Dec

30

Correspondence With Steve Stigler, from Victor Niederhoffer

December 30, 2009 | Leave a Comment

An article with highly defective statistical reasoning appears in the WSJ purporting to show there is a tremendous turnover in the top 25 companies from 10 years ago to today. It is best to consider this by noting how many of the top 25 baseball players by batting average in 1999 are still there today. That's the best way to get a handle on the regression bias implicit in such studies. The following correspondence between Vic and Steve Stigler puts it in perspective:

An article with highly defective statistical reasoning appears in the WSJ purporting to show there is a tremendous turnover in the top 25 companies from 10 years ago to today. It is best to consider this by noting how many of the top 25 baseball players by batting average in 1999 are still there today. That's the best way to get a handle on the regression bias implicit in such studies. The following correspondence between Vic and Steve Stigler puts it in perspective:

Dear Steve,

Hope you and family well. Merry Christmas. Here's an unusal aspect of the regresson bias. Wonder to what extent this consistent with properties of random numbers and to what extent it represents a change in the level of skill or in this case price change. It would be an interesting study. I was pleased that my daughter Kira got into Columbia Engineering School on early admission and another daughter had a grandson Wilder Niederhoffer named after a Libertarian. Best, Vic

Dear Vic,

This is the same as Horace Secrist "Triumph of Mediocrity in Business" 1933, in Chapter 8 of my book Statistics on the Table.

Congrats to all your successful avoidance of and tendency towards mediocrity in your descendents!

I attach my remarks from a memorial for Rose Friedman Dec 12.

Have a happy new year! Steve

Ken Drees adds:

Market cap 10 year free market survivors: old fashioned energy (big oil), food (Walmart), and technology (human invention) lead the list and boring consumer Gillette (razor blades for everyman). Things the human race needs for survival and to thrive will always be investments that will endure.

Big government wants to bleed big oil, keep food out of banking (probably best that Walmart was denied a key to the club after all), litigate tech for the halibut. And what can be done to Gillette? Maybe the healthcare bill can attach itself to some personal care products and bleed a little off. Also, energy, food, and the stuff everyone buys is what the government tries to melt out of the inflation indexes. So what we need is what they attack and thus make more expensive to us and then they tell us that its not more expensive and to just substitute chicken for meat.

GE? what do they do other than derivatives and green initiatives which are starting to turn a little brown.

Kim Zussman replies:

From the "getting little things right but big ones wrong" department:

What were dinosaurs long at KT boundary?

Prior decade's math/science PhDs lemming into finance.

New decade definition: "lemming": The process of best/brightest young people flowing en mass to the latest promising nascent bubble.

Dec

28

Stock Monthly Return Autocorrelation, from Kim Zussman

December 28, 2009 | Leave a Comment

Using DJIA monthly returns, at the end of each December and end of decade (i.e., 12/ XXX9), checked correlation of this month's return with prior month's. Here are the correlations along with the mean return for months within each decade:

Date correl 120 av 120

12/1/1999 -0.120 0.013

12/1/1959 -0.022 0.011

12/3/1979 0.012 0.001

12/1/1949 0.019 0.003

12/1/1969 0.020 0.002

12/1/1989 0.054 0.011

11/2/2009 0.111 0.000

12/1/1939 0.119 0.001

12/1/1999 -0.120 0.013

12/1/1959 -0.022 0.011

12/3/1979 0.012 0.001

12/1/1949 0.019 0.003

12/1/1969 0.020 0.002

12/1/1989 0.054 0.011

11/2/2009 0.111 0.000

12/1/1939 0.119 0.001

Looks like returns were higher for decades with monthly correlation more negative, which is verified by regression:

Regression Analysis: av 120 versus correl 120

The regression equation is av 120 = 0.00647 - 0.0481 correl 120

Predictor Coef SE Coef T P

Constant 0.0065 0.00153 4.23 0.006

correl 120 -0.048 0.02036 -2.36 0.056

S = 0.00409714 R-Sq = 48.2% R-Sq(adj) = 39.6%

////////

Note the recent decade most resembled the one ending in 1940. In honor thereof, here is some good stuff by a former neighbor.

Jordan Low comments:

Could this be due to positive downside autocorrelation during a crisis? I am speculating…

Dec

26

Lady Gaga: 10 Things We Can Learn, from Victor Niederhoffer

December 26, 2009 | Leave a Comment

The great ascent of Lady Gaga from an also-ran performer in the Lower East Side techno-rock clubs a few years ago to number one selling recording artist in five countries, four million albums sold, and 20 million singles, rivals nothing so much as the ascent of Killmanjaro in 5½ hours or Apple's 4000% rise from 5 to 210 and the fourth largest market cap company in four years. Here are some of the things we can learn from her about how to be successful in the markets.

The great ascent of Lady Gaga from an also-ran performer in the Lower East Side techno-rock clubs a few years ago to number one selling recording artist in five countries, four million albums sold, and 20 million singles, rivals nothing so much as the ascent of Killmanjaro in 5½ hours or Apple's 4000% rise from 5 to 210 and the fourth largest market cap company in four years. Here are some of the things we can learn from her about how to be successful in the markets.

1. The Lady has a core of admirers she can always count on: the gay community. "I've got so many gay fans and they're loyal to me. They'll always stand by me and I"ll always stand by them." Apple's loyal fans are those that started out with them making music on their first computers and the minority group that liked the Apple operating system over and above the mainstream Microsoft one.

2. The prouct must be packaged and designed with great care and verve. Gaga has a special team, the Haus of Gaga, that designs all her clothes and stage performances. "When I'm writing music I'm thinking about what I'm going to wear on stage." Apple's packaging, its vivid colors, its compactness, directness, ease of use is crucial to its success.

3. You have to be technical to be a success. Gaga was playing by ear at the age of four, planning to go to Juilliard at 13. She writes her own music and her voice was good enough to attract Akon to sign her. The companies that have had the highest returns are people by engineers and computer scientistis with technical degrees.

4. You need a vision to be successful. Gaga didn't try to be the world's #1 singer or its most profitable. But she had a vision to combine glam rock with simple melodies. The best performing companies, Apple or Cisco or Whole Foods, have a product that makes life better for their customers, and they aim to be the best at it, and stick to their knitting.

5. She gets great reviews from the critics and this filters to the masses. All the best-performing companies reach out to the idea that has the world in its grip. They are all huge supporters of the current administration and reach out to unisex and redisbrituive policies so that the critics who share their persuasion will be sure to nominate them for awards. The most popular song of Gaga makes fun of rich kids that want material goods. When will she be invited to the Oval?

6. She has a simple product and a simple name. It's four letters and two syllables. And she combines simple movements, simple melodies, and simple rock rhythms in her songs. The price to weight ratio of Apple products is comparable to her own.

7. She stands on the shoulders of giants. She has borrowed from all the most popular idols that preceded her including Michael Jackson, Madonna, Blondie, and Andy Warhol. To be successful you need the base of fans that your predeceessors have accummulated.

8. She is shocking and exuberant in the things she does. The bubbles that she wore in Rolling Stone remind me of the glass houses Apple sells their products in, and her performances on stage are reminiscent of the conventions where Apple unleashes its products.

9. She has a completely integrated operation, writing her own songs, dancing them, designing her own clothes, and distributing them through a company she owns. The control of product from start to finish a la Apple's designed marketing and then retailing their own products is crucial nowadays to the most successful companies.

10. She is always ready to seek the limelight. She strives to have the best product, is proud of it, and will stop at nothing to popularize her brand. If it requires appearing nude, why that's just more publicity that her critics and core fans will love.

Kim Zussman comments:

This wonderful analysis also convincingly articulates the ugly, banal, cynical, pandering con of capitalism in general and investing in particular. Presumably the patina of beauty derives from the knowledge that it is facade.

Add to AAPL's list recruitment of the left, which targets Wintel for viruses but leaves MacAlone - encouraging climate coolers to take the path of least resistance.

Relatedly, Madam Gaga also evidences survivor-bias: How many thousands of performers try different angles but don't make it, then with the benefit of hindsight we ascribe causality to the at least partly accidental qualities of the successful?

Vince Fulco adds:

I would venture Lady Gag Gag's actions, as I like to call her, is bleeding into other artists' styles. Forced to watch Shakira's latest DVD by my significant other yesterday, it was obvious she's leaning much more risque in movements, outfits and dance routines. She certainly doesn't need to given her voice, lyrics and natural beauty. Beyonce seems to be doing the same. Although I catch these performers infrequently, who passes up an undulating set of hips that the wife gives free pass on viewing?

I would venture Lady Gag Gag's actions, as I like to call her, is bleeding into other artists' styles. Forced to watch Shakira's latest DVD by my significant other yesterday, it was obvious she's leaning much more risque in movements, outfits and dance routines. She certainly doesn't need to given her voice, lyrics and natural beauty. Beyonce seems to be doing the same. Although I catch these performers infrequently, who passes up an undulating set of hips that the wife gives free pass on viewing?

