to do with human nature.

As far as they were concerned, when it came to silver futures traded in a retail account, everybody was Gallo until proven otherwise. In the long-run I'm not sure what the karma consequences of presuming that everybody is a hoodoo waiting to happen, but the people from that brokerage house were obviously no strangers to some of the darker corners of psychology.

Mar

21

A Gilbertian Googlewhack, from Victor Niederhoffer

March 21, 2011 | Leave a Comment

One is reminded of scenes from Iolanthe "proudly let the drums roll/ we are peers of highest station/ pillars of the English nation/ ta ran ta ran ta ra" from memory as the markets after two fantastic drum rolls of upness at the opening repeat it for the third time in a row as of 11 pm, thereby creating a Gilbertian googlewhack.

Mar

21

The Boy Wonder, from Victor Niederhoffer

March 21, 2011 | 5 Comments

One should never use the habits of the Boy Wonder as a source for emulation except in the field of romance and good times before the inevitable last days. Certainly everything he did in speculation was wrong except for his ability to cheat the bucket shops by betting on reversals arising from the concentration of limits at the bid and the asked.

One should never use the habits of the Boy Wonder as a source for emulation except in the field of romance and good times before the inevitable last days. Certainly everything he did in speculation was wrong except for his ability to cheat the bucket shops by betting on reversals arising from the concentration of limits at the bid and the asked.

Ken Drees comments:

I don't know if you are judging him too harshly or not, but I read somewhere that he suffered from clinical depression and at that time was not a known ailment– maybe this led to his "trade–all the time" mentality and other outlets for passions. Beating the bucket shops who cheated the public at their own game seems counting card like to me– which led those cheats to get a bigger and bigger shoe– to keep the metaphor extended.

And maybe I am too harsh on the schooling aspect– but less chit chat, what do you think about the market talk is better for me as I try to extract longer term trend trades and stay with them. As an example, the Middle East shakeup in my mind means one thing, trade wise, and that's higher oil price. I try to minimize the back and forth headlines as much as possible. In that vein, Livermore's isolated trading office was set up to keep outside influence away. I think there is something good to take from that.

Victor Niederhoffer replies:

One would think that he suffered more from excessive inebriation and the aftermath of womanizing too much than clinical depression. The depression was likely caused by his extravagant and unsustainable life style and vig paying.

Mar

21

A Rather Shocking Study, from Victor Niederhoffer

March 21, 2011 | 1 Comment

A rather shocking study which shows that investors in mutual funds receive a much worse return than the actual return shown by the mutual fund through putting most of their investment in before the mutual fund goes down and least of their investments when mutual funds before the mutual fund goes up. The actual underperformance seems to be of the order of 3 percentage points of return a year, i.e, 6% versus 9%, with sector funds and specialty funds and growth funds showing much greater underperfomance. This must be a pretty good indicator of when to go against a particular sector.

A rather shocking study which shows that investors in mutual funds receive a much worse return than the actual return shown by the mutual fund through putting most of their investment in before the mutual fund goes down and least of their investments when mutual funds before the mutual fund goes up. The actual underperformance seems to be of the order of 3 percentage points of return a year, i.e, 6% versus 9%, with sector funds and specialty funds and growth funds showing much greater underperfomance. This must be a pretty good indicator of when to go against a particular sector.

Steve Ellison writes:

I read Mr. Swedroe's book Rational Investing in Irrational Times. This is very interesting data, but it undermines his main message, that the market is efficient and even professional managers can't beat it, so you should diversify and keep costs low by buying index funds. If mutual funds favored by the public underperform by a wide margin, something else must be overperforming. One might be able to beat the market by simply avoiding the hot funds and their favored stocks, like Bacon's technique of betting on all the other horses besides the overpriced favorite.

Mick St. Amour writes:

A great contrarian indicator. The retail investor is often guilty of chasing returns and as you can see this is a performance killer.

Larry Williams writes:

Aha, mutual funds are for the masses, while the elite managers of money: Cohen, PTJ, Dalio– are the winners for their clients.

But hold on a moment here. Lots of professional managers have beat the market for many, many years. It can be done, and it is being done. But not all can do it. Just like not all teams will be in the final four, and while luck is part of the game, in the end skill carries the day.

Mar

20

Query of the Day, from Victor Niederhoffer

March 20, 2011 | Leave a Comment

What would the return on buying one share of every internet related company have been for various beginning and end periods? One is not sure it was a bust, especially taking account of the returns of venture capital companies that invested during that period. One Ebay or Facebook or Groupon could cover many a 0% return.

