Nov

14

Inquiring Minds Wish to Know, from Victor Niederhoffer

November 14, 2010 | Leave a Comment

Tremendous run of red and green colors in the bond stock interrelations foretelling a return to days when increased output was considered good for both bonds and stocks, and decreased output was considered bad for both bonds and stocks. What does this foretell for the future? Is it bullish or bearish for both? And why did it happen? Inquiring and hopeful of profit minds wish to know.

Nov

13

Childrens Money Book Recommendations, from Ken Drees

November 13, 2010 | 2 Comments

Do you all have any suggestions for childrens money books? Any ideas for a ten year old? I read The Richest Man in Babylon when I was 22– if that gives you any idea on the lack of money/market books in my young life.

Do you all have any suggestions for childrens money books? Any ideas for a ten year old? I read The Richest Man in Babylon when I was 22– if that gives you any idea on the lack of money/market books in my young life.

Alan Millhone writes:

The money books I had when ten were by Whitnam, and there were slots for collecting dates of Lincoln pennies and buffalo nickels and mercury dimes etc.

Dylan Distasio responds:

Hi Alan,

Thanks for bringing back some wonderful childhood memories for me. My father passed on coin collecting as a hobby to my brothers and myself when we were children. I haven't been very active with it as an adult, but I used to love sorting through change bags from the bank in search of silver coinage or old pennies to fill my Whitman coin folders. I grew up in the 80s when you still had a chance to come across some silver ones (granted they were not in very good condition). I also have some old Morgan heads and other assorted issues. One of my favorite coins as a child was the "steel" penny from 1943.

More recently, I've collected proof sets of the state quarters series, although not for hopes of financial gains, I just love the look of a proof struck coin and find the state quarters interesting.

Nov

13

CLIENT 9: The Rise and Fall of Eliot Spitzer, reviewed by Marion Dreyfus

November 13, 2010 | Leave a Comment

With Client 9, director Alex Gibney explores the shadowy corners of a seemingly familiar story.

With Client 9, director Alex Gibney explores the shadowy corners of a seemingly familiar story.

There is a striking shot of a snow leopard toward the end of this remarkable documentary. The leopard, taken in the middle of a snowy scene midwinter in NYC or some vast landed zoo, stalks the forest or tree line. He is elegant, feral, dangerous … yet beautiful. There is a clear parallel in the Spitzer shown in this rare documentary that gives viewers close-up and personal access to so many pooh-bahs and mastodons of the financial world. Client 9 tells the story of a sensational trial with unprecedented access to prosecutors, defense attorneys, Market panjandrums, Fed types, usually inaccessible moguls, victims and, from behind bars, Mr. Spitzer, himself.

Some viewers were annoyed at having to sit through this well-photographed, well-paced, well-written doc, because they knew it to be Step One in the rehabilitation of the Man That Was Eliot Spitzer.

Since the film wrapped, he has inaugurated a (now failing) talk show on CNN, and he will be speaking around town in the near future (18 November, Fordham, for one).

The fascinating aspect of this 'kiss'-and-tell are the female distaffers of his escort service who speak on camera—some using surrogate actresses to mouth their speeches!—as Spitzer seems for all the world like a thinner, smarter, faster-talking Al Gore sitting at his ease, discussing the vagaries of Lehman or BoA mishandlings, arrests and such. Nerveless and shameless. There is only one point in the entire length of the piece where Spitzer's eyes dart to the side in a well-understood feint of embarrassment and guilt. But it lasts an eye-blink.

I see this as of a piece, in a sense, with THE SOCIAL CONTRACT, about the formation of FaceBook, and WALL STREET 2: MONEY NEVER SLEEPS. They form a triumvirate of fast-thinking, chicanery-ridden, entrepreneurial and high-energy brain friction that motivates and energizes so much of the picture we 'admire' so often about the canyons of Wall Street.

One looks at the title and wonders if it is prologue or prophecy. This was a man who had inexhaustible jet propulsion, almost. It remains to be seen if he can propel himself back into the graces of society again.

One kind of hopes he will, because he has the appeal of a cunningly patterned and talented snake. Always interesting to see how and where such mesmerizing creatures go, no?

Nov

12

The Stock Market as a Beauty Contest, from Kim Zussman

November 12, 2010 | Leave a Comment

"The stock market is the type of beauty contest [apparently common in England at the time] in which you choose the girl that most others will find most beautiful, not the girl you find most beautiful." –Keynes

"The stock market is the type of beauty contest [apparently common in England at the time] in which you choose the girl that most others will find most beautiful, not the girl you find most beautiful." –Keynes

Not sure about Maynard's proclivities, but those afflicted with affinity for the opposite sex may find such judgements most difficult.

Rudolf Hauser writes:

This points to a key difference between long-term investing using fundamental analysis and trading. In essence the trader/speculator skill's lies in seeing how others will view events and makes his bets accordingly. This is the case even if someone with an intermediate term horizon relies on fundamentals in their analysis. In contrast the long-term investor (horizon measured in next few years) implicitly trusts not in his or her ability to anticipate how others will react but assumes superior knowledge in anticipating the future fundamentals of a company will enfold and considers if the security is likely to provide a superior return over that longer horizon given how the market usually perceives such a future state on the assumption that the usual influences on a stock short-term will at some point reflect the future values perceived by such an investor. To the extent that the market is driven by the former, opportunities can occur. For example, in a market downturn long-term opportunities may arise but the market could continue falling because of a near-term focus of most market participants. Accumulating a position over time would allow one to avoid buying the possibility of buying at even better future prices while avoiding the possibility of not taking advantage of current prices entirely should the market have reached bottom. Naturally a long-term investor has to be prepared to hold (avoid leveraging) his or her position and for periods of low or negative returns. Naturally that same fundamental investor will improve his or her performance to the extent that he or she can predict how traders will react and impact near to intermediate term price movements to time their own transactions.

Nov

12

Cisco and the Government, from Paolo Pezzutti

November 12, 2010 | Leave a Comment

"Disappointing sales and profit forecasts from Cisco Systems Inc. show cutbacks in government spending that pose risks for companies that rely on the sector for growth." "State government orders fell 48 percent in the last quarter"

"Disappointing sales and profit forecasts from Cisco Systems Inc. show cutbacks in government spending that pose risks for companies that rely on the sector for growth." "State government orders fell 48 percent in the last quarter"

It is interesting to see how the times of the dot.com bubble are behind us. Now that the precipitous pace of growth is over they have to rely on increasingly indebted governments to keep their business going…Who is John Galt?

Gary Rogan writes:

If you superimpose the growth in the US GDP vs. growth in public debt since a little after 2000 you will realize that the entire US economy has been relying on the increasingly indebted government to keep the GDP growing, and that process went into hyperdrive since 2008. The entire growth for the last decade has been just a glorified game of check kiting.

Rocky Humbert responds:

GDP 3/31/01 = 10.3 Trillion

GDP 9/30/10 = 14.73 Trillion

US total Public Debt Outstanding 3/31/01: 2.10 Trillion

US total Public Debt Outstanding 9/30/10: 4.65 Trillion

Nominal GDP growth = 4.43 Trillion (43%)

Nominal US total public debt growth = 2.55 (121%)

Unless Mr. Rogan has become a Keynesian, one would have expected him to argue that had the US total public debt growth (and government spending in general) been smaller, the Nominal GDP growth would actually have been larger. It's peculiar that he's arguing the opposite.

Gary Rogan responds:

Rocky, take a look at the chart at the top of this article (a few months ago, but still) and you will realize that there is more than one definition of "US public debt" and some come closer than others to matching my statement.

I did not argue one way or another about what would happen had the overall government borrowing not been so large. I will argue, or rather state, now that in order for the free market forces to act to restart the non-subsidized GDP growth we would have had to experience a rather severe, non-government-corrected recession to clean out all the malinvestment of the last 15+ years. I will also state that not only had there not been any Keynesian multiplier on the government spending in a "greater than 1" sense for a while, but lately that multiplier has collapsed to a rather small fracton. Nevertheless, even now if you borrow and spend you will raise the GDP by more than if you don't borrow and spend. Nothing particularly Keynesian there.