Dec

23

Whup ‘em With the Yield Curve, from Kim Zussman

December 23, 2009 | Leave a Comment

The attached chart shows weekly historical 10Y-2Y Treasury yields* (which is a measure of the yield curve slope) alongside log SP500 weekly closes, 6/76-present.

After the whip-inflation Volcker period (late 70's-early 80's), the yield curve looks like a tool to reverse recessions and bear markets in stocks. The recent peak 10Y-2Y of 2.69 is the highest since another 2.69 in 8/2003, and the prior maximum was 2.62 in 7/1992. Too little N for inference, but stocks rose for a long time after these peaks, and if nothing else it shows what the FED is trying to whip up.

*(Market yield on U.S. Treasury securities at 2-year, 10-year, constant maturity, quoted on investment basis, Fed data).

Steve Ellison comments:

I ran regressions of the yield curve, which I defined as the difference between the interest rates on the 10-year bond and the 3-month T-Bill, and the subsequent 4-month change in the S&P 500.

From 1962 to 1982, there was a strong positive correlation between the yield curve and the subsequent change in the S&P 500.

ANOVA

df SS MS F Significance F

Regression 1 0.043 0.043 6.76 0.012

Residual 61 0.387 0.006

Total 62 0.430

However, from 1983 to 2009, not only was the correlation non-significant, but the sign changed.

ANOVA

df SS MS F Significance F

Regression 1 0.004 0.004 0.54 0.463

Residual 76 0.618 0.008

Total 77 0.623

Dec

23

Imagine If, from Kim Zussman

December 23, 2009 | 1 Comment

Imagine the drift in US stocks had world wars been on US soil.

undestruction look-back bias

Dec

14

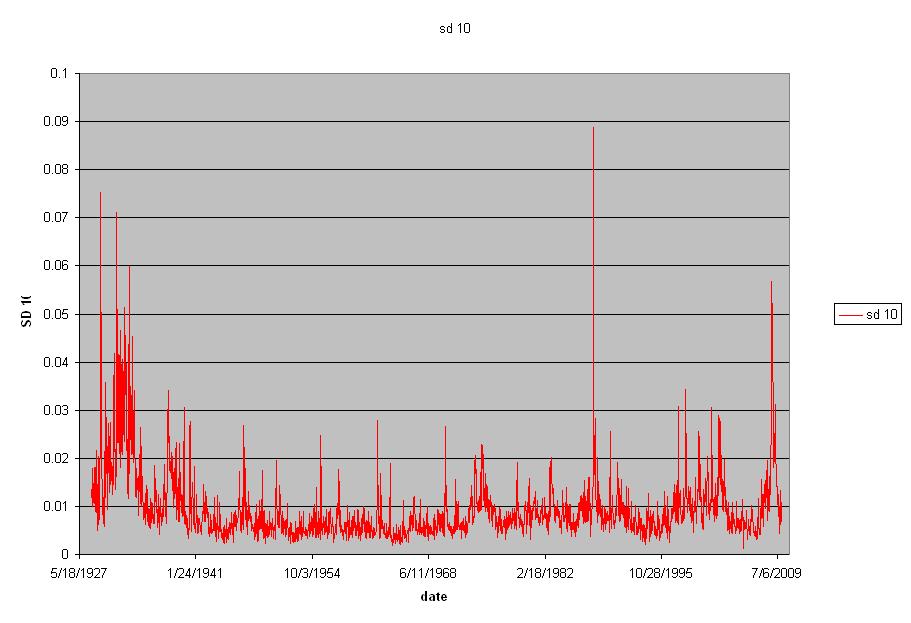

Waiting for Volo, from Kim Zussman

December 14, 2009 | 2 Comments

One definition of volatility is stdev of daily returns over a period. Using DJIA daily closes since 1929, partitioned the series into non-overlapping 10 trading-day periods. At the end of each 10D, calculated stdev of that period.

The attached graph plots 10D stdev over the whole series, with the familiar spikes corresponding to other volatility measures such as VIX and VXO. Note historically there are relatively few spikes with SD10 0.03, but when in the past they occurred (late 1920s/early 30s, late 30s, and early 2000s), there were other large spikes which followed. The notable exception is 1987, and of course the present because:

1. The future hasn't happened yet

2. The late Dr. Samuelson won the debate with the late Dr. Friedman, at least within our current Keynesian government

In attempt to quantify waits to next volatility spike after large spikes, defined a large spike as: (a maximum at the center of 17 - 10D periods) AND (>0.03). (a major spike which was the highest for 80 days in the past and 80 days in the future). The recent large volatility spike which peaked Oct 2008 was 0.057, 29 10D periods ago.

Once spikes >0.03 were identified, checked wait time until another spike >0.02 occurred. Here are the instances and the waits:

Date >0.03 nxt spike

10/17/08 0.057 ??

09/24/01 0.031 21

09/14/98 0.034 38

10/28/97 0.031 22

10/27/87 0.089 50

09/08/39 0.030 18

10/22/37 0.034 11

07/28/33 0.045 25

03/21/33 0.060 9

08/16/32 0.051 14

02/25/32 0.047 12

10/14/31 0.071 9

06/23/30 0.036 13

11/14/29 0.075 15

mean 19.8

Note the current wait of 29 10D periods is third longest, after 38 (1998) and 50 (1987).

So here we are, waiting for Godot.

Dec

14

Aristotle, from John Watson

December 14, 2009 | Leave a Comment

Aristotle once said, "All paid jobs absorb and degrade the mind" Is there any way of quantifying this, and are there any implications in the markets, life, and trade?

Aristotle once said, "All paid jobs absorb and degrade the mind" Is there any way of quantifying this, and are there any implications in the markets, life, and trade?

Aristotle also said, "We are what we repeatedly do. Excellence then, is not an act, but a habit." Does this extol the virtue of practicing until we get it right? How does one know if they are getting it right, and if they have the proper tutor.

Aristotle wrote in his Nicomachean Ethics "It is not always the same thing to be a good man and a good citizen." I've been wringing my head trying to figure out all of the different philosophers who have borrowed this idea, and have come up with a list of at least 20. Any help in compiling a complete list would be appreciated.

He also wrote in Nichomachean Ethics, "It is possible to fail in many ways…while to succeed is possible only in one way." I would like to disprove this as there are more than one path to success.

Kim Zussman replies:

Do a twin study:

Find pairs of identical twins (same genes) with different employment histories. Best would be congressman vs. doctor. Failing that, find pairs with large differences in total hours worked to date.

Perform intelligence testing on the pairs, and use paired t-test to check for difference as a function of high vs low prior work/brain wear.

A related study could be done on the productivity effects of wearing robes and fondness for little boys.

Jim Sogi writes:

At the risk of disagreeing with Aristotle, excellence is a constant struggle. At least for me it is. Habit implies some sort of easy continuation. Constant vigilance is very very difficult. Excellence also connotes superiority over others. Thus there is a the constant pushing and straining to excel over others who try even harder.

J.T. Holley replies:

I don't think Mankind or Aristotle (all thought is a mere footnote to him in Philosophy circles) should be given a break at their points in time now that we've evolved Capitalism to the point it is today. Seems to me that the most important principle here is that what was shared by Susan Niederhoffer the other day "everyday seek out knowledge". In the agrarian society that was around in Ari's time we can certainly understand that doing some "meaningless paid job" took away from the devotion, persistence, focus and the ability that Ari had at driving forward to thought and knowledge. He is reluctant to realize though that the underlying power of Capitalism and his own mind freed him up to pursue his own thoughts and not degrade his mind.

"We are what we repeatedly do."

I happen to agree with this but not in totality. His teacher Plato spoke of to paraphrase "to know the good is to be the good". Much more objective than Aristotle's "do do the good is to know the good" of which leans towards being subjective. I think both are acceptable in "being". Case in point is Plato's "Allegory of the Cave". Being tied to the post the man competed and "repeatedly" learned to beat his peers at guessing at the shadows, but once freed and outside the cave he saw the light! The objective in this allegory trumped the subjective that was thought to be the truth. The objective with the subjective seems to be balanced though if we apply Aristotle's "golden mean" that he also mentions in Nich. Ethics. A wonderful balance of both instead of just one or the other.

"Nicomachean Ethics," he said, "It is not always the same thing to be a good man and a good citizen."

Kierkegaard found and wrote of this as well. He found great power, strength, and lessons in the paradox and hypocrisies of life. His three stages of life's way is a good example of this with the movement from aesthete to ethical to final religious. In the final stage of religious for Kierkegaard he used the Paradox of Abraham to find his strength. Being told by Gawd to go to the mountain and sacrifice his son what thoughts must have been in his mind and that of his town or family? He was either a lunatic by most or the most devout believer in Gawd's word. Kierkegaard spoke of the "fear and trembling" that must've been going on as the knife was thrust to the air to the point to where it was almost at apex to come down into his young son's chest. "good man" or "good citizen"? "religious" or "crazy"? Of course as the passage goes he didn't have to ultimately sacrifice his son but the lamb. The paradox was there though when thought and decision was made to be true to himself.