Mar

18

Amazing Moves, from Victor Niederhoffer

March 18, 2011 | Leave a Comment

The amazing moves this week are consistent with my 50 year old studies as to what happens following cardinal panics like airline crashes, and presidential assassinations. A terrible move down, and then by the end of the week, right where it was before. It happened to i s p and the grains and oil and the dollar yen. What else? How to generalize?

The amazing moves this week are consistent with my 50 year old studies as to what happens following cardinal panics like airline crashes, and presidential assassinations. A terrible move down, and then by the end of the week, right where it was before. It happened to i s p and the grains and oil and the dollar yen. What else? How to generalize?

Jon Longtin responds:

"…how to generalize?"

One thought would be to do a simple curve fit on an instrument of your choice after each event in history. Since the events themselves are unique and relatively short in duration (earthquake, assassination, terrorist bombing, etc.) and also very well defined in time, the trigger point (or time t=0) is well known almost immediately after the event happens.

In general a cusp-like response is observed (very rapid decline, followed by a well-defined apex, and then a rapid ascent (although probably not as sharp as the descent) to some threshold pre-event point (say 80%).

The underlying argument would be that people's mass reaction to any catastrophic event is similar (panic, confusion, and uncertainty followed by the gradual realization that the world is not ending, and things work back to normal). Since the underlying behavior is the same, it's not unreasonable to expect that the financial instrument's response should similarly be the same across different events. One could then try to form a single curve by appropriate scaling (so-called self-similar behavior). Then, when a new situation presents itself (hate to sound so detached when speaking of disasters), one could chart the instrument's history against the curve, and as soon as enough points were collected, match/scale it to the master curve and make an estimate as to the turn-around point and recovery and go from there.

One could further classify events into separate categories, e.g., natural disasters, political events, financial events, etc., and prepare appropriate curves for each, since the nature of the event will be similarly well defined and knowable very soon after it happens.

The engineering analog is somewhat along the following lines: a standard technique to test a system is to apply an impulse response and see how the system responds. Examples include tapping an automobile frame with a hammer and measuring how the structure responses in time, or using a gunshot to measure the acoustics in a large hall. In these measurements, the initial driver (the hammer hit or gunshot) happens so quickly that it has come and gone before the system has had a chance to even begin to respond. As a consequence the resulting measurement is only the response of the system and is not contaminated by the initial response.

In contrast, drivers that that are longer in time have a more complicated interaction with the structure, because the structure will start to respond to the first part of the driver, but the system is still being driven. The analog would be grabbing onto the car frame with your hands and shaking it repeatedly for a few minutes to get it to vibrate: the car frame will begin to response as soon as you start shaking it, but then as you continue to shake it, that further alters the response, which affects the response, etc. etc. = much more complicated to analyze and predict.

In financial terms, disasters are often very short in duration (seconds and minutes), and subsequently they behave like an impulse response, with the system being society. In contrast, an event such as the wave of unrest in the middle east is a much longer time-frame event (weeks and months): the event and the response become highly coupled, making their analysis more complicated.

Anatoly Veltman writes:

Not sure if it's a separate topic, but there are sometimes dangers when you generalize. For example, the level of EUR currency (and its perceived trend) is significantly higher today than at this sample's outset. To what degree did this influence most commodities' comeback?

Another layer that could be added to this sample's analysis: what to make of the relatively lagging instruments? Sugar, Platinum and Palladium haven't made up their losses…

The President of the Old Speculator's Club, John Tierney, responds:

How does one make generalizations from the recent events outlined by the Chair? I have no doubt that his 50-year study shows similar market reactions. However, I'm reluctant to adopt any new theories or adjust my current investment outlook due to these studies. The current environment, and one that has existed at least since the Fed initiated QE1, is the involvement of government agencies.

I and others have suggested this surreptitious presence in the past. We have been (rightly) put in our place because we failed to fulfill the Chair's mandate: "stats on the table" (something, by the way, which Rocky was very, very good at).

In the current situation and that which has existed for several years now, we KNOW that our government (and others) have been manipulating the "invisible hand." We may not be aware of the extent of the presence, or where it is being applied, but that it exists is an established (and self-confessed) fact.

With that in mind, I'm left to "guess" whether the current scenario is an accurate re-enactment of past events, or whether it has been manipulated to seem so. For years we on the List have been leery of the efficacy of any government interference in the markets. With that in mind, it's difficult to make a legitimate extrapolation from past events - the new, big, player makes any surmise questionable.

My reluctance to revise my pre-existing view of the market's course is only enhanced by the numerous television experts who are outlining a "bounce-back" scenario based on past bounce-backs. It may well occur but will it endure or will it vanish with the exit of the interference? I'm currently betting (and that IS the right word) against it.