Nov

12

Notes from Jakarta, from Jan-Peter Janssen

November 12, 2010 | Leave a Comment

Notes from Jakarta:

#1. Fresh is better. Alive is the best. Asians know. Buy newly caught fish directly from a fisherman . Super markets are no no. Poultry shall be bought alive. Meat shall come from a wild animal. Learn to hunt or get to know a hunter.

#2. Let chefs do the cooking. Unless you're willing to slaughter chickens yourself, that is.

#3. Don't BBQ with charcoal. Indonesians use pieces of dried coconuts. Tastes much better. If you don't have ample supplies of coconuts, experiment with various kinds of wood.

#4. Do as the locals. Indonesians don't sit at the table. They sit ON it . Local traditions add flavor to the BBQ experience.

Nov

12

Dominant Social Themes, shared by Gary Rogan

November 12, 2010 | 2 Comments

Dominant Social Theme from thedailybell.com

Dominant Social Theme from thedailybell.com

A dominant social theme is a belief system (usually concerning a purported social or natural problem) launched by the monetary elite that grows into an archetype or meme, usually after much repetition. The problem may be centered on people themselves (overpopulation) or caused by people (global warming). Dominant social themes often are launched from the centers of the power elite's global architecture, including the United Nations, World Bank, World Trade Organization and World Health Organization, where the related problems are declared to be such. The themes are then rebroadcast by the mainstream media. The hallmarks of a problem that drives a dominant social theme are:

• The problem is presented as one that can be solved only by those in authority.

• The prescribed solution requires action by, and greater authority for, social and political institutions that are distant from the societies they pretend to benefit.

• Reminders of the problem persist no matter how much evidence appears that the problem is fictitious, trivial or irremediable.

• The problem may co-exist in the public's mind with other purported problems with which it is inconsistent.

The United Nations is an example of an authority-based solution to a problem proposed by a dominant social theme. The problem is international conflict, including war. The solution is for national governments to be made subject to a worldwide authority.

The European Union is the United Nations writ small. The problem is isolated national markets and a lack of economic cooperation. The solution is for the national governments of Europe to be made subject to a European authority. Other examples of problems that support dominant social themes are: Bird flu. Even though it is rarely communicable from human to human, the disease is promoted as an extraordinary problem by emphasizing the high rate of mortality among the few people infected. This encourages the militarization of health care, supports planning for a "state of emergency" in Western countries and makes quarantining entire populations acceptable to the public. It also enriches Big Pharma and its shareholders by creating demand for vaccines and other drugs.

Swine flu. This disease is the thematic complement of bird flu. Even though the mortality rate is unremarkable by the standard of seasonal flu, the disease is promoted as an extraordinary problem by emphasizing the ease with which it is communicated from human to human. This encourages the militarization of health care, supports planning for a "state of emergency" in Western countries and makes quarantining entire populations acceptable to the public. It also enriches Big Pharma and its shareholders by creating demand for vaccines and other drugs.

Peak oil: Belief that oil supplies are on the verge of exhaustion justifies rising oil prices, for the benefit of producers, and provides a rationale for energy-efficiency regulations (to the benefit of certain manufacturers) and for subsidies for companies involved with "alternative energy" (biodiesel, solar, wind power and others). It also supports the promotion of public companies associated with energy alternatives.

Central banking: The idea that depressions are caused by free markets and by constraints on the supply of money imposed by a redeemable currency support the necessity of giving unlimited discretionary power to central banks that preside over fiat currencies. The manipulation of the fiat currencies can generate enormous wealth for favored parties.

The creation and exploitation of dominant social themes has been aided by the growth of modern, centralized mass media. The Internet, which decentralizes the power for mass communication, threatens the ability to invent and control dominant social themes.

Nov

11

Leave It to the Stock Exchange’s Second Biggest Faker, from Victor Niederhoffer

November 11, 2010 | 7 Comments

Leave it to the stock exchanges second biggest faker to send the market tanking on a shortfall and dissimilitude. It's the confrontation with reality that occurs whenever he speaks that makes one realize "how could I have been such a fool to believe in him when I knew all the time he was like that." Such revisions of hopeful feelings are common in the market and life and seem to cause what used to be called agonizing reappraisals. Other personages that cause this when they are shown to be without substance or window dressing their positions on could be predicted to be the Sage or …

Nov

11

In Flanders Field, from Jim Lackey

November 11, 2010 | Leave a Comment

.jpg) In Flanders Field

In Flanders Field

by John McCrae

In Flanders Fields the poppies blow,

Between the crosses, row on row,

That mark our place; and in the sky,

The larks, still bravely singing, fly,

Scarce heard amid the guns below.

We are the dead.

Short days ago,

We lived, felt dawn, saw sunset glow,

Loved and were loved and now we lie,

In Flanders Fields.

Take up our quarrel with the foe

To you, from failing hands, we throw,

The torch, be yours to hold it high.

If ye break faith with us, who die,

We shall not sleep, though poppies grow,

In Flanders Fields.

Check out this site about the VFW Buddy Poppy Program in honor of Veterans Day. Give a few bucks, and hang it off your rear view mirror.

By the way, another Moe, Richard (who served in the House), is the author of the best unit history from the Civil War. It is about the First Minnesota.

Nov

11

Gary Johnson in the News, from Victor Niederhoffer

November 11, 2010 | 2 Comments

Follow up from a friend of Aubrey who climbed Mr. Everest with a broken leg, and vetoed more bills than all other Governors combined when in office:

"Forget Palin, here's Gary Johnson"

from CNN.

Nov

11

Oil Prices, from Stefan Jovanovich

November 11, 2010 | Leave a Comment

Is there any validity to this type of analysis?

Is there any validity to this type of analysis?

Price of Sperm Oil (in gold dollars) - Eaton, "Petroleum"

1831 $0.30

1843 $0.63

1854 $1.92

1866 $1.28

The explanation of the price drop in 1866:

"This posed (and contrived) photograph was taken by John A. Mather in the Pennsylvania oilfields, probably in 1866. It was the year of a bust, a phenomenon that visits the industry from time to time. The price of crude dipped too low for profits in 1866 and forced some operators to sell or even abandon their equipment."

Rocky Humbert writes:

At the risk of eliciting hate mail from my libertarian friends, I make two observations where the government can actually help things along:

1) Short and Long-tail externalities. Markets are ill-suited to efficiently allocating the costs of mass torts such as pollution (and man-made climate change — should it ever actually pass muster beyond any reasonable doubt). I submit that correctly applied, Pigovian Taxes improve societal outcomes, and challenge Libertarians to argue otherwise.

2) Dissemination of truthful versus fraudulent information. It's difficult to imagine that anyone still believes that smoking is not unhealthy. It was in 1963 when the original surgeon general's report reported the links between smoking, cancer and heart disease. For forty years, the tobacco industry labored feverishly to prove otherwise, and their attempts at some points came periliously close to fraud and perjury. One can reasonably argue that it should not be the government's role to interfere with a fully-informed smoker's choice, but it's a much different argument to say that the smoker should be misinformed. The incremental value from cigarette packs displaying pictures of dirty lungs and dying children is questionable — which demonstrates the saying "too much of a good thing isn't a good thing"

Which brings me to the restaurant menus in NY which must now display calorie counts…. During a recent visit to Ben & Jerry's, I winced when I read that the awesome fully-loaded Brownie Sundae had 1800 calories, and this information certainly contributed to my decision to get the small mint chip cup instead. The cost to Ben&Jerry of proving this information (other than in lost sales) is small, and my "informed decision" was probably healthier — yet, this additional knowledge certainly reduced my enjoyment of the ice cream experience. I recently read that Obamacare mandates that vending machines display calorie counts (for owners of 20+ machines), and the vending machine owners are (perhaps rightly) upset about the costs of complying with these new regulations. Once again, "too much of a good thing isn't a good thing."

Gary Rogan writes:

The government can do a lot of good. There are many well-meaning people in government, and since it expends enormous resources it produces a lot of good. You got close to the crux of the matter towards the end: WHO should decide if the cost or the action or in fact the action itself (in resources and restrictions on freedom) is worth it? Can they reliably make the right choice? What happens when they make the wrong choice with all the firepower that stands behind them?