He also wrote in"Nichomachean Ethics," "It is possible to fail in many ways…while to succeed is possible only in one way"

to quote the Chair "The best way to achieve victory is to master all the rules for disaster, and then concentrate on avoiding them." Trial and error is important in life and speculation. The pain from failing can often lead us to being better individuals and profit takers.

Nigel Davies writes:

I think there are a number of problems in discussing 'ancient wisdom', for example culture, language and context. One might ask what defined paid and unpaid work in Aristotle's time? I'd argue that to really understand what he was saying one would have to be a several thousand year old Greek.

I think there are a number of problems in discussing 'ancient wisdom', for example culture, language and context. One might ask what defined paid and unpaid work in Aristotle's time? I'd argue that to really understand what he was saying one would have to be a several thousand year old Greek.

As for the internalization of excellence (i.e. habits), the valuation of such may depend on whether one prefers 'reason' to 'intuition born of vast experience (ie habits)'. Taking a different angle on this, does an inexperienced but opinionated newcomer deserve to win against an old hand? Humans value their reason, but maybe this is just vanity talking.

Peter Grieve adds:

I bow to no man in my admiration for the literature of classical Attica, but Nigel has put his finger on a weakness. The surviving philosophical writers did tend to value reason over experience. This may be why they made tremendous progress in mathematics, but were dreadful scientists and mediocre engineers (Archimedes came later, and was a Syracusean). Their mathematics was largely intended to support astrology, for heavens sake. This is in line with their feeling that people who actually produced anything were of a lower order. Apparently people were amazed when Socrates spoke to artisans in an attempt to find answers. Aristotle's attitudes about paid work may reflect this bias.

Dec

12

Laffer Curve? from Kim Zussman

December 12, 2009 | 1 Comment

Here is a quick look at 2008 per-capita GDP and income taxes.

Country data on "all-in" income tax rate (income tax plus employee social security contributions):

Calculated average % tax for single (no child, two children), married single earner (no child, two children), and compared to per-capita GDP from Wikipedia/IMF, by country for major countries:

Country Tax GDP pc

Australia 21.7% 36918

Austria 32.8% 39887

Belgium 36.6% 36416

Canada 19.2% 39098

Czech Republ 15.1% 25118

Denmark 38.2% 37304

Finland 30.0% 36320

France 24.0% 34205

Germany 33.0% 35539

Greece 26.4% 30681

Hungary 38.3% 19553

Iceland 19.5% 40471

Ireland 10.0% 42110

Italy 25.6% 30631

Japan 18.3% 34116

Korea 11.2% 27692

Luxembourg 21.5% 82441

Mexico 5.1% 14534

Netherlands 32.6% 40558

New Zealand 21.2% 27083

Norway 27.9% 53738

Poland 24.6% 17537

Portugal 18.7% 22232

Slovak Republic 16.8% 22097

Spain 14.5% 30589

Sweden 26.7% 37334

Switzerland 18.3% 43196

Turkey 26.8% 13139

United Kingdom 24.8% 36358

United States 17.7% 40440

Ignoring that the Laffer Curve is supposed to be an inverted parabola, here is regression showing no relationship:

Regression Analysis: GDP versus all in tax

The regression equation is

GDP = 30035 + 18111 all in tax

Predictor Coef SE Coef T P

Constant 30035 7250 4.14 0.000

all in tax 18111 29442 0.62 0.543

S = 13134.8 R-Sq = 1.3% R-Sq(adj) = 0.0%

An exercise left to the reader would be effect of within-country change in all-in personal tax vs per-capita GDP.

Dec

11

Whither Japan? from Dan Grossman

December 11, 2009 | 4 Comments

I used to do a lot of business in Japan and I think very highly of Japanese businessmen (unfortunately they rarely include women at high levels). They have an industrious, highly intelligent population, are very interested in business, and a good base as the second largest economy in the world.

I used to do a lot of business in Japan and I think very highly of Japanese businessmen (unfortunately they rarely include women at high levels). They have an industrious, highly intelligent population, are very interested in business, and a good base as the second largest economy in the world.

It is a great mystery to me why they (and their stock market) have not done better in recent years and I have never seen any good explanation of it. Okay, they had a bubble that burst, government policies that were not great, and they have an aging population. But so what? They had plenty of opportunity to recover on their own in spite of whatever the government has been doing. (BTW their government policies could not be any worse than our current ones, so if government policies are the test, we're in big trouble.)

Has anyone seen or can anyone give a decent explanation of why Japan has lagged?

Ken Drees writes:

1. LDP party out of power after 55 years.

2. Exports and profits slumping via USA trade like others Asian exporters.

3. Big(gest) holder of USD denominated debt.

4. Aging populaton (nothing new), but 81 billion spending package just announced, more internal stimulus to follow?

5. Need to diversify their surplus holdings like others (China, Brazil, Russia, et. al.)?

6. New party administration playing a little differently with USA — recent Obama trip no real results, prior to that some grumblings about USA debt, etc.

7. Japan equities — bottoms in 1998, 2003, 2009 — skewed symetric reverse head & shoulders – or just bumping along the bottom?

8. Will need to strengthen export markets everywhere and keep USA markets open and profitable. Japan's growth lies with its neighbors if USA doesn't fix itself.

9. Yen carry trade over, yen rising — conflicts with strategic direction that exports and export profits need to be robust.

10. Zugszwang-lite Japan — any small move doesn't change game for the better. Are there any good moves available?

How will the new party lead? If they cannot rope in the yen to improve exports can they stimulate spending via QE and weaken yen at same time? Or is this approach too slow and meandering? There seems no real strong moves available unless global imbalances happen first and allow Japan countermove possibilties. Japan seems still to be unable to escape via its own power.

Is Japan getting tired of being tired?

Charles Pennington adds:

A broad-brush explanation is that the Nikkei got way out of line with other world markets and has spent the past 20 years returning to normalcy.

A broad-brush explanation is that the Nikkei got way out of line with other world markets and has spent the past 20 years returning to normalcy.

The Japanese price to earnings ratio was "well over 100" in the late 80s, and now it's 33 (reported by today's Financial Times), still higher than the US at 22. Earnings for the S&P are up about 2-3 times over their level in 1989, and perhaps the Nikkei's are as well, but if the P/E fell from, say, 200 down to more normal value of 33, a value much more in-line with other world markets, well, that explains a lot.

The Chair will rightly point out that this is retrospective, descriptive, and not predictive, that Japan's interest rates are (or at least were) lower, that the accounting may be different. Also, Mr. Grossman doubtless already knows all these figures, so he is looking for a better explanation, which I don't have.

Kim Zussman adds:

Country-stock could be like "best company" studies, showing admired firms under-performing the rest. Presumably established/successful companies/economies have less upside than currently dire situations. And more downside?

Vince Fulco replies:

To the list I would add traditional factors such as:

1. Shareholders — very far down the societal list of all stakeholders in the corporate world. The stock market is generally considered more for gambling (no jokes Dr. Z!)

2. Much heavier reliance on debt financing (too much) due to roots in maibatsu/keiretsu structure whereby a conglomerate's banking branch handles all the financing needs

3. No Carl Icahn or Guy Wyser Pratte influence to shake up entrenched mgmts and unlock under-utilized assets. The quote is 'the nail which sticks up gets pounded down'. A few have tried over the years but are usually labeled degenerates or cowboys and run out of town one way or another.

4. Years of very low ROI, white elephant projects by the government, to keep happy important constituents of the LDP (the old group in power) such as construction and the mob — i.e. the bridge to an island with 50 people on it, which we almost got in Alaska a few years back.

5. Legacy obligations which haven't been addressed but simply kicked down the road as we've emulated so well in the last 12 months.

Ken Drees responds:

Vince, Kevin, Kim and Charles have all provided excellent observations as to Japan's inbred entrenched-ness, inabilities to move, and relative over valuations. Also, the idea that is was the once high flyer status albatross, so all these past behaviors are in the rear view mirror, yet they continue to taint the view of Japan as an old has-been power country. But change agents may now be inside this yesterday/today paradigm. So far Palindrome's reflexive reinforcement of trend is still in force. The malaise continues. Will some new change agent surface? Will the reflexive reinforcement finally be breached.

Vince, Kevin, Kim and Charles have all provided excellent observations as to Japan's inbred entrenched-ness, inabilities to move, and relative over valuations. Also, the idea that is was the once high flyer status albatross, so all these past behaviors are in the rear view mirror, yet they continue to taint the view of Japan as an old has-been power country. But change agents may now be inside this yesterday/today paradigm. So far Palindrome's reflexive reinforcement of trend is still in force. The malaise continues. Will some new change agent surface? Will the reflexive reinforcement finally be breached.

