|

Daily Speculations

The

Web Site of Victor Niederhoffer and Laurel Kenner

Dedicated to the scientific method, free markets, ballyhoo deflation, value creation, and laughter.

A forum for us to use our meager abilities to make the world of specinvestments a better

place

|

|

Home

Write to us at:  (address

is not clickable)

(address

is not clickable)

The Chairman

Victor Niederhoffer

THE JOURNAL

OF LAW AND ECONOMICS Vol XI, April 1968, pp35-53

PREDICTIVE AND

STATISTICAL PROPERTIES

OF INSIDER TRADING*

JAMES H. LORIE

AND VICTOR NIEDERHOFFER

University

of Chicago

INTRODUCTION

”INSIDERS” are officers, directors, and owners

of ten per cent or more of the common stock of the companies listed on the New

York and American Stock Exchanges. The Securities and Exchange Commission (the

SEC) requires that insiders keep the Commission informed regarding transactions

in the common stock and convertible securities of the respective companies. The

interest of the SEC in trading by insiders stems in part from the belief that

insiders should not exploit their special opportunities to know about

developments in their companies for personal profit through short-term trading.

Further, the Commission feels that information on trading by insiders should be

fully disclosed to the investing public because of light which such trading

might cast upon the company’s future prospects.

There is also wide-spread interest in the

investment community in trading by insiders because of the prevalent belief that

insiders have valuable private information which bears upon their company’s

prospects and that knowledge of the trading by insiders will permit valid

inferences regarding future movements in the prices of stocks. Because of the

interest by the SEC and the investment community in insider trading, we have

undertaken this study. The subject has been studied before in many ways, but

none of the preceding studies has been definitive and the additional methods of

analysis seemed promising. Opinions are somewhat polarized. Academic studies

have found virtually no evidence of profitable exploitation by insiders of their

special knowledge and no value to outsiders in data on trading by insiders.

Others believe that insiders often make extraordinary profits and that knowledge

of their trading is valuable. Both the SEC and investors should be interested in

which opinion is correct. The methods and coverage of this study differ from

those of earlier work, as do our conclusions. We show that proper and prompt

analysis of data on insider trading can be profitable, although almost all

earlier academic work has reached the contrary conclusion. The first section of

this report comments on some methodological problems; the second deals with the

statistical properties of insider trading; the third, with various promising

kinds of analyses; the fourth summarizes our findings.

SECTION 1.

SOME METHODOLOGICAL PROBLEMS AND COMMENTS

Studies of insider trading are based on data

published by the SEC for all listed companies in its Official Summary of

Stock Transactions.[1] The Summary is a complete record of transactions of at

least 100 shares in the stock of their own companies (or convertible securities)

by the directors, officers, and owners of ten per cent or more of the

outstanding shares. The Summary is compiled from month-end reports of insiders

and is in print approximately five weeks after the last transaction. The basic

data, however, are frequently filed by the insiders with the stock exchanges

within a few day of the transaction. Regulations require that information be

filed with the exchanges within ten days of the end of the month in which the

trading takes place.

A methodological problem arises from

imprecision in specifying the date of transactions. During 1951-1962, the

Summary gives only the month rather than the actual date of individual

transactions. The possible error caused by this imprecision can be substantial,

for the average variation from month to month in the price of a stock is

approximately 6 per cent. Furthermore, the closing price for the month is an

average of 5 per cent greater than the lowest daily closing price and 5 per cent

less than the highest daily closing price. Unfortunately, most of the empirical

studies have used data from this period with a loss in precision and a

consequent tendency to create the impression that insiders made less money on

their transactions than they actually did. In the absence of an exact date of

purchase or sale, the investigator has assumed that the transactions were made

at the average price for the month, at the price prevailing at the middle of the

month, or at the price at the end of the month. But the price on the day the

insider actually made his transaction has consistently been more favorable to

him than the price on the aforementioned dates. This fact emerges clearly from a

study reported in Section 3-A. All occasions were noted on which three or more

insiders (net) bought stock during a month. The price on the date of the last

insider transaction during the month was compared with the price six trading

days after the end of the month.[2] On 32 of 36 occasions, the price on the

sixth trading day after the end of the month was higher than the price actually

paid. But on only 19 of the 46 occasions on which three or more insiders sold

was the price higher on the sixth trading day after the end of the month. A

difference at least as great as this would occur fewer than one in ten thousand

occasions if insiders did not consistently execute trades at more favorable

prices than the price on the sixth trading day after the end of the month.