William Weaver shares:

Check out this interesting abstract:

Behavioral economic studies reveal that negative sentiment driven by bad mood and anxiety affects investment decisions and may hence affect asset pricing. In this study we examine the effect of aviation disasters on stock prices. We find evidence of a significant negative event effect with a market average loss of more than $60 billion per aviation disaster, whereas the estimated actual loss is no more than $1 billion. In two days a price reversal occurs. We find the effect to be greater in small and riskier stocks and in firms belonging to less stable industries. This event effect is also accompanied by an increase in the perceived risk: implied volatility increases after aviation disasters without an increase in actual volatility.

Found via the Empirical Finance blog

Mar

18

GoogleWhacks, from Victor Niederhoffer

March 18, 2011 | 1 Comment

There is something called a googlewhack, something where two words have never been used in conjunction on the same page. There should be a similar thing for markets "a whackpatt?" when a event that's only happened once before in last 15 years occurs. There should be a restriction to only two or at most 3 independent variables or some similar rule of simplicity. Today is a good whack. Was up 10 yesterday, and now same 10 with a few finesses.

There is something called a googlewhack, something where two words have never been used in conjunction on the same page. There should be a similar thing for markets "a whackpatt?" when a event that's only happened once before in last 15 years occurs. There should be a restriction to only two or at most 3 independent variables or some similar rule of simplicity. Today is a good whack. Was up 10 yesterday, and now same 10 with a few finesses.

Mar

17

Flexionism of the Day, from Victor Niederhoffer

March 17, 2011 | 1 Comment

So is the consensus now among us non flexions that the radiation danger is merely exaggerated 100 fold so that technology in the US will be set back 30 years, and government intervention will be lubricated for the next 4 years to deal with the crisis which seems so much worse to the US than the Japanese and IAEA? This is not meant to diminish the magnitude of the tragedy in Japan, but merely to wonder if we believe that the subsequent dangers have been much exaggerated for flexionic profit?

So is the consensus now among us non flexions that the radiation danger is merely exaggerated 100 fold so that technology in the US will be set back 30 years, and government intervention will be lubricated for the next 4 years to deal with the crisis which seems so much worse to the US than the Japanese and IAEA? This is not meant to diminish the magnitude of the tragedy in Japan, but merely to wonder if we believe that the subsequent dangers have been much exaggerated for flexionic profit?

Anatoly Veltman writes:

Yes, of course. One thing to be sure about is that T.Boone Pickens' funds will start getting ahead, as Natural Gas projects (like gradual highway infrastructure to facilitate filling-up vehicles, especially trucks and such) should finally be given light-of-day.

Bill Rafter comments:

"Never let a crisis go to waste."

Jay Pasch writes:

Buy the clashing of bearish cymbals, and sell the euphoric opposite…

Kim Zussman ironizes:

Buy the clashing of bearish cymbals, and sell the euphoric opposite in flat/choppy markets. If markets ain't flat or choppy, don't buy and sell 'em.

Steve Ellison writes:

No doubt it was my poor judgment, but from the perspective of operating a specialty line in panics, the moments of panic in the past week in the S&P 500 seemed too brief and ephemeral to go all in. The changes since the earthquake were:

3/11 +11.7

3/14 -10.7

3/15 -15.2

3/16 -21.4

3/17 +14.9

There were three moderately large down days in a row, but for perspective, the S&P 500 futures are still up 1.5% year to date. Only for the briefest of moments did they trade below the 1247.9 year-end close of 2010.

Mar

16

More Natural Disasters Likely? from Victor Niederhoffer

March 16, 2011 | Leave a Comment

What is the geophysics of thinking that more natural disasters are more likely now that the earth quake has occurred?

What is the geophysics of thinking that more natural disasters are more likely now that the earth quake has occurred?

Kim Zussman shares:

Read this article.

Rudolf Hauser writes:

Another factor to consider is the shifting of the magnetic poles. This is reportedly associated with violent swings in weather and more earthquakes and volcanic explosions. Apparently there has been a marked acceleration in the rate of shifting in the past few years. Some question whether this might be the cause of recent weather extremes and geological activity. Since such shifts occur only every half million years or so we obviously have little idea of how they progress. If this is a real reason for concern it is an issue far more immediate and important that the global warming fears.

Pitt T. Maner III writes:

There have been suggestions of a connection with renewed (regional?) vulcanism.

The last eruption of Mt. Fuji , for instance, occurred 49 days after the previous largest earthquake in Japanese history.

Another Japanese volcano has resumed activity but cause/effect from the March 11 quake may be tenuous.