Nov

11

What a Speculator Is, from George Parkanyi

November 11, 2010 | 1 Comment

What has being liberal, libertarian, vegetarian or whatever got to do with being a good speculator? In my mind a speculator needs to explore and understand how the world is, rather than how he wishes it to be. If the world if full of bleeding-heart blood-sucking socialists, then figure out how to speculate successfully under those conditions. Or if it's full of profit-at-all costs exploitive blood-sucking capitalists, figure out how to speculate through that. Who cares (as a speculator) if paper currency is going to become an environmental problem. Should one be buying gold? And/or timberlands? Speculation is little more than a game really. You're dealt a hand– figure out how to put it to best use. Influence the game if you can. If someone else isn't playing by the rules– adapt. Be creative, resourceful.

What has being liberal, libertarian, vegetarian or whatever got to do with being a good speculator? In my mind a speculator needs to explore and understand how the world is, rather than how he wishes it to be. If the world if full of bleeding-heart blood-sucking socialists, then figure out how to speculate successfully under those conditions. Or if it's full of profit-at-all costs exploitive blood-sucking capitalists, figure out how to speculate through that. Who cares (as a speculator) if paper currency is going to become an environmental problem. Should one be buying gold? And/or timberlands? Speculation is little more than a game really. You're dealt a hand– figure out how to put it to best use. Influence the game if you can. If someone else isn't playing by the rules– adapt. Be creative, resourceful.

Everyone should of course nurture and grow a life philosophy and be able to freely pursue it (although I personally don't agree with anyone trying to impose theirs on others, including parents). This of course can influence why and how you speculate, but I think its the individual's application of intellect and effort rather than the philosophy itself that determines the success.

Just my two cents. No– four cents. Is it four yet? (Where the hell is gold trading now? … Haha. )

Kim Zussman writes:

It is the rare person who can bet and profit from the opposite of their own belief system. Imagine going against your own G-d, your people, your family, your children– because intellectually you believe they will lose and you will pay any price to be on the profitable side of the bet.

Faustian abitrage

Nov

10

One Admires, from Victor Niederhoffer

November 10, 2010 | 2 Comments

One admires the insouciance, the shiftiness, the redeployment, the false signaling, the appearance of propriety, (what is the right expression?) with which the Fed announces their schedule of securities eligible for their quantitative easing at 2:00 pm. this afternoon. They wish the "flexibility " to buy the highest yielding securities from the bank so that they can "give the public" the best return. What a snare and delusion, a displacement, a false marking et al, to displace attention from fact that they are buying a trillion dollars of securities by force from the clients that own them, adding to the demand schedule by 100% or so with every security always fairly much the same shift from each other so that buying one raises the price of all others to their clients non animadversion.

One admires the insouciance, the shiftiness, the redeployment, the false signaling, the appearance of propriety, (what is the right expression?) with which the Fed announces their schedule of securities eligible for their quantitative easing at 2:00 pm. this afternoon. They wish the "flexibility " to buy the highest yielding securities from the bank so that they can "give the public" the best return. What a snare and delusion, a displacement, a false marking et al, to displace attention from fact that they are buying a trillion dollars of securities by force from the clients that own them, adding to the demand schedule by 100% or so with every security always fairly much the same shift from each other so that buying one raises the price of all others to their clients non animadversion.

Nov

10

Symmetry, from Jim Sogi

November 10, 2010 | Leave a Comment

Very symmetrical shaping in ES over last couple weeks. Symmetry seems to be one of the underlying principals of the universe, to put it most broadly. Eastern philosophy calls it yin and yang.

Nov

10

Thought of the Day, from Jeff Watson

November 10, 2010 | 2 Comments

In this article I recently read, "Oil Will Run Dry 90 Years Before Substitutes Roll Out, Study Predicts", Dr. Niemeier says, "We need stronger policy impetus to push the development of these alternative replacement technologies along." Spoken like a true statist who depends on government largesse and central planning.

In the real world, what we need is for there to be an incentive, as described by a real price, and the free market will find a solution to the oil depletion, in short order.

Nov

10

The Power of Double Check, from Ken Drees

November 10, 2010 | Leave a Comment

This morning's lesson with my son involved a mate on the move problem with double check being the application.

This morning's lesson with my son involved a mate on the move problem with double check being the application.

The power of ++ is that it removes two of three methods of check deflection from the king's choices– interpose and capture and forces the king to move. Aron Nimzowitsch wrote that, "Even the laziest king flees wildly in the face of a double check." And I kept the lesson up as we waited for the bus adding on that the ++ always involves a discovered check (a surprise) and that it even gives the checking player a "tempo" in that the opponent is forced to flee and not make a truly organic move and now this lesson has percolated into thinking about markets.

Now in silver was the raise of requirements of margin the discovered check, and the piece that moved out to create that discovery was the price of silver itself? This example maybe doesn't work so well as a double check, but simply a discovered check. Or a certain stock was moving very aggressively higher and then a surprise downgrade premarket occurred. Was the potential downgrade that was aiming all along at the stock price hidden and then revealed at a critical time

For a double check scenario–maybe hike of margin requirements and a new contract amount limit rule being imposed at the same time would be more appropriate. Causing extreme contract liquidation (a move by the king only).

Double check in markets is interesting and in my opinion is associated with a negative ( a check) to the rising item. A surprise inclusion of a stock into an index combined with a stock split may be an upside example of double check. One more facet of double check is that the piece you move or even the piece giving the discovered check can be left enprise or at risk for the move, giving the ability to extend the piece's power and range –a springboard of sorts. A suspension of consequence for a short time.

Nov

10

A Useful Thought For Today, from Rocky Humbert

November 10, 2010 | Leave a Comment

The Waverly Advisors morning note commented on yesterday's precious metals markets. Their observation is relevant to all markets at all times:

"In practical "trader's terms", it boils down to this: These markets are certainly overextended by any measure, and, as such, are vulnerable to corrections. Because of the potential for new feedback loops, these corrections may be larger, sharper, and more irrational than most market participants expect. In short, expect the unexpected and do not be caught off guard. Though yesterday's action could set off a larger pullback, we see nothing to challenge the integrity of the higher timeframe trend, and weakness in these markets is to be bought until further notice."

Mental note to self: Make sure that I am on the distribution list for the "further notice."

Anton Johnson writes:

Consider further notice given: See CME silver margin increase.

Victor Niederhoffer comments:

Further notice with bonds going through 30 year auction. Will they be able to pull rabbit out of the hat, especially considering recent failures. My goodness, the clients might have a loss.Let us hope that any announcements of a negative nature will be released before the auction so as not to upset the sensibilities as usual.

Anatoly Veltman asks:

1. I never looked up Waverly– are they good?

2. Silver hit $29.34 Tuesday. It is back over $28 this minute. Please don't lose sight of history. November two years ago: $9. Watch out this week (comes from a fool with $1m in margin money leveraged 30:1 on the day Silver dropped from $11.25 to $7.50; and traded even lower next day!)

Nov

9

The Flexis and the Vigis, from Victor Niederhoffer

November 9, 2010 | 1 Comment

No sooner said that increase in inflation expectations might change the schedule of flexionic payments, then bonds go to a 3 month low. The vigilantes finally do their thing.

Vince Fulco writes:

Especially on a day when the former Harvard head said the Fed "needs to do much more".

Ken Drees comments:

Back to back red days per dailyspec calendar– recently rare.

Nov

9

Briefly Speaking, from Victor Niederhoffer

November 9, 2010 | Leave a Comment

I recently played with Aubrey at the new Stuyvesant park on West Street. It illustrates many things that made America great and are appropriate to think about relative to the well known abundance that giving each settler his own plot gave to the pilgrims enabling them to have a Thanksgiving. Everything is better now. Think back to the catalogs you used to order from 10 years ago, and see if there's anything you would buy. Not only in electronics, but in toys , gifts, cosmetics. The park has products from Kompani and Berliner– that are infinitely safer and more playful than the old parks. The ropes of the jungle gym protect the kids from falling and doubtless save hundreds of lives a year. The artificial soft turn prevents thousands of deaths a year from concrete and asphalt accidents. All the equipment turns and jumps with unbreakable springs. The plastic that Kompani uses is infinitely safer and more playful than the splintering and depreciating wood that our kids grew up on. How many things are infinitely better now than they were 20 years ago.