The early elements for a change exist. To bet on a new bullish Japan is a long shot. But how much money can be made betting the field? Tax policy can be repealed, monopoly/hands in hands can be abolished, small investors can be made more ownership level. All the levers to lift the old dead stump and turn it over are at the ready. Or is this a dead end due to lack of will? Is Japan a stunted growth, never ever to leave off-broadway? If a global imbalance rises up, will Japan change tack and ride out on a new wind? I am watching Japan, if only since they since they are shackled to the USD. Maybe the impetus for change is at hand. This new administration in Japan — what do they owe the US?

Stefan Jovanovich replies:

The Japanese are certainly not hidebound where their Navy is concerned. They are the dominant sea power in their part of the world. From the folks at StrategyPage.com:

"Japan is currently the second largest naval power in the Pacific (after the United States), with a total of 32 destroyers, nine guided-missile destroyers, and nine frigates. The older Tachikaze-class guided-missile destroyers are being replaced by the new Atago-class destroyers. Japan also has 16 modern diesel-electric submarines. The Chinese navy is larger in terms of ships. They have 25 destroyers and 45 frigates. However, of these 25 destroyers, 16 are the much older (than Japanese equivalent) Luda class. Most of the frigates are the obsolete Jianghu class ships. China has 60 diesel-electric submarines, but most of them are elderly Romeo and Ming class boats. China's Han class SSNs (nuclear attack subs) are old and noisy. In terms of modern vessels, China is not only outnumbered, but the Japanese ships spend more time at sea and the crews are better trained. The Chinese are also at a disadvantage when it comes to naval air power. Most of China's naval fighters are old. They have a growing number of modern J-11s (a copy of the Russian Su-27) and the Su-30MKK. Japan is almost at parity in terms of numbers (187 F-15J/DJs and 140 F-2s to 400 Chinese J-11/Su-30MKKs). Japan has better trained pilots, although China is trying to close that gap as well."

Yishen Kuik adds:

The attention to detail and sense of duty of their workforce is amazing, and the public infrastructure in Tokyo is of a very high quality — certainly better than Boston, DC, New York or the Bay Area. Tokyo is much bigger than all these four areas. It makes New York seem small.

The attention to detail and sense of duty of their workforce is amazing, and the public infrastructure in Tokyo is of a very high quality — certainly better than Boston, DC, New York or the Bay Area. Tokyo is much bigger than all these four areas. It makes New York seem small.

It's not entirely clear to me why their equity markets haven't done better, but the "obvious" explanations of long term multiple contraction and shrinking internal aggregate demand seem to be correct.

I believe GDP per capita in Japan has been rising all along at the same pace as in the US since 1989, so it isn't as if quality of living in Japan has been frozen at 1989 levels. From what I can tell walking around the streets, they still enjoy a comparable standard of living to anywhere in the OECD, and have an unemployment rate (whatever that means in Japan) of 5.0%

Henrik Andersson replies:

Some investors are expressing great fear about the debt given the large amount maturing in the coming 12 months that is held by citizens, as Yishen writes, and given it has "no foreign demand, no domestic savings, structurally declining tax receipts and savings due to demographics, etc." Any views on this?

The top line numbers for the country are stagnant, but the per capita numbers don't look so bad. Japan might have a ton of public debt, but most of it is yen denominated and some 3/4 of it is held domestically by its own citizens.

Dan Grossman writes:

Two thoughts perhaps follow from the helpful comments of Prof. Pennington and Mr. Kuik:

Two thoughts perhaps follow from the helpful comments of Prof. Pennington and Mr. Kuik:

1. Based on the two-decade decline in average Japanese stock PEs from 200 to 33, why shouldn't average US stock PEs decline further from the current 22 if government policies following bursting of the bubble are equally ineffective in the US as they have been in Japan?

2. If since 1990 the U.S had avoided illegal and legal immigration anywhere near the extent to which Japan has, the US unemployment rate would probably also be 5%.

Vitaliy Katsenelson adds:

Please look at slide 14. Japanese valuations at the of 1989 were incredibly high, add to that a lengthy deleveraging process on the corporate side and leveraging (debt to GDP has tripled) on the government side and you also have anemic economic growth.

Vince Fulco writes:

Here is fascinating article in the WSJ re: a foreigner helping a small japanese village manage the downside of the demographic slowdown. One wonders how much more pervasive this sclerotic 'no change' attitude really is…

Charles Pennington adds:

There's a nice column by Lisa W. Hess in the Dec. 28 Forbes about investing in Japan.

She claims that small cap companies are even more undervalued than large cap, and recommends buying the Topix rather than the Nikkei.

Dec

9

Name That Fund! from William Weaver

December 9, 2009 | 2 Comments

Hypothetical:

Hypothetical:

You wake up this morning and have an extra $10 million dollars in your bank account. You call your banker and find out that your broker overcharged you for commissions and that the money is yours without taxes. Throughout the day you proceed to spend as much as you can; a new car… two new cars, an addition to the house that includes an indoor pool and of course gifts for your family.

You check your statement and find you still have $5 million left so you decide to invest in another hedge fund (you've managed to spend much more than $10 million in broker commissions so you've got a lot of investments). You are presented with the following list. Assuming you know nothing of the investment style or past performance of the funds, which fund would you invest in?

Intercept Capital Management

Alexander Hamilton Capital Management

Federalist Capital Management

Trafalgar Capital Management

Barkentine Capital Management

Bearing Capital Management

Royal Sovereign Capital Management

White Knight Capital Management

Rittenhouse Capital Management

VectorPoint Capital Management

Thank you so much! Any input you have is greatly appreciated.

Kim Zussman adds:

Tiger's Wood Decapitation Management

Tom Marks asks:

Is Prof. Sharpe involved with that outfit?

Dec

9

The Shadow Knows, from Kim Zussman

December 9, 2009 | Leave a Comment

Many will recall Ross Miller's study of Fidelity Magellan fund under Robert Stansky, in which he shows the fund to have been essentially indexing — without adding manager value (however you define that).

Many will recall Ross Miller's study of Fidelity Magellan fund under Robert Stansky, in which he shows the fund to have been essentially indexing — without adding manager value (however you define that).

This paper appeared circa Feb 2007; shortly after which Mr. Stansky was dismissed.

Here is a check on whether Fidelity Magellan's new manager is real or just a shadow. FMAGX daily returns (cls-cls) were regressed against big-cap SP500 index ETF, SPY. First for an equal 704 day period prior to Ross' study:

Regression Analysis: FMAGX- versus SPY-

The regression equation is

FMAGX- = - 0.000106 + 1.06 SPY-

Predictor Coef SE Coef T P

Constant -0.00011 0.00011 -1.01 0.313

SPY- 1.064 0.01640 64.88 0.000

S = 0.00278542 R-Sq = 85.7% R-Sq(adj) = 85.7%

FMAGX slightly underperformed SPY (NS), with high correlation.

Here is the same regression for the 704 days since the study:

Regression Analysis: FMAGX+ versus SPY+

The regression equation is

FMAGX+ = 0.000011 + 1.07 SPY+

Predictor Coef SE Coef T P

Constant 0.0000111 0.00023 0.05 0.961

SPY+ 1.075 0.01152 93.22 0.000

S = 0.00594187 R-Sq = 92.5% R-Sq(adj) = 92.5%

Basically identical to SPY, with same beta as before, now with even more correlation.

Eclipsing the shadow.

Alston Mabry continues:

However if one invests in 200+ large cap stocks stocks among 60 subgroups, they are going to likely going to correlate closely with the S&P 500. For example, over the past two years, an equal investment in each the nine stocks he listed would have had a 95% daily correlation with SPY.

Following a similar path, one calculates correlations for the daily log% changes of a few stocks vs SPY, over a 120-day period:

MCD by SPY: +0.36

MSFT by SPY: +0.52

PG by SPY: +0.54

Then, simply add the daily log% changes of one or more stocks together, day by day, and run the correlation against the SPY:

MCD+MSFT by SPY: +0.58

MCD+PG by SPY: +0.55

MCD+MSFT+PG by SPY: +0.67

It doesn't seem surprising that for any combination of components of SPY, one gets a higher R than any of the individual components in the combination.This is just a "back of the envelope" test, and I don't know how it would look for all possible combinations, or taking cap-weighting into account.

Phil McDonnell adds:

If one were to re-do Big Al's study it would be better to use simple percentage changes not logs. Logs are for compounding and are needed for one time period following another if reinvestment is allowed. But since step two in this process is to average the stocks into small 2 & 3 stock portfolios a simple average would be better.

In general building portfolios of positively correlated stocks will tend to move the portfolio toward the average return. However if one searches for negatively correlated investments with positive expectation returns can be achieved with less risk.