The volcano, Shinmoedake, is famous for standing in as the villain's secret rocket base in the 1967 James Bond film, "You Only Live Twice".

Bill Rafter comments:

Earthquakes and volcanism are simply different manifestations of the goings on of plate tectonics.

Read this article from New Sceintist: "The megaquake connection: Are huge earthquakes linked?".

Mar

16

Market Gyrations Caused Me to Miss Knicks Game, from Victor Niederhoffer

March 16, 2011 | Leave a Comment

The market was gyrating so much last night in a negative direction that I didn't even have time to see how badly the Knicks got killed while I was out. And the regression bias has never had a better examplar than the Knicks. Luck + skill determines every outcome. The luck is random. Whenever the Knicks have a good win, the luck factor was highly favorable. And then the next time out they lose by 47.

The market was gyrating so much last night in a negative direction that I didn't even have time to see how badly the Knicks got killed while I was out. And the regression bias has never had a better examplar than the Knicks. Luck + skill determines every outcome. The luck is random. Whenever the Knicks have a good win, the luck factor was highly favorable. And then the next time out they lose by 47.

J.T Holley writes:

It's very much the same as my beloved Va Tech Hokies in all their sporting events. The listing of the samples for the regression bias can be used with football and basketball which makes it all the more interesting when I gather data.

The ultimate highlight that sticks out in the sampling of being a fan is 11-0 regular Season with Andre Davis on the cover of Sports Illustrated with the caption "Do They Belong?", meaning to me that luck got them there. Lost in the NCAA Championship to Fla. State in a 46-29 nail biting game that is still talked about as one of the greatest losses, great loss yeah right? That loss was 1/4/00, the S&P 500 top ticked within days of the loss.most recently to add was the NCAA committee somehow having watched the Hokies fight and claw with 7 players to beat Duke at home while ranked #3 only to follow up to losses to Boston College and Clemson in final two regular season games. Be casted in typical fashion as a bubble team. Go into the ACC Tourney win, then beat Fla. State on a tenth of a second made shot that was canceled after regulation. They must've said luck, thus snubbed from the NCAA Tourney for the 4th straight time after a couple years back being the only 10 game ACC winner not make the Tourney. S&P 500 is at hand in gyration.

It's sad and the life of a Hokie, but the regression bias to the S&P is there as well.

I have often wondered now as a grown man looking back at this game against Florida State (yes the Seminoles again) and the luck + skill that it required didn't curse or hoodoo Virginia Tech in some way?

I dare not even pull data from 1980 to see what the S&P did days after. It's like I know it somehow wouldn't even effect the averages in the regression bias if it was positive anyways.

Alston Mabry writes:

The Hokies got stiffed again. This year, though, I think they may be standing in the "stiffed" line behind Colorado. Not only did Colorado (overall 21-13, 8-8 conf) go 6-3 in their last 9 games, including a win over now-4-seed Texas, but in that stretch they won their first round game in the Big 12 tourney against Iowa State, then in the next round beat Kansas State for the third time this season, and finally went up against Kansas, a team that along with Ohio State forms the most common prediction for the NCAA final game…and Colorado scores 83 points against Kansas in a tough loss. But Colorado doesn't deserve any place at all in the NCAAs? They can score NBA-level points in a tournament game against one of the consensus two best teams in the country…but they don't deserve a slot in the NCAA tournament. If that makes sense, explain to me why Villanova isn't headed for the NIT.

Once one examines these situations at Va Tech and Colorado, as well as other seeding and bubble-team choices, one can't help but think that perhaps the committee is screwing this whole thing up on purpose so they can say, "You're right! We messed up! The only solution is to expand to 96 teams!"

J.T Holley replies:

Very simple. The NCAA Committee is made up of only TWO people that have played basketball or coached basketball.

The answer to Villanova is that they are in the Big East. The Big East gets a bias and free pass. They have the most Teams in 11 being selected for the Tournament. No other Conference constantly gets more at large bids, yes I'm aware they have the biggest conference with 16 Teams. There are what 37 at large bids. 11/37= a tad bit biased under 30%.

My conspiracy theory is the following: The Big East is such a lackluster Football Conference in the past decade that the NCAA overcompensates for them in basketball due to their humiliating play on the gridiron and the fact that the BCS favors the SEC.

Note that Alabama an SEC team was 12-4 and won their side of the conference in basketball in the SEC and got snubbed as well by the NCAA Committee?

Worth noting is the eventual winners and why the bias now? Who was the last Big East Team to win the NCAA Tourney? '04 UConn then prior it was '03 Syracuse. That is over 7 years ago? In the meantime either the ACC or SEC has won 5 of the last 6 Titles?