I recently played with Aubrey at the new Stuyvesant park on West Street. It illustrates many things that made America great and are appropriate to think about relative to the well known abundance that giving each settler his own plot gave to the pilgrims enabling them to have a Thanksgiving. Everything is better now. Think back to the catalogs you used to order from 10 years ago, and see if there's anything you would buy. Not only in electronics, but in toys , gifts, cosmetics. The park has products from Kompani and Berliner– that are infinitely safer and more playful than the old parks. The ropes of the jungle gym protect the kids from falling and doubtless save hundreds of lives a year. The artificial soft turn prevents thousands of deaths a year from concrete and asphalt accidents. All the equipment turns and jumps with unbreakable springs. The plastic that Kompani uses is infinitely safer and more playful than the splintering and depreciating wood that our kids grew up on. How many things are infinitely better now than they were 20 years ago.

What causes this? Incentives, competition, specialization and trade. I must improve on this thought for my annual thanksgiving message based on the incentives that Governor Bradford provided.

Russ Sears writes:

While one would hope that there is truth in this post, I believe the closer you look the more you see this is the incentive of government in charge of most parks and hover parents, not a free market. Parks often are most concerned with preventing lawsuits, rather than the entertainment or the education or even the holistic physical well being of the kids. Gone are the Basketball goals, the volleyball nets, and the score of competitive sports played on baseball field that encourage kids to casually compete, testing who is best. Even a kid Aubrey's age understands when helmets are good and when they are for show and support of over protective parents.

It is outside the parks system. To find the free market and true innovation you must go to the mountain climber, the bicyclist, the hikers, the campers, and even running specialty stores. There kids are thought to take educated risks and how to swing the odds greatly in your favor, to have a great time and live life fully in true freedom. These store are amazing places with gear that would stun a Rip Van Winkle awakened from a 20 year nap.

Rocky Humbert writes:

Each year, emergency departments treat more than 200,000 children for playground-related injuries.

Each year, emergency departments treat more than 200,000 children for playground-related injuries.

And from 1990 to 2000, 147 children aged 14 and under died from playground-related injuries. 56% died from strangulation and 20% died from falls. This may not seem like a troubling statistic, unless it's your kid that hit the ground at terminal velocity.

I submit that the Plaintiff's Bar is the "unsung hero" in playground safety evolution.

Russ Sears adds:

How many of increasingly obese, depressed, apathetic and unambitious youth and young adults are there through lost opportunity cost? Like the FDA, let us never forget "safety" has a hidden cost. In fact it could be argued that the bubble in safe AAA bonds was the fuel that allowed the housing bubble to start, grow and explode.

Jeff Watson writes:

You're right that most things have improved in science kits and electronics. However, chemistry sets have gotten worse, although they are much safer. My old Gilbert set from when I was a kid had a much wider range of experiments and greater variety of chemicals than any set today due to the legalities and regulations. Although I love the new electronics kits, the old Allied Electronic "Knight Kit 200" was the best electronic kit I ever played with because it was a breadboard and even had a solar cell. I tried my hand at designing simple circuits with this kit and always had a propensity to blow out .01uF ceramic discs due to my adventure.

You're right that most things have improved in science kits and electronics. However, chemistry sets have gotten worse, although they are much safer. My old Gilbert set from when I was a kid had a much wider range of experiments and greater variety of chemicals than any set today due to the legalities and regulations. Although I love the new electronics kits, the old Allied Electronic "Knight Kit 200" was the best electronic kit I ever played with because it was a breadboard and even had a solar cell. I tried my hand at designing simple circuits with this kit and always had a propensity to blow out .01uF ceramic discs due to my adventure.

Victor Niederhoffer replies:

I disagree with you. The Kosmos Chem 3000 is infinitely better as are the snap tech kits much better than allied or radio shack. You must come and see the new science curricula that Kosmos provides.

I disagree with you. The Kosmos Chem 3000 is infinitely better as are the snap tech kits much better than allied or radio shack. You must come and see the new science curricula that Kosmos provides.

Jeff Watson elaborates:

The nice thing about the old Allied 200 in one kit was that it was a breadboard kit and used 110VAC with a multi tapped transformer. The breadboard came with plenty of extra connectors and I could add all the extra resistors, capacitors, transistors, coils, chokes, diodes, tubes, etc, that I could scrounge from old TV sets etc. The new kits just don't allow that flexibility, at least from what I've seen online etc. I still have that old kit and taught John the rudiments of basic circuitry when he was a kid. That kit is so old, I had to change out all the electrolytics and put in a new transformer as components change values with age. In my case, all the science and electronic kits I had ended up getting heavily customized by me, and they never resembled the original after a few days.

Victor Niederhoffer writes:

Yes. But that's infinitely more difficult and harder to learn and attach the springs than the snap-ons, which come with all those components and educational sets keyed to actual curricula.

Jeff Watson counters:

I know that the springs are harder, but they worked for me. When I was a kid, I never followed a curriculum, but by 5th grade, I was looking at schematics in Popular Electronics and building workable models on my Knight Kit breadboard. I made many improvements to their schematics and sent them to the magazine and I was published and rewarded with a free subscription. My tweaks weren't much, but for a 11 year old kid, they were pretty cool and left me with a sense of accomplishment. I never did much digital as it wasn't around then, but when I was a freshman in college, I remember studying "Digital Electronics for Scientists" by Malmstadt. Good book that is dated but still useful today.

Nov

9

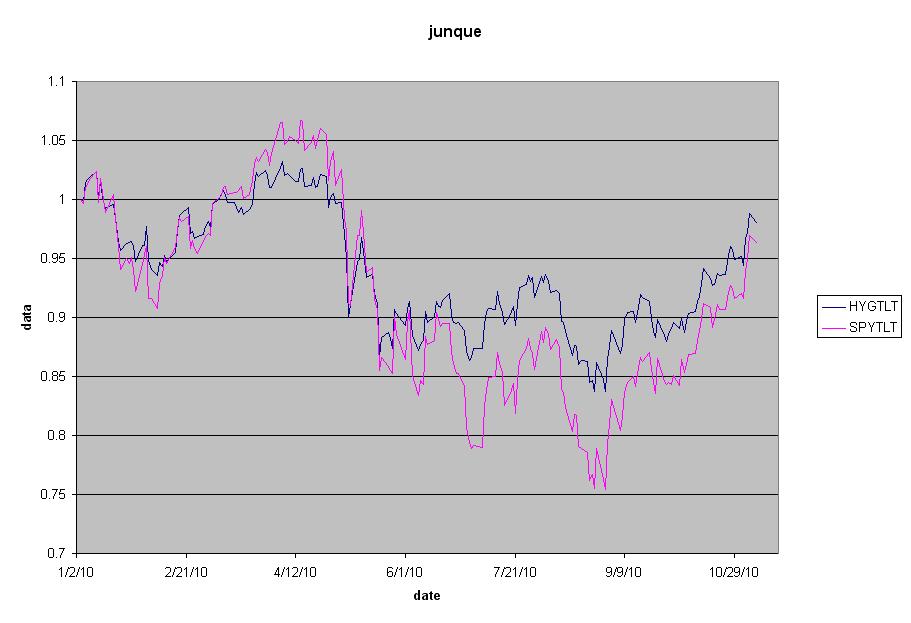

Junque, from Kim Zussman

November 9, 2010 | Leave a Comment

The attached chart plots two ratios from Jan 2010 to present: high-yield bond etf (HYG) / long-treasury bonds (TLT), and SP500 (SPY) / TLT.

From a "risk free" (free at last!) rate of return standpoint, neither junk nor stocks have gained YTD. Both dipped prior to Ben(ding) Over, with stocks showing more risk free volatility (higher high and lower low) than junk.

Nov

9

Commodity Curiosity, from Rocky Humbert

November 9, 2010 | Leave a Comment

The "greatest" stock market bull run began in 1982, and in the subsequent five years, the Dow Jones increased by roughly 2.7x. The bull was interrupted by the October 1987 crash (36%), and it took almost exactly two years for the Dow Jones to reclaim its previous record high. The prologue from 1989 to 2000 needs no recounting.

The "greatest" stock market bull run began in 1982, and in the subsequent five years, the Dow Jones increased by roughly 2.7x. The bull was interrupted by the October 1987 crash (36%), and it took almost exactly two years for the Dow Jones to reclaim its previous record high. The prologue from 1989 to 2000 needs no recounting.