Dr. McDonnell is the author of Optimal Portfolio Modeling, Wiley, 2008

Kim Zussman writes:

MSFT is 2.4% of SP500/SPY; MCD is 0.7%

Dec

6

From the Deception Reading List, from Kim Zussman

December 6, 2009 | 1 Comment

From Against the Gods, Peter Bernstein, 1996 printing, chapter 15, paragraph 1:

From Against the Gods, Peter Bernstein, 1996 printing, chapter 15, paragraph 1:

"..quantification of risk is alive, well, and regularly practiced by professionals in today's world of globalized investing. Charles Tschampion, a managing director of the $50 billion General Motors pension fund, recently remarked, "Investment management is not art, not science, it's engineering… We are in the business of managing and engineering financial investment risk." The challenge for GM, according to Tschampion, "is to first not take more risk than we need to generate the return offered." A high degree of philosophical and mathematical sophistication lies behind Tschampion's words."

Dec

5

Buying the S&P, from Ken Drees

December 5, 2009 | 3 Comments

Buying the S&P today [2009/12/04] after the run up since March, throwing in the towel because this employment news means the economy is turning around, is akin to buying that stout, fat blood bay gelding team hitched to the most beautiful painted wagon ever seen. Arsenic fortified fiends, a la Ben Green. As soon as you buy them, they start losing weight, losing pep, losing beauty, losing power — powder on a knife, turn your back and walk away.

Buying the S&P today [2009/12/04] after the run up since March, throwing in the towel because this employment news means the economy is turning around, is akin to buying that stout, fat blood bay gelding team hitched to the most beautiful painted wagon ever seen. Arsenic fortified fiends, a la Ben Green. As soon as you buy them, they start losing weight, losing pep, losing beauty, losing power — powder on a knife, turn your back and walk away.

Kim Zussman questions:

How would you participate as a market Asperger if the market:

- Became a vehicle of change for the powers of evil

- Cheers only the flaws and mistakes of capitalism and human nature

- Makes you money only when your bets are cynical, or in the opposite direction of your beliefs

- Moves are 100% random, with an occasional bone thrown to keep you paying vig and (especially now) taxes

Dec

4

Productivity, from Jeff Watson

December 4, 2009 | 2 Comments

U.S. nonfarm worker productivity jumped at an annual rate of 8.1% in the third quarter, the biggest rise in productivity since 2003.– News Report.

I own a couple of businesses and am constantly trying to increase productivity. One benchmark for productivity is the study of Items Sold per Labor Hour (IPLH). In my mind, this is the ultimate measure, as it's non-inflationary, and cannot be massaged. I also pay attention to Items per Customer and Sales per SQ Foot. I set goals and hold the managers' feet to the fire if the IPLH suddenly dips. I don't mind paying overtime if it is used to generate extra business, and not used to finish work due to slacking. Being retail oriented, when there is downtime, the employees are expected to clean and front the inventory. We pay our employees a little over the market rate and give quarterly bonuses, yet remind them that they are only as good as their last numbers. Still, our turnover is well below the industry standards. Turnover will kill you as it costs me $1600 to train a new employee and get him up to speed.

I own a couple of businesses and am constantly trying to increase productivity. One benchmark for productivity is the study of Items Sold per Labor Hour (IPLH). In my mind, this is the ultimate measure, as it's non-inflationary, and cannot be massaged. I also pay attention to Items per Customer and Sales per SQ Foot. I set goals and hold the managers' feet to the fire if the IPLH suddenly dips. I don't mind paying overtime if it is used to generate extra business, and not used to finish work due to slacking. Being retail oriented, when there is downtime, the employees are expected to clean and front the inventory. We pay our employees a little over the market rate and give quarterly bonuses, yet remind them that they are only as good as their last numbers. Still, our turnover is well below the industry standards. Turnover will kill you as it costs me $1600 to train a new employee and get him up to speed.

Jeff Watson, surfer, speculator, poker player and art connoisseur, blogs as MasterOfTheUniverse.

Kim Zussman adds:

Possible ways to increase productivity:

Produce more with less

Produce more with the same

Produce a lot more with a little more

Produce the same with less

Produce less with a lot less

For those still employed, fear would seem to be a good motivator to work harder/more efficiently. Especially those making less than the Holy Ceiling of $250,000 per year.

Dec

2

Day of Week and Mood, from Ken Drees

December 2, 2009 | Leave a Comment

If Fridays are the best day of the week (mood wise) and traders are happy and prone to take chances, but lock in profits to be safe. And Mondays are the worst day of the week (mood wise), back to work, the grind–but some energized from the weekend all studied up and ready to go–would not Wednesday morning then be the mid point in terms of mood? Facing the long tiring day–won't be over the hump till next morning, knee deep in the work week, probably surly or strained.

If Fridays are the best day of the week (mood wise) and traders are happy and prone to take chances, but lock in profits to be safe. And Mondays are the worst day of the week (mood wise), back to work, the grind–but some energized from the weekend all studied up and ready to go–would not Wednesday morning then be the mid point in terms of mood? Facing the long tiring day–won't be over the hump till next morning, knee deep in the work week, probably surly or strained.

Tired, stressed and stuck in the middle–how to take advantage?

Victor Niederhoffer writes:

One would count.

Kim Zussman adds:

The weekly cycle in happiness appears to suggest livejournal bloggers don't like work or school. Wednesday is the maximum distance from the weekend, and happiness peaks on Saturday.

I would argue lots of adults are TGIM'ers.

Even without looking at the market, in the old days you could often tell if it's up or down by looking at spec-posts:

Permabull/permabear post ratio and tone.

Adam Robinson comments:

A lot, a lotta work has been done quantifying moods using corpus linguistics. Here's one interesting paper on time of day/day of week mood cycles.

Phil McDonnell replies:

Gallup Daily Poll has done a decent start to confirm that the phenomenon of weekly mood swings is quite real. The linked daily graph of US mood makes it quite clear that there is a weekly cycle. The next step is counting in the market as the Chair suggests.

J.P Highland writes:

My Friday attitude toward trading depends on how the previous 4 days were. If justice was found I play it safe looking not to finish in foul mood and have a sour weekend. If things went bad I become overly aggressive looking to bring my PnL back to green but usually the outcome is bad.

Victor Niederhoffer comments:

This is right out of Bacon I believe with the 8th and 9th race in those days, now the 17th and 18th on the card, being people like us trying to get even by playing the long shots.

Dec

2

An Exercise for the Reader, from Phil McDonnell

December 2, 2009 | Leave a Comment

Most say this rally started on Mar. 9th at the ominous level of 666 on the S&P. It seems to have stalled at about 1110. What number does one get when 1110 is divided by 666?

Kim Zussman writes:

It's 666 raised by 66.6%. Evidencing the Antimistress.

Nov

30

Allocation of Capital, from Dan Grossman

November 30, 2009 | 3 Comments

Allocation of capital on a macro, national scale is an important but under-studied subject, relevant to analysis of the cureent economic situation.

Allocation of capital on a macro, national scale is an important but under-studied subject, relevant to analysis of the cureent economic situation.

While the collapse of the Soviet economy seems multi-determined and very difficult to analyze, misallocation of capital (MAC) was a key, if not the key, ingredient. From the outset Soviet Communism was famous for its Five-Year Plans for investment and capital allocation. In the beginning the Plans emphasized catching up in major industrial areas where Western countries had obviously been successful — steel, machine tools, electric power — and the growth of the Soviet economy did well. There was even talk among US experts of the higher-growth-rate Soviet economy eventually surpassing that of the US.

But by the latter 20th century, US and other Western economies had become more subtle and technologically-oriented. Economic growth depended on research and fast-moving investment into high tech areas — inventions and products that initially seemed minor or almost invisible, discoverable only by haphazard groups of large corporate and tiny individual entrepreneurs, totally unpredictable to government bureaucrats.

In this environment Soviet Communism was hopelessly outclassed. Its top-down planning and traditional love of Five-Year Plans and machine tools could not keep up with Silicon Valley. Billions of dollars of Soviet capital were being allocated to projects with marginal or even negative returns, while growing billions of dollars of American capital were being allocated to the then unusually high returns of Silicon Valley and the like. Compounded over 30 or 40 years, this makes for an incredible difference in result, collapse for one and tremendous prosperity for the other.

What are the implications of this for present times?

First, we have a situation in the US where major portions of our very large economy are being shifted from allocation by entrepreneurs, who in the aggregate know where to allocate capital (not because they are so smart but because they are governed by highly diverse market forces), to allocation by Congress and government bureaucrats, who don't. (And "don't know" is charitable, since their political incentives of pork and saving failing constituencies make the government allocations even less economic.) That has to be far less favorable for long-term US economic growth.

Second, we have China. While the Chinese are probably smarter, or more uptodate, than the Soviets were in their allocations, and are dealing with an economy much more open to market forces (particularly in having to cater to US purchasing allocations), can the Chinese in their government-directed investment and capital allocations continue to escape the defects of the Soviet allocations?