The current commodity bull run began in 2003, and in the subsequent five years, the CCI Index (Continuous Commodity Index) increased by an eerily similar 2.7x. This rally was interrupted by the commodity crash of 2008 (42%), and it's taken a eerily similar two years for the CCI to reclaim its previous record high. The prologue of the current commodity bull market has not yet been written.

Lest you accuse me of sounding like Jimmy Rogers, please note that I do not speak with a Southern Drawl (nor do I wear bowties.) I do, however, note that EVERY modern easing cycle has been coincident with some asset prices achieving prices where one rubs one's eyes and exclaims, "Darn– why didn't I own more of THAT stuff!!

"The story doesn't change. Only the Bloomberg quote symbol.

Nov

9

A Market Stew, from Ken Drees

November 9, 2010 | 1 Comment

1. –qe2 now bad, good, needed, loathed, ok, in a box, maybe not have to do it after all if inflation shows up. qe3 qnd qe4?

2. –china raising rates again, no like qe2, no like Japan, rare earth tough luck, don't tell us about our currency float.

3. –commodities going up and up and up–and oil is lagging, silver was rigged all along (who knew), copper hot, cocoa yummy, and yellow cake.

4. –gold keeps on keeping on and all that broken jewelry already melted for cash.

5. –Bam on the run (is he coming back?) —tax hikes coming, health care costs a coming, no cola to wash down high prices. Bam parties on!

6. –nat gas flickering–Rocky's indicator?

7. –jobs, no jobs, unemployment stuck, 99 weeks over with repubs in, states unhappy, state govs cutting jobs, local gov cutting jobs.

8. –iran, israel—where did that go? Oil back almost to 90.

9. –europe rebails coming? — bailouts ok here but usa qe2 is bad example.

10.–dollar breathing heavy. dollar this - dollar that, everyone (brazil too) talking about dollar. the dollar is linked into every trade on the face of the planet (cnbc).

11.–inflation is low under 2% and Ben wants above 2% shadow stats says inflation already 6% can we handle a fed 2%+ number?

12.–qe2 is a blunt tool and that causes bubbles in other asset classes–stone knives and bearskins—how can we work with these tools?

13.–housing is wrecked. rico coming, can't foreclose, can't sell, can't redo mbs now, fannie needs more money.

14.–"Structural" used as modifier for (unemployment, pipeline inflation, housing problems, lack of gdp growth, dollar woes)

15.–Bonds—do they matter, like deficits? Poor ranting Santelli– get over it Rick.

16.–Stocks are being targeted by the fed for pumping. We all know that this means we are good to go. SPY up 9 out of last 10 weeks.

17.–GM — gotta float the big gov boat. Its simply a question of perfect pricing.

18.–Holidays are coming, year end coming but no one is selling. The market buried the hindenburg indicator!

19.–G20—so what.

20.–Hillary, what is she doing? What about Bam's cabinet —more change coming?

21.–3-5 banks closed every weekend–so what, who cares, old news.

22.–lot of cash still on the sidelines. where is it going—everywhere!

23.–holding cash is stupid says Cramer–a bonehead move.

24.–its a GLOBAL thing now –we are all in this thing, a simmering market stew.

25.–Lets look towards 1st quarter earnings–there is nothing else to think about.

Nov

9

Gold/Silver Bulls, from Anatoly Veltman

November 9, 2010 | 3 Comments

Gold/silver bulls are getting sloppy again, now at $1410/ $27.73. Silver has been the catalyst for this entire two-month leg up, crowning a whopping $10 move during this time frame. At the start of this Tuesday's session, however, the Bulls ought to be cautious. Just like with that $3.50 Dec NatGas print early in Oct.25 session - the daily charts are going parabolic!

Gold/silver bulls are getting sloppy again, now at $1410/ $27.73. Silver has been the catalyst for this entire two-month leg up, crowning a whopping $10 move during this time frame. At the start of this Tuesday's session, however, the Bulls ought to be cautious. Just like with that $3.50 Dec NatGas print early in Oct.25 session - the daily charts are going parabolic!

I would be heeding the following alarming factors, as Gold and Silver futures sit at record highs tonight:

1. USD has been firming in last couple of sessions - but Gold and Silver still rallied to records. Bulls will argue that this a positive divergence, pointing to "independent strength". I suspect that this, in fact, may be pointing to forced short-covering; and thus, less of the forced short-covering remains to be executed!

2. Platinum and Copper did not follow Gold, Silver and Palladium's move to new highs Friday and Monday. I would note muted response in Crude and grains as well. The only other commodities that continued parabolic were the leading stars of the period: Cotton and Sugar. Again, another sign of forced short-covering well in progress.

3. Significant news of QE2 and elections are done with, and precious metals have just tacked on more gains.

4. Chartists know that, following a lengthy run, a commodity that continues parabolic at week's start risks a powerful intra-week reversal. Those types of "outside reversals" on the Weekly are much more potent, in my observation, than the ones on Daily. When Gold futures chart-painted that "shocking" intra-day reversal from $1366 to $1326 on October 7, that made me temporary Bullish. I shall not be Bullish if something like "outside reversal" will be painted on Weekly chart.

5. Another chart complication will be caused by semi-holiday week, with Veterans Day shutting the Treasury markets on Nov.11, and taking bank and Fed personnel out of the office.

Rocky Humbert writes:

I would be heeding the following factors:

1) The record high in silver was approximately $41.5/oz on January 21, 1980. That's approximately 49% higher than the current price. Anatoly's statement (regarding silver) is wrong.

2) That gold just made a record high is not predictive but it does prove a simple fact. EVERY gold long is sitting on a profit. And every gold short is sitting on a loss. That's not a recipe for bullish capitulation.

Anatoly is continuing to demonstrate a FleckenAbelGrantian personality disorder. Eventually, he'll be right. But eventually is a long time.

In contrast, I just stay long gold and roll up my puts every $50 or so. I wish I could say that I'm smart, but I'm not. The objective of speculation is making and preserving profits. Not sounding erudite. See this post.

Anatoly Veltman responds:

Rocky's comment is educational. Rocky advocates buy-and-hold (on way up)/sell-and-hold (on-way-down) vs. market timing. Excellent subject for separate thread, and I'm sure such thread will attract wide participation.

To return to this week's Gold/Silver situation, I'm attempting to be ready for this particular charting set-up: outside reversal on Weekly chart. Due to Nov.11 semi-holiday, such weekly bar may be painted this week OR it may take a combination of this week's and next week's bars. Monitoring many liquid markets over the past 24 years, I found such pattern to often mark longer-term reversals- and thus worthy of being prepared.

Why anticipate (rather than follow), and how?

1. A Gold/Silver bull wants to hold Long exposure. Following rapid price jump, his dilemma may be similar to bear's: how to stay with his biased position. One definition of up-trend - higher highs AND higher lows - will be threatened by trading below $1315 or below $1160, depending on trader's intensity. Both marks are too far below, when trading $1410-1425. Thus bull's dilemma is very real: historical cost should never be used in analysis of a liquid trading instrument– you're basically marked-to-market every single $1 move, if not every 10 cent tick. Is this a good plan to hold Long at $1410-1425, if a drop below $1315 will cause you to sell out and possibly reverse to Short? Or even lower, below $1160?

2. One shouldn't ALWAYS try to anticipate every outside price path. Hints are essential to go on ALERT. Fri and Mon Gold/Silver/Palladium jump against stronger USD gave a hint of "forced" short-covering in progress in those particular metals, while other remained calm. Stubborn Cotton and Sugar rocket, while other commodities do little– is another sign of "forced" short-covering. The more short-covering is done, the less remains to be done.

3. I confess that lately my analysis lacks previous complexity, as I just observe/comment and have no vested interest. To duly gage possible trade exhaustion, one-dimensional PRICE charting is not enough. One absolutely must employ second dimension of daily OPEN INTEREST change, and ideally third dimension of changes in Open Interest MAKE-UP (i.e. Commitment of Traders). My current guesses are much less scientific than I'd like– they are just a heads-up.

Nov

9

Paper Cups as an Economic Indicator? from Alan Millhone

November 9, 2010 | Leave a Comment

Hello Everyone:

Hello Everyone:

Today I stopped at Third Street Deli. I have dined there for many years. I always have their iced tea. Up until today they gave you a sturdy plastic cup with their name and logo on each cup with bright green lettering. Today they have begun using a mediocre generic paper cup. I asked if out of the others? Was informed it was a 'cut back' .

Regards:

Alan

Victor Niederhoffer comments:

I think the paper cup may be much healthier. This reminds me of the purveyor of paper cups for Dannon yogurt that owned the old dixie cup plant that I was trying to sell. They told me they had a lock to grow exactly as Dannon did because Dannon needed their cups. I asked, "what about all the colorful plastic cups the other yogurts are beginning to use?" "No way," they said, "yogurt can't be sold in plastic cups because it doesn't taste as good or ferment as well."

Shortly thereafter the company was 1/5 its former 15 mm size. A strange follow up came when I read Roger Kahn's book about running a minor league team. Roger accroding to Larry Ritter was an egomaniac who fancied himself a great baseball player and tried to place it prominently in every book. But Roger found a backer for his minor league team. It was the same owner who assured me nothing could go wrong with the dixie cup. They fought like cats and dogs, and the book makes a hilarious reading as the two of them tried to impose their will on a down trodden minor league team with all the problems of selling ice cream and peanuts and programs to cover the salaries. Paper cups look pretty good in my book.

Nov

8

Day Trading, from Larry Williams

November 8, 2010 | 4 Comments

Trend is the basis of profits; no trend, no profits.

Trend is the basis of profits; no trend, no profits.

Trend is a function of time. 3-5 hours does not allow for trend moves of any real magnitude; day traders play with a stacked deck. The dream of daytrading is in fact a nightmare for most everyone. It can be done, but not for massive profits.

Nick White writes:

There is an excellent discussion of the dynamics of this point in the gentleman from Amioun's first book.

I quote / summarize / paraphrase at length:

Take a regular dentist. A priori, we know he is an excellent investor and has an expected annual return of 15% over t-bills with a vol of 10%. Dentist builds a trading room in his attic, deciding to spend every day watching the market and drink cappuccino. He buys a bloomberg and lots of expensive PC's to automate his trading etc etc. His 15% return with 10% vol per yr translates to a 93% probability of success in a given year. But seen at a narrow time scale, this translates into a mere 50.02% probability of success over any given second. OVER THE VERY NARROW TIME INCREMENT, THE OBSERVATION WILL REVEAL CLOSE TO NOTHING,. Yet the dentist's heart will not tell him that. Being emotional, he feels a pang with every loss, as it shows red on his screen.At the end of each day, the dentist is knackered and emotionally drained Minute by minute examination shows that each day (given 8hrs / day) he will have 241 pleasurable minutes against 239 unpleasant ones. These amount to 60,688 and 60721 per year. Given that an unpleasurable minute is worse in reverse pleasure than the pleasurable minute is in pleasure terms, then the dentist incurs a large defecit when EXAMINING HIS PERFORMANCE AT HIGH FREQUENCY. In contradistinction, imagine the situation where the dentist examines his portfolio only upon receiving the monthly account from the brokerage house….67% of the months will be positive, he gets only four negative pangs of pain per year, and eight uplifting ones. THe efffect is magnified at the annual level where, for the next 19/20 years, he will have a pleasant experience looking at his annual statements.

Scale Probability

1yr 93%

1 qtr 77%

1 mth 67%

1 day 54%

1 hr

51.30%

1 minute

50.17%

1 second

50.02%

The net net of all this is as follows:

If we look at the ratio of noise to non-noise then you get the following. Over one year we gets .7 parts noise for every part of performance. Over one month we get 2.32 parts noise per part of performance Over one hour, 30 parts noise for every part performance Over one second. 1796 parts noise per part of performance. Therefore:

Over short time increments, one observes the variability of the portfolio, not the returns…you just see variance and little else. This is emotionally difficult to parse…even though at any moment you see a combination of both variance and return, your brain can't tell the difference. This explains the burn-out rate amongst people who constantly expose themselves to randomness (especially given greater effect of negative experiences than positive experiences).

Kim Zussman writes:

The analysis is flawed:

1. A regular dentist should not day trade because of opportunity cost and squandering what he paid for his profession's barrier to entry

2. One can only know their returns ex post. If you could know them ex ante there would be no psychological issues - fear comes from uncertainty.

3. Irregular dentists are another story

Rocky Humbert writes:

Kim writes: "If you could know them ex ante there would be no psychological issues– fear comes from uncertainty."

This is not correct.

Fear is a pre-wired response in most people, and can have little to do with the rational analysis of a situation or uncertainty.

Example 1: While waiting to mount an extreme amusement park ride (roller coaster etc), the symptoms of fear (sweating, elevated pulse, etc.) are a genuine physiological response regardless of the fact that the odds of injury on the ride are miniscule.

Example 2: If you are engrossed while watching a horror movie, your limbic system kicks in … just as if you were being chased by the Blair Witch.

Example 3: Phobias are real, and irrational. A person who is afraid of flying is not interested in the fact that his plane will almost certainly not crash. Yet, people are not afraid of driving to work — even though the odds of dying during a commute are much higher than on a cross-country flight.

The emotional fear/greed response to P&L mark-to-market are real– and I believe genetically pre-disposed. They are analogous to phobias and obsessive-compulsive disorders. Hence, I believe Nick's post about timeframes is extraordinarly profound and accurate.

Nov

8

An Interesting Chart, from Victor Niederhoffer

November 8, 2010 | 2 Comments

There's an interesting chart illustrating Livermore's point that when a market goes above a round number (1000) it is bullish. Gold approaching 1400, - round numbers at 1200 were temp turning point but runs through other 100s show no tendency to reversal. A whole study has to be done with as is data on individual stocks.

Alan Millhone writes:

All I know is reg gasoline over three now and killing the average citizen. Gold will push two the way things are faltering.

Ken Drees writes:

I am not hearing the gas price complaint yet as it seems that many are very conditioned in the high 2's and even the low 3's may seem not worth complaining about.

I think a round "4" handle on the gas price will start up the wailing and gnashing of teeth this time around.

Sam Marx prophesies:

$4 gasoline will occur at or before the 2012 election.

Nov

8

Bambi Syndrome, from T.K Marks

November 8, 2010 | Leave a Comment

I finished reading a fine book last evening, and one of its closing philosophical points made me think of an old friend, Doug. It involved hunting, and his explanation one time to me that uninformed opponents of such appear to be burdened with some sort of Bambi Syndrome. Also known as BS, in the jargon of clinicians.

I finished reading a fine book last evening, and one of its closing philosophical points made me think of an old friend, Doug. It involved hunting, and his explanation one time to me that uninformed opponents of such appear to be burdened with some sort of Bambi Syndrome. Also known as BS, in the jargon of clinicians.

That is, the overwhelming majority of these opponents would have no problem with consuming mass-produced animals, but are seemingly appalled when somebody else more humanely cuts out the middleman, and cramped cages and pens.

That is a more than fair observation as there would seem to be an obvious paradox at work here. And probably one with parallels to other endeavors as well, which is why it is always prudent not to be reflexively judgmental about things about which we may not readily understand.

The person in the book echoing Doug's point was Eric Clapton, of all souls, in his autobiography.

An intense volume, it's Clapton tale of long redemption, going from a $2000 a day heroin habit, to a two-bottle a day liquor problem that he eventually found even more debilitating, as hard as that might be to imagine.

But rather than gloss over his troubled past, he vivisects it for all to see, with some of the scenes he gets into absolutely brutal to behold. It's amazing this guy is alive and sane, no less as wonderfully alive and lucid as he clearly appears to be.

It would seem obvious why Doug, a wildlife biologist and lifelong Vermont outdoorsman, wouldn't be burdened by Bambi Syndrome. But when reading Clapton's account of his life, it was interesting to note how the tortured artist came to his epiphany.

It seems that when he finally emerged from the thick woods of his various addictions, he found himself with much time on his hands, so he walked into the real woods.

With a bang.

pp. 294-295:

The tour of America took me through the autumn, and then on my return to England, I delved into a new hobby that was to equal fishing as an obsession in the years to come. My friend Phillip Walford, who is the river keeper on the stretch of the river Test that I fish, had always said that I should take up game shooting, if only for the logical reason that the shooting season starts when fishing season ends…I am a deep-end person, and in just a short time I was ordering braces of fine English guns and driving all over the country to shoot on different estates, gradually improving my skill and having the time of my life.