And with the likelihood of the Chinese misallocations being covered up by phony statistics over many years (the same type of phony statistics that misled not only the Soviets themselves but sophisticated outside observers such as the CIA), isn't this a situation that will sometime lead to a pretty dramatic day of reckoning?

By the way, I have not read any academic or investment research on capital allocation/misallocation and the above is pretty much off the top of my head. Thus I would be grateful for good citations or sources to contradict or modify my views, or to better educate myself in this area.

Stefan Jovanovich comments:

I think Mr. Grossman exaggerates the extent to which American "capital" has been allocated by entrepreneurs in the years since 1925. Wealth has certainly been created by enterprising individuals; but the extent to which the national wealth has been allocated by the government should not be ignored. One statistic always comes to mind when I read praise for American "capitalism" — the amount of money spent on the Manhattan Project alone was more than the entire historical investment in the U.S. auto industry. Silicon Valley — which looks a good deal like Detroit in the mid-1930s these days — was very much the product of the military-industrial complex Eisenhower questioned. Mr. Hewlett and Mr. Packard got their start by selling oscilloscopes to the Army, and but for the need for control devices for ICBMs, they would still be growing fruit in the orchards around San Jose.

What defeated Soviet communism was the absence of private money, the inability of individuals to save their own wealth in a form that could be spent by them. Everything in the Soviet Union was rationed; it was the ultimate single payer system. The question for which none of us has an answer is will private money continue to exist in China when that country has its banking and credit crisis? (Of course, the cynics I know are asking the same question about the present banking system in the United States: "What do you think of the American system of private money, Mr. Gandhi?" "A most excellent idea.")

P.S. For the first 60 years the Soviets' allocation of capital was not greatly inferior to our own where military technology was concerned. Their ability to literally move their entire industrial base 500 to 1000 miles east while defending themselves against the Wehrmacht is a miracle of raw production that more than equals anything done by Kaiser's shipyards and Boeing's B-29 factories in Kansas. Imagine the German Army invading the United States through the Champlain valley and capturing Boston, Pittsburgh, Cleveland, Philadelphia and New York and the United States' moving its entire steel and auto industries by rail to Nebraska in the midst of winter.

P.P.S. The B-29 was built in Kansas because of the assumption that the United States might be subject to the same kind of sustained bomber offensive that the Allies had been conducting against Germany. The failure of the Germans to develop the significant heavy lift capacity for bombing and transport is probably the single top down command decision that doomed them; if they had invested the effort into development of a 4-engine bomber that they put into rocketry, they would have won. Instead, the Allies did, which allowed them to discover after the fact — thank you, Professor Galbraith — that bombing was a complete failure.

Kim Zussman replies:

One could make the case that the tech bubble was partially the result of the collapse of USSR:

- The political stability risk-premium in the US went down post-Soviet threat (markets move in reverse to risk premium change)

- Defense spending went from 6% to 4% of GDP from 1990-2000 (see attached chart from this site). Some of that went toward tech investment (Note that defense spending went up post 911, and stocks/ROC 00-10 was not as good as 90-00).

- Check out what happened to Japan and Germany stocks post-defeat, and St. Petersburg post-Bolshevik.

Nov

23

Speaking of Value Line, from Kim Zussman

November 23, 2009 | Leave a Comment

Here is a description of the studies I am doing on Value Line. FVL is an ETF which uses the Value Line timeliness system. Instead of using VL service to pick stocks individually, you can own FVL and obtain VL returns (of course other screens could be applied).

Using daily closes of FVL and SP500 ETF SPY, I did a linear regression:

For each day's change in SPY (X), what is the same day's change in FVL (Y). The actual equation for this line is:

FVL = - 0.000109 + 0.791 SPY (Y = alpha + beta*X)

The regression does a least-squares fit of a line to the data (minimizing the sum of squares of errors in Y direction), and the slope and Y-intercept of this line describes how FVL's daily change is related to SPY's.

The slope ("beta") of 0.8 means that when SPY goes up 1%, on average FVL went up 0.8%, etc. The intercept alpha) shows, on average, whether FVL gives higher or lower daily return than SPY, by checking where the line crosses when SPY is zero.

Both slope and intercept are tested for statistical significance (assuming error residuals are normally distributed), that is whether they were likely to have occurred by chance alone.

(Better descriptions welcomed)

Here is the study:

FVL; Value Line timeliness ETF.

From inception in 2003, regressed daily return of FVL vs SPY:

Regression Analysis: FVL versus SPY

The regression equation is

FVL = - 0.000109 + 0.791 SPY

Predictor Coef SE Coef T P

Constant -0.00011 0.00023 -0.48 0.630

SPY 0.79111 0.01640 48.24 0.000

S = 0.00906282 R-Sq = 59.3% R-Sq(adj) = 59.2%

>> Conclusion: alpha (with respect to SPY) for FVL is negative, though N.S. Beta is 0.8, and highly significant.

A scatter diagram is also available.

Charles Pennington writes:

For my curiosity, could you (if convenient) try reversing it and regressing SPY vs the VL fund, for comparison?

Kim Zussman replies:

No problem, Charles. Here's what happens when you reverse the independent and dependent:

Regression Analysis: SPY versus FVL

The regression equation is

SPY = 0.000173 + 0.749 FVL

Predictor Coef SE Coef T P

Constant 0.0001734 0.0002204 0.79 0.432

FVL 0.74920 0.01553 48.24 0.000

S = 0.00881953 R-Sq = 59.3% R-Sq(adj) = 59.2%

Analysis of Variance

Source DF SS MS F P

Regression 1 0.18099 0.18099 2326.84 0.000

Residual Error 1599 0.12438 0.00008

Total 1600 0.30537

Nov

22

Deception, from Victor Niederhoffer

November 22, 2009 | Leave a Comment

The best books on deception are the best books about the market. The best book about the market according to Martin Shubik is Ben Green's Horse Trading. I would add that there is a good section on deception in EdSpec. And I would point out that a systematic categorization of deception is essential and this is available in the ecology literature following J.R. Krebs's citations on deception in various species, especially monkeys.

The best books on deception are the best books about the market. The best book about the market according to Martin Shubik is Ben Green's Horse Trading. I would add that there is a good section on deception in EdSpec. And I would point out that a systematic categorization of deception is essential and this is available in the ecology literature following J.R. Krebs's citations on deception in various species, especially monkeys.

Adam Robinson says:

Of course, as I've eulogized no end, The Farming Game by Bryan Jones also has much to say on deception in the buying and selling of livestock, and does so with wit and insight.

Alston Mabry recommends:

I like A Treasury of Deception: Liars, Misleaders, Hoodwinkers, and the Extraordinary True Stories of History's Greatest Hoaxes, Fakes and Frauds by Michael Farquhar.

Russ Herrold re: The Farming Game:

I purchased The Farming Game on your recommendation and enjoyed it. It was a bit dated as to price examples (they look like a series from the mid 1960s to the mid 1970s), but the underlying principles remain sound. The book starts a bit slowly, setting up some stereotype character sketches, and then strings them together a bit, a bit later in the book.

Kim Zussman writes:

Here is my Deception reading list:

Stocks for the Long Run, Siegel

Irrational Exuberance, Shiller

A Random Walk Down Wall St., Malkiel (efficient markets)

Beating the Street, Lynch (inefficient markets)

Trade Like a Hedge Fund: 20 Successful Uncorrelated Strategies & Techniques to Winning Profits, Altucher

The Intelligent Investor, Benjamin Graham (value)

Common Stocks and Uncommon Profits and Other Writings, Fisher (growth)

Futures: Fundamental Analysis, Schwager

Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications, Murphy

Contrarian Investment Strategies - The Next Generation, Dreyman

Trend Following: How Great Traders Make Millions in Up or Down Markets, Covel

Momentum Stock Selection: Using The Momentum Method For Maximum Profits, Bernstein

(eigenvector = deception)

Vince Fulco adds:

To Dr. Zussman's excellent list, I would add another one very much off the radar screen. In Hostile Territory by Gerald Westerby is purported to be written by a former Mossad agent and profiles his adventures in Africa, the ME and Europe. I consider it of the best books written on the manipulation of human perceptions, mental flaws and frailties. I try to read it once a year to condition myself to avoid the traps. It is right up there with Cialdini, but the dynamic and life threatening challenges faced by the author are much more entertaining while providing extraordinary lessons on the subtleties of behavior.

I found the walk through on structuring a diversified [here: agri-]business very approachable, and anticipate lending it out to give context for further discussions to some I work with and mentor.

Jeff Watson comments:

The best book I ever read on deception was called The Game by Neil Strauss. This book is the holy grail for pickup artists, but the lessons easily translate into all areas of life from sports to trading to games. It was very entertaining and well written, znd Strauss gives point by point instructions on how to manipulate, deceive, obfuscate, hypnotize, and control your opponent or object of desire. Strauss takes time to delve into the science of how to pick up women, and believes in rigorous testing and the book surprisingly isn't as misogynistic as one would expect.