Clapton continues:

Ethically it was never a problem for me, and it is the same with fishing. My family and I eat what I catch and shoot. It is fresh and healthy and we love it. I am a hunter; it is in my genes, and I am quite comfortable with that. I also support a lot of other countryside pursuits, quite simply because I believe they are an important part of our culture and heritage, and need protecting, usually from people, or movements of people, who have little understanding of the delicate economic balance of countryside communities and have watched too many Disney movies.

Bambi Syndrome further explained.

Nov

8

Letter to the Editor, from Don Boudreaux

November 8, 2010 | 1 Comment

6 November 2010

6 November 2010

Editor, The New York Times

620 Eighth Avenue

New York, NY 10018

To the Editor:

You report that President Obama's export promoting trip to Asia is partly an attempt to "ease tensions with America's chief executives many of whom spent the recent campaign accusing the White House of being anti-business."

There are two ways for a government to be 'pro-business.' The first way is to avoid interfering in capitalist acts among consenting adults - that is, to keep taxes low, regulations few, and subsidies non-existent. This 'pro-business' stance promotes widespread prosperity because in reality it isn't so much pro-business as it is pro-consumer. When this way is pursued, businesses are rewarded for pleasing consumers, and ONLY for pleasing consumers.

The second, and very different, way for government to be pro-business is to bestow favors and privileges on politically connected firms. Such favors, such as tariffs and export subsidies, invariably oblige consumers to pay more - either directly in the form of higher prices, or indirectly in the form of higher taxes - for goods and services. This way of being pro-business reduces the nation's prosperity by relieving businesses of the need to satisfy consumers. When this second way is pursued, businesses are rewarded for pleasing politicians. Competition for consumers' dollars is replaced by competition for political favors.

The fact that more than 200 American business executives are in India with the President is cause to fear that any pro-business policies he might adopt will be of the second, impoverishing sort.

Sincerely,

Donald J. Boudreaux Professor of Economics George Mason UniversityNov

8

Review of Photograph 51, from Marion Dreyfus

November 8, 2010 | Leave a Comment

How many plays can you recall, offhand, that have at their center the subject of science? Michael Frayn’s “Copenhagen” is one, Stoppard’s “Arcadia” is another, and, um…

How many plays can you recall, offhand, that have at their center the subject of science? Michael Frayn’s “Copenhagen” is one, Stoppard’s “Arcadia” is another, and, um…

Exactly.

Anna Ziegler has taken advantage of the sensible idea that science is exciting, dramatic, and largely (alas) unknown in its atomistic dailiness and canine-cyclical rivalries. The Ensemble Studio Theatre offers monetary prizes for “compelling and credible” dramas involving science and technology, and if “Photograph 51” is any indication, they have a strikingly winning formula.

It is London, 1953, and separate teams of scientists are madly, often secretly, researching the “secret of life,” the strands of being we easily toss about as DNA and RNA. At the time, a British Jewish female scientist, Rosalind Franklin (amazingly convincing Kristen Bush) in concert with her by-our-standards primitive cameras, microscopes and developmental instruments and her self-possession, works doggedly and without assistance from her male cohorts to perfect an image of the helical pattern that reveals the building structure of life. Researcher Franklin used x-ray diffraction photography to minutely examine what people then called ‘the secret of life.’

Franklin’s work is of course derided and laughed at by her lab colleagues, some of whom cannot fathom that they admire her while envying her ferocious dedication. Her materials, especially her exacting crystallographic imagery, are secretly studied and handed around, as she persists with her driven examination of everything she theorizes and tries to resolve. A team of snarky researchers in a Cambridge lab removed from Franklin’s make errors and misjudgments galore, but recognize the Eureka moment weeks earlier than does Rosalind, and hasten to create the model that has made their names synonymous with the double helix. Watson & Crick, anyone?

What, however, kept Dr. Rosalind Franklin from the scientific halls of fame and glory that rightly belonged to her?

A play about the cruelties of being a female in the male-dominated world of science (which female scientist is ever married? Which ever had a child?), about the cut-throat worlds of science and succeeding. And the cost of not realizing that no matter what industry you squirrel or feint into, competition is the substrate name of the game.

The acting is uniformly superb, with a cast of (to me) unknowns. The set design, lighting, scene changes and especially the direction are first-rate. Even the diction for the majoritarian Brits, and the several American lab assistants and newly minted doctors, are pitch-perfect. Only one nitpick: One of the fellows, the American Crick, mispronounces data, as most people usually do, even today. It seems unacceptable for a scientist to do so, however. His coarseness in many matters linguistic and cultural, however, was of a piece, and contributed to the overall texture and viability of this remarkable piece of writing, which requires intense familiarity with the science of biology and genetics as well as dramaturgic niceties.

The packed SRO audience was held rapt from start to finish.

OK, so it’s science—does that mean it is dusty sere and stat-filled? Not the least. There is profound drama and emotion, taut expectation and riveting suspense. Of the past 5 or 6 dramas experienced in the past fortnight, this is far and away the very best. In fact I think it the best show I have seen this year—on or Off Broadway. Though it is a bit of a shlep to get to, the price is gentler than most shows today, and the recompense in enjoyment and full-throated literate comic, tragic and all the in-between elements are there for the inhaling.

Twist this helix as you might: A superb piece of science; a superb piece of theatre.

At the Ensemble Studio Theatre – 549 West 52nd Street, NYC Until 27 November

(For more info on this fascinating stuff: Try The New Yorker article “Photo Finish” or the PBS documentary “Secret of Photo 51?)

Nov

8

Thought of the Day, from Jim Sogi

November 8, 2010 | 2 Comments

There are some great opportunities for day trading. Recent months have had some good opportunities. It goes in cycles though. Some days are no good and it's just as well to go surfing instead. There are many edges available.

There are some great opportunities for day trading. Recent months have had some good opportunities. It goes in cycles though. Some days are no good and it's just as well to go surfing instead. There are many edges available.

People have different niches. Some systems may not make as much money, but then again some make more, and more consistently than swing trading.

Nov

7

The Search for Good Indian Food, from Pitt T. Maner III

November 7, 2010 | Leave a Comment

Many enjoy looking the search for good Indian restaurants in unexpected places across the country. A fine vindaloo and a pint of your favorite Samuel Smith's ale are hard to beat.

Many enjoy looking the search for good Indian restaurants in unexpected places across the country. A fine vindaloo and a pint of your favorite Samuel Smith's ale are hard to beat.

Here is one economist's list for whipping up a quick start Indian dish:

Buy whole spices, not ground. Get:

Cinnamon stick (not the Mexican kind) Cumin Coriander Cloves Cardamom, preferably both green and black Black peppercorns Red chilis, or red chili powder Wet ginger paste (go to an Indian grocer's), or fresh ginger, never ever ever powdered ginger Garam masala, here a good powder from an Indian mart is OK though better to make it fresh Turmeric, powder will do

For bases, draw upon:

1. Sauteed and pureed yellow onions

2. Plain yogurt, some will wish to add heavy cream as a thickener

3. Coconut milkNow start your dish. Create the chosen base. Ghee (clarified butter) can be added to #1 or #2 for yummy richness but I usually don't for health reasons. Don't mix #2 and #3.

Then take your preferred mix of spices. Fry the hard ones for two to three minutes over medium heat (3.5 on an electric stove) and puree them. Cinnamon stick should be left whole in the sauce to leach out its flavor. Never are more than three cloves needed and they can be left whole too.

Cardamoms can be inserted whole and then removed, especially if large ones are smashed open a bit with a blunt edge. Otherwise experiment with preferred combinations.

In a separate pan, quickly cook your preferred meat over high heat, just enough to make it a bit translucent or pink. Insert the partially cooked stuff into the liquid base and turn to low heat until the dish is ready.

Vegetables can be substituted for meat.

You can introduce mace and mustard seeds, or tomato can be a base in sauces.

You now have a combinatorial knowledge of many many Indian recipes and you need not memorize anything.

By the way, if you must buy powdered curry, Golden Bell is by far the best. It is packed with bay leaves and stays potent for months. You can sautee some chopped yellow onions, toss in ground lamb, douse it in Golden Bell, cook over low heat until dry, and when on the plate, over rice, coat it in plain yogurt.