The best book I ever read on deception was called The Game by Neil Strauss. This book is the holy grail for pickup artists, but the lessons easily translate into all areas of life from sports to trading to games. It was very entertaining and well written, znd Strauss gives point by point instructions on how to manipulate, deceive, obfuscate, hypnotize, and control your opponent or object of desire. Strauss takes time to delve into the science of how to pick up women, and believes in rigorous testing and the book surprisingly isn't as misogynistic as one would expect.

Bruno Ombreux writes:

One absolute classic is Arthur Schopenhauer's The Art of Controversy. It also goes by a different title: "The Art of Being Right". Here is a Wikipedia article with the full list of stratagems. And it is available for free at Gutenberg.

Kim Zussman writes:

The most respected investment books of the 20th century all have eigenproblem of hidden utility. Even when authors are intellectually honest, it's hard to understand how they could escape distortion induced by rewards.

Some are selling their strategy (read my book but invest with me), talking their book (I'm deep into growth or value, so please buy these), pandering the academy (status as published professor), making a career of teaching how to trade, increasing status, creating a legacy, etc. This is similar to the more general, "how many friends do you have who don't profit from you?"

Bruno Ombreux responds:

I haven't read all the books in Dr. Zussman's list, but among those I've read, I think two are not deceptions:

A Random Walk Down Wall St., Malkiel (efficient markets)

Most investors would be better off reading this book and stopping there. Also:

The Intelligent Investor, Benjamin Graham (value)

I haven't finished this book because after the first two chapters I realized it was just a watered down version of the first edition of Security Analysis, from the same author + Dodd.

Security Analysis is an excellent book that makes excellent points for the era it was written in. Their technique of looking into detail at companies accounts is similar to detective work, which itself is an application of the scientific method. In my opinion, this kind of financial analysis is a valid way to proceed.

Nigel Davies comments:

The nature of deception may be much deeper than many authors make out. I would say that the origin of all deception is in fact self-deception and that the supposed 'deceiver' is doing nothing more than moving into the vacant space within our understanding.

George Parkanyi writes:

There is a saying. "Fool me once, shame on you. Fool me twice, shame on me." To me it's just a given that traders, particularly those trading in size, use techniques to mask their intentions. And sure, those that have knowledge of them, run stops. That's just one of many influences that make financial instruments wiggle on a day-to-day basis, and you would not only have to sort out what is "deceptive" behaviour vs stupid vs herd behaviour, but whether the deception was or was not in your favour. Unless you have a large network of people you can call on the inside that can give you information that helps you take the temperature of a given market, I don't see the point of trying to personify this market move or that market move as "deception", especially in a big liquid market that is essentially a non-linear system subject to multiple influences. If there's a pattern that you detect and can exploit then so be it. But does it matter if it is "deception" vs. sentiment or just a big whale moving through?

There is a saying. "Fool me once, shame on you. Fool me twice, shame on me." To me it's just a given that traders, particularly those trading in size, use techniques to mask their intentions. And sure, those that have knowledge of them, run stops. That's just one of many influences that make financial instruments wiggle on a day-to-day basis, and you would not only have to sort out what is "deceptive" behaviour vs stupid vs herd behaviour, but whether the deception was or was not in your favour. Unless you have a large network of people you can call on the inside that can give you information that helps you take the temperature of a given market, I don't see the point of trying to personify this market move or that market move as "deception", especially in a big liquid market that is essentially a non-linear system subject to multiple influences. If there's a pattern that you detect and can exploit then so be it. But does it matter if it is "deception" vs. sentiment or just a big whale moving through?

Don't get me wrong. Reading about deception is certainly interesting. As a Scout leader, Arthur Baden-Powell's role in the Battle of Mafeking during the Boer War is an excellent example. In fact, BP's entire early career was based on deception. But I personally don't see the value in getting overly concerned about deception in the markets, though I understand that others do.

I think if you have a general sense of the day-to-day character of a market that you have researched and trade regularly, and do some research to try to anticipate macro influences on that market that might cause it to trend, the rest can be handled with money management.

Stefan Jovanovich replies:

Baden Powell's energy as a commander was probably the decisive factor in having the deception succeed:

From British Battles:

Baden-Powell conducted the defence of the town with great energy and resource, leading the Boers to believe there was a larger garrison than was the case. In November 1899 Baden-Powell launched a series of raids on the Boers lines that caused him some casualties but made the Boers wary of the garrison.

Initially the Mafeking garrison had no artillery. Baden-Powell improvised various items to look like real guns and trains, while engineers manufactured a gun, known as the "Wolf", from a length of steel pipe. The Boers used the 2 two inch guns they had captured from Dr Jamieson to bombard the town. Dud shells fired from these guns were reworked and discharged at the Boer lines from the Wolf. An officer found an old muzzle loading naval gun serving as a gate post. This gun was christened "Lord Nelson" and drafted into service. Dynamite grenades were manufactured and thrown at the Boer lines and a small railway line was built across the town.

In sharp contrast to the indolent Ladysmith garrison, Baden-Powell kept his men constantly on the move, raiding the Boer lines and keeping the besiegers on their toes.

Scott Brooks adds:

Atlas Shrugged not only speaks of deception, but the deceivers are open about their deception. The deceivers/looters are like gangsters who are in complete control in kick sand in the faces of the producers, daring them to say A is A and damning them if they do, all the while fooling the masses with their A is B pablum. The parallels to our world today are stunning.

Nov

21

Retire With $1 Million in S&P500, from Kim Zussman

November 21, 2009 | 6 Comments

A once popular eigenshibboleth is the need for stocks to finance retirement. There are lots of graphs of historical compounding of the SP500 over various periods, but I was curious about account balances over periods of retirement consumption. This is a simple (* see note) study of hypothetical $1M retirement accounts invested in the SP500, for 5 different individuals each retiring at the beginning of a decade: 1950, 1960, 1970, 1980, and 1990.

For everyone (except Goldman Sachs employees), they say one needs about 80% of their pre-retirement income to retire comfortably. $8,000 per month is 80% of $120,000 annual income (average government employee). Each of the 5 retirees puts $1M into the SP500 at the beginning of his retirement (his because a woman's work is never done), and each month sells stock and draws out $8,000 - leaving the balance in stocks. The balance of each retirement portfolio varies due to monthly drawdown + stock exposure, and the running account-balances are graphed in the attachment to compare balance variability and time to depletion for the different periods.

1950 did very well, with his account varying about $1.5M from 1955-69, and he didn't run out of money until 1989. Men didn't live so long then, so his widow must have been smart. The money lasted 39 years.

1960 wasn't so lucky: his account dropped rapidly in value, and was gone by 1974. Hopefully his wife was a professor too, and for the rest of their days they read books from the library together. Money lasted 14 years.

1970 unfortunately had to go back to work after 10 years, when his $1M was gone. Fortunately he got a job as a photographer for Playboy.

1980 made Einstein look like a Troglodyte. His account is still nearly $1M in 2009, and at times approached $3M. 1980 is a widower, and is friends with 1970, who set him up and he is now happily wed to a centerfold. Has been spending for 29 years and no end in sight.

1990 got off to a great start, but the last decade put him into Cymbalta, Cialis, and Metamucil. His account, which was worth $1.6M in 2000, is worth only $280,000 now, and he is calling the Senate today to make sure his meds will be free. 19+years and looking precarious; money may be gone in 3 years.

Note: *(study is very simple: inflation not factored, ignore effects of taxes, SP without dividends, earlier periods hard to index, no one has 100% in stocks, etc).

Anton Johnson comments:

An excellent study that demonstrates the perils of excessive withdrawal rates and underfunded retirement savings.

If we account for dividends and inflation which are not trivial, add government retirement benefits, and the modeled retiree varies withdrawal rates to the widely recommended annual 4-5% of gross account value, certainly a rosier picture emerges.

Kim Zussman adds:

There are many ways the retardees [Ed.: spelling?] could or should have allocated/withdrawn, but here I was trying to elucidate the effect of luck: when you retire vs the market then. The graphs are reverse of often shown compounding up to retirement — adding X per month to stock account (Famous example Mr. Hill, the engineer who used Value Line to compound millions).

One notes the effect here of changing cycles: 1977-00 worked for all stocks, not just growth. And since then, well, it's been more difficult. Even difficult for Value Line:

"November 10th, 2009

Last week the SEC charged Value Line Inc., an affiliated broker-dealer Value Line Securities (VLS), and two of Value Line’s senior officers with defrauding the firm’s family of mutual funds. Value Line’s CEO Jean Buttner and its former Chief Compliance Officer David Henigson have both settled the charged by consenting to the entry of a cease-and-desist order, though they have neither admitted to nor denied the SEC’s charges.