Nov

7

The Kelly Criterion, from Ralph Vince

November 7, 2010 | Leave a Comment

As far as I have ever been able to ascertain, Larry Williams was the first to attempt to apply the Kelly Criterion to outright position trading, and the first to openly discuss it. His pursuit in this regard not only was my initial immersion to the ideas, but he funded those attempts. Whatever I've uncovered along the way is a product of that — Larry's unquenchable curiosity, fearlessness regarding risk, and willingness to fund pursuits others would never touch.

As far as I have ever been able to ascertain, Larry Williams was the first to attempt to apply the Kelly Criterion to outright position trading, and the first to openly discuss it. His pursuit in this regard not only was my initial immersion to the ideas, but he funded those attempts. Whatever I've uncovered along the way is a product of that — Larry's unquenchable curiosity, fearlessness regarding risk, and willingness to fund pursuits others would never touch.

A couple of points further in the post worth mentioning here because I think the other interested members deserve to have light shed on some misconceptions, some of which are a little dangerous to ascribe to, but are widely held.

"One "plays" forever, or practically forever."

But no one does and no one can, and it is this very notion of there being a finite "horizon," that changes not only the calculation of a growth optimal fraction, but every other metric related to it, giving rise to an entirely new discipline in and of itself.

"If one is somewhat risk averse, one can establish a half Kelly criterion, essentially betting half one's full Kelly bet. This results in a lower probability of one's bankroll halving."

But why "half?" Why this arbitrary number? (Or any other arbitrary dilution for that matter?) Remember, we're dealing with a function that has an optimal point, implying a curve, and it is the nature of this curve that is important to us. Being at different points on the curve has vastly different implications to us. Further, the various and important watershed points almost all are a function of that "horizon" mentioned earlier, i.e. the points migrate about this curve as a function of that horizon. Advocates of a "Half Kelly," or other arbitrary point along this chronomorphic curve (with respect to the horizon and events transpired) are seemingly unaware of the implications of their arbitrarily-chosen points.

"The criterion is to maximize the expected value of the logarithm of one's bankroll."

Yes, that is the Kelly Criterion which, in trading, does NOT result in the growth optimal fraction but a far more aggressive (and dangerous, without growth-commensurate benefit) number. No one seems to understand this.. The number returned in determining the value that satisfies the Kelly Criterion can be converted into a growth optimal number (which I call the optimal fraction. or optimal f) but in and of itself, the value that satisfies the Kelly Criterion is NOT the growth optimal fraction in trading. Incidentally, the so-called Kelly Formulas (put forth by Thorp I believe, and market applications attempted by Larry Williams in the mid-1980s) do NOT satisfy the Kelly Criterion in trading applications, but DO in gambling ones (that is, in trading applications they will not yield the same results as the value which satisfies the Kelly Criterion. The Kelly Formulas do, for dual-outcome situations, return the growth optimal fraction). For more on this I can only refer those interested to the most recent Journal of the International Federation of Technical Analysts 11 (available at admin at ifta dot org) or the 2-day course on Risk-Opportunity Analysis I am having in Tampa Nov 13 & 14 see http://ralphvince.com)

"The biggest issue of application is that one makes many assumptions about statistical distributions, correlations, returns, etc. that are all wrong."

I agree. In a strange, ironic twist to my modest participation to this story, it was (again, but some decades later) Larry Williams (rather recent) insistence of a way to apply what I know of growth maximization in a robust way. As a result of the pollenization of these ideas by Larry, I can state unequivocally that there are clear, simple, mathematical solutions to these impediments — in short, if someone wishes to apply a growth optimal approach to their future trading, these impediments ARE readily surmountable. But be certain your criterion is growth optimality, and be sure you really want to get into the cage and fight the gorilla. Most just want to sit and watch Dancing with the Stars.

Nick White comments:

Dancing with the stars….brilliant and well said.

We're all fortunate beneficiaries of Mr. Vince's investigations into the intricacies of these issues.

Phil McDonnell writes:

Kelly originally wrote his paper based on race track examples with binary outcome. You won or lost with assumed probabilities and you knew the wager size and payoff. So strictly speaking his formula only applies to wagers with two outcomes. Even a blackjack hand has at least five possible outcomes (win, lose, blackjack, double down, split) and not just two so strictly speaking Kelly's formula does not apply. Some people have erroneously tried to modify the binary Kelly formula by using average win size and average loss size to compute. All such formulas are dead wrong. The reason is that, in general, the average log does not equal the log of the average.

As Larry Williams pointed out most people do not feel comfortable using the optimum log approach even if the math is done correctly. I believe there is a simple reason for this. Most people do not have a simple logarithmic utility function. Rather they seek to maximize ln( ln w), where w is wealth. This is an iterated log function and results in a much more conservative ride. I talk about this distinction toward the end of my book. Ralph Vince also has written extensively on this subject using his term optimal f.

There is another issue with simply maximizing returns and that is it may not really take into account risk in a proper manner. It is true that the log function weights the largest loss the most in a non-linear manner and reduces the weights of gains so that the largest gains are weighted sub-linearly. But that may still not be enough to satisfy one's real risk aversion. That is part of my argument for the iterated log form but it may be that an explicit metric such as standard deviation is still needed.

Larry Williams writes:

Optimal or Maximum Wealth (possible gain) only comes with Maximum Risk; therein lies the problem. Not loosing…risk…is more important than gain in the art of speculation business.

Chris Cooper writes:

More important, as far as my practical experience goes, is that one's estimate of the edge is always subject to uncertainty. The reasons have been discussed on this list before, but certainly include changing regimes, limited history for the models, curve fitting, flexionic machinations, scaling nonlinearity, etc. I relied on the Kelly formula extensively in the mid-'70s when gambling, and uncertainty in your edge was no less important then. The problem arises because overestimating your edge is so destructive to your terminal wealth.

It might be interesting academically to consider an approach, such as Bayesian, where your estimate of the edge is not stationary, but in fact must decrease when you hit a losing streak.

James Arveson writes:

I am a newbie on this site, but I can assure y'all that any finite amounts of outcomes can easily be handled by maximizing the expected value of the logarithm of one's fortune. I have also executed these theoretical outcomes for many years in AC and LV in BJ, and yes, in Bethlehem, PA in Texas Hold 'Em. See Mathematics of Poker for a better exposition of these issues than I could ever present.

Remember that each bet is a single bet, and one can bet forever. Leo Breiman has actually proved that (in the most general cases) that this approach DOMINATES all other strategies.

Now, IMHO, this approach is irrelevant to the market. NO ONE can get all the statistical assumptions correct-statistical distribution, EV, correlation, return, s.d., etc.

Have fun until we get to the next level. Same goes for Markowitz. Check out www.styleadvisor.com. I have no piece of their puzzle but wish I did (I might be able to get a write-off ski trip to Lake Tahoe where they are located).

Actualizing all of this crap may be the next Nobel Prize in Econ, but it will probably not help schlepers make money in the markets.

Ralph Vince replies:

James,

Pursuing awards is for schlepers like Krugman or other academic dweebs –it's an award voted upon by dweebs for dweebs, and its pursuit bridles and constrains the mind (as *any* political pursuit will. Usually, the truth lies with things that - people off). To-wit, the lack of challenge to the notion that Kelly presents on p925 in the conclusion of his now-famous paper wherein he asserts that geometric growth is maximized by the gambler betting a fraction such that "at every bet he maximizes the the expected value of the logarithm of his capital."

This is accepted by the gambling community, and, by extension (falsely, mistakenly) accepted by the trading community. HOWEVER, a critical analysis of this notion reveals that it does NOT result in the growth optimal fraction, but rather in a multiplier of one's account to risk (the two are different indeed, the latter being less than or equal to the former, resulting often in over-wagering). In fact, the multiplier on one's stake equals the optimal fraction to risk only in certain, specific instances which manifest in gambling, but are rare still in trading (e.g. only on long positions, etc.). I would gladly go into this in depth put I cannot publicly do so as the paper on this has been publish in a current issue of a journal, and I have agreed to refer those interested to the article instead. The upshot is, that the Kelly Criterion, as specified above, is not what Kelly and others thought it was except in the special case I just mentioned — it is NOT the growth-optimal fraction, but something different, equal to the growth-optimal fraction only in the special case — a case that manifests in gambling with ubiquity, and oddly, in trading very rarely.