The Commission found that Value Line had been redirecting portions of the funds’ securities trades to VLS from 1986 until 2004 and that Buttner and Henigson overall received “over $24 million in bogus brokerage commissions from the funds pursuant to this scheme, as VLS did not perform any bona fide brokerage services for the funds on these trades.”

According to the SEC’s press release, Value Line, Buttner and Henigson further misrepresented VLS’s “phantom brokerage services” to Value Line’s shareholders, the Independent Directors/Trustees, and the SEC."

What if you invest in something other than the stock market? In the interest of ethnic diversity, attached is chart of $1M retirement accounts, each drawing $8000 per month, and compounding 1, 2,3,4,5% interest monthly on the remaining balances. I left off the current 0% interest environment, as an exercise for the reader.

Alston Mabry replies:

That's funny, because one of the authors of one of the investment books you listed previously, recently penned a journalistic piece about how maybe it didn't make sense to go to college, because if you put the college money instead into a savings account earning "just 5%", then you would get a better lifetime return.

The whereabouts of this magical savings account was not given.

Jason Ruspini writes in:

The effects of demographics on the underlying returns can't be too auspicious for more recent vintages. The parallel the Sage drew between 1954 and today seems very shaky in that respect.

Nov

18

Brooke Is Superficial, She Talks Only About Things, by Kim Zussman

November 18, 2009 | 4 Comments

Brooke [Shields] is superficial, she talks only about things rather than ideas. — Attributed to Andre Agassi.

Supposedly Brooke graduated Magna from Yale, so she must be a well-reasoned thingophile. I called my college daughter this morning, hoping to give fatherly advice on "how not to be superficial." A simple formula: in speech, increase the ratio (ideas)/(things).

Supposedly Brooke graduated Magna from Yale, so she must be a well-reasoned thingophile. I called my college daughter this morning, hoping to give fatherly advice on "how not to be superficial." A simple formula: in speech, increase the ratio (ideas)/(things).

This advice rapidly became convoluted. An idea fundamentally is a thing. Structurally — an arrangement of specific neuronal connections. Money certainly is a thing, but also an idea; an idea which can transmit ideas (e.g. paying a consultant for ideas). A vehicle to facilitate trading of things, often glorified, and vilified, by people with conflicting ideas about the value of things.

Breast implants are things, with an idea behind them (a new tee-shirt logo?). Make-up is a thing — to present an illusory idea; allure, of youth and seduction, and escape from the idea of time, aging, and death.

Brooke may have had ideas about using her things to get things — a very common idea.

The advice was unnecessary as my daughter isn't superficial. But still it's interesting that smart, beautiful women, who never do things by accident, use the idea of things to get things.

Nov

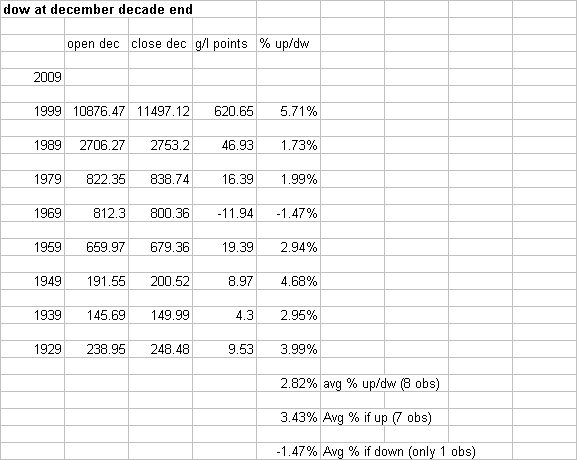

16

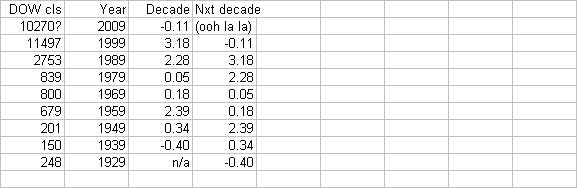

Dow in December XXX9, from Ken Drees

November 16, 2009 | Leave a Comment

Speaking of decades, if you had to pick one asset to buy for the decade and you had to just hold it, what would that be? For example, these would have been great decade-long holds without trading:

1999—buy gold

1989—buy tech stocks

1979—buy US stocks

My long pull ideas for 2010- 2019:

biotech — (buy a biotech mutual fund and forget it)

tech (robotics, space, warfare)

China (no brainer)

US real estate — (it should recover by 2019, eh?)

commodities — (feed China)

Kim Zussman looks at it differently:

Counting years ending in 9 as end-of decade, if DOW closes near where it is now — this will be the first down decade since the one ending in 1939. Here are decade returns and alongside the subsequent decade:

Not related to day-trading, but long (10+yr) period movements of the stock market could affect contemporaneous investors' future outlooks. E.g., those in stocks 1990-2000 experienced something very different from the recent (down?) decade.

Nov

14

Charting A Previous Era, from Kim Zussman

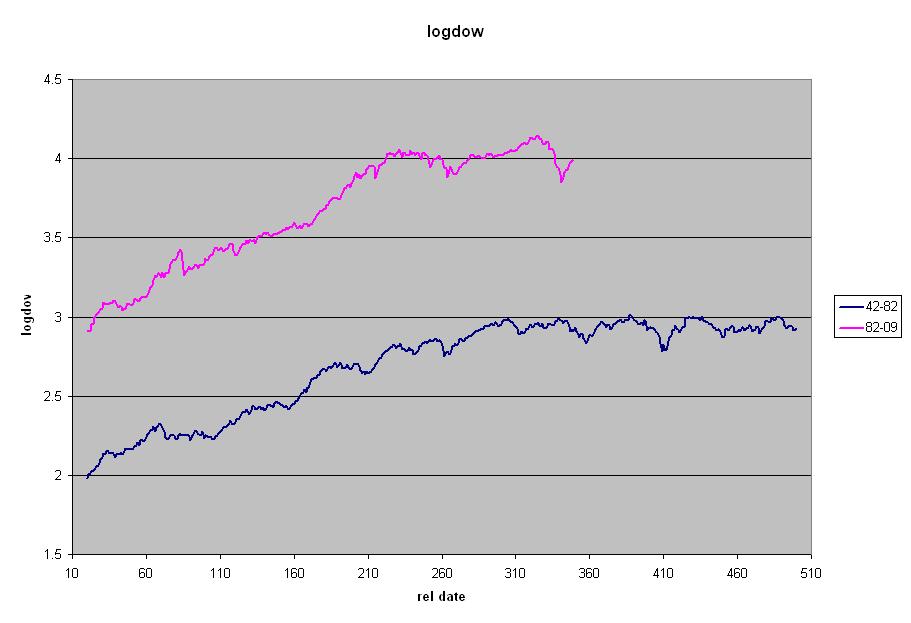

November 14, 2009 | Leave a Comment

The attached chart compares log(DJIA monthly close) for the periods 1942-1982 and 1982-2009, transposed such that 1942 and 1982 start at the same point in time. "Relative date" axis is in months at the same scale for both periods. The "range-bound" period (and what a range it was) in the older series starts in 1965 and ends in 1982. Why did it end ? Presumably de-torporization via larger than life Paul Volcker, Ronald Reagan, Bill Gates, and Michael Milken.

Why 1942? It was a good starting point, as it was when Bogart made Casablanca. The era 1942-1982 could be called the era before financial engineering ("I am shocked to learn that there is gambling going on here, gambling on the value of mortgage backed securities").

Nov

11

How Now, Mighty Dow? , by Kim Zussman

November 11, 2009 | 1 Comment

Dividing DOW weekly closes into non-overlapping 25 week segments, I checked for large advances similar to now using:

{max close (recent 25W)} / {min close (prior 25W)}

Currently this quantity - the move to the high weekly close of the 25 weeks ending last week, compared to the low weekly close of the prior 25 weeks - is 0.51 (+51%). I checked back to 1929; there has not been a gain over 50% since 1983, then 1974, and in the 1930's (see attached).

Looking only at periods with gains >40%, here are the returns over the subsequent 25 weeks:

Date 25 max/min nxt 25W

02/19/34 0.960 -0.142

08/28/33 0.957 0.024

02/27/33 0.793 0.925

06/27/83 0.584 0.021

12/05/38 0.529 -0.072

10/27/75 0.512 0.197

01/20/36 0.498 0.116

05/05/75 0.454 -0.017

10/19/87 0.446 0.032

03/29/43 0.441 0.033

07/29/35 0.439 0.173

05/12/86 0.418 0.072

10/21/29 0.403 -0.024

. avg 0.103

Anton Johnson comments:

A quick look at all non-overlapping 25-week periods for weekly Dow 1929-Current yields a mean return of 2.73%; using this as the baseline results in a 7.56% excess return for the R>40% periods (10.29-2.73 = 7.56). However the 92.5% return in 1933 significantly skews the small R>40% sample. Median returns are 3.57% and 3.20% respectively, not much different from each other.

Oct

24

Political Science, from Kim Zussman