There are a number of other difficulties in

interpreting data on trading by insiders. Transactions of members of the family

of the insider do not have to be reported. It would be possible for insiders to

tell their families to act in anticipation of some unusually favorable or

unfavorable event, thereby evading detection. Manne emphasizes another

profitable arrangement whereby insiders of different companies exchange valuable

information about their respective companies.[3] Since insiders are required to

report transactions only in their own companies, we would have difficulty in

detecting these activities.

Further, the Summary is bulky and difficult to

analyze. The Summary of the 1930’s came in three sections, and frequently was

over 70 pages long. ‘There have been occasions on which the transactions of

insiders were reported two or more years after the actual transaction. Another

obstacle to refined analysis has been locating price and dividend information to

match the dates of insider transactions. As a result of these difficulties,

those who have insisted on accurate observation have been forced to limit

severely the number of companies and years subjected to study.

A majority of scholars considering the

profitability and utility of data on insider trading have reached negative

conclusions. For example, Smith, in summarizing his frequently-quoted monograph,

states: “Furthermore, the several tests suggest, without definitely answering

the question, that the performance of insiders of large companies may have been

definitely inferior to that for the aggregate of listed companies.”[4] And Wu

notes “there is very little evidence that a definite relationship exists between

insider transactions and subsequent price movements,” and concludes “from these

cross- section data, there is no sufficient evidence to prove that insiders in

these 50 companies as a group had outperformed the market.”[5]

This view, however, is opposed to a belief

common in Wall Street. Shaw observes that “logic does indicate that corporate

officers and directors know more about the future of their own companies than

other observers, and this logic has been clearly enough demonstrated in practice

to make the study of insider

transactions a useful tool for other investors.”[6] Harriet West concludes in

the Encyclopedia of Stock Market Techniques that when officials of a

company are buying their own stock on a decline, an outsider can safely assume

that the outlook is as good or better than when he first purchased his stock.[7]

The major newspapers publish summarized reports

of the large transactions of insiders so that their readers can gain indications

of possible price movements. Finally, the Insider Report, The Indicator Digest,

Drew Associates, Value Line Investment Survey, Stanford Investment Management,

Inc., and the Consensus of Insiders base their advice in part on the

transactions of insiders.

This paper contains information which tends to

corroborate the view of the stock market

advisers. We have noted (Section 3-A) for example, that insiders have superior

ability to “predict” large price changes in their stock. In Section 3-B, we

demonstrate that intensive insider buying in a month typically signals

performance which is favorable relative to the market in the next six months and

conversely for intensive selling. Section 3-C, on the other hand, provides an

example of a commonly held belief about insider trading that is not confirmed by

our investigation. We test the contention that there are companies in which

insiders are consistently successful and find little support for it.

SECTION 2.

STATISTICAL PROPERTIES OF INSIDER TRADING

In order to provide a framework for these

studies, we devote this section to an analysis of some statistical properties of

data on insider trading. Other investigators may find this section useful. The

data we analyze here are insider trades from January, 1950 to December, 1960 of

a stratified random sample of 105 New York Stock Exchange companies. The major

kinds of information reported in the Summary are month and year of transaction,

the relationship of transactor (Director, Officer, etc.), nature of ownership

(Direct, Indirect, etc.), size of purchase, and month-end holding.

We record simply as an example one of the most

famous set of trades by insiders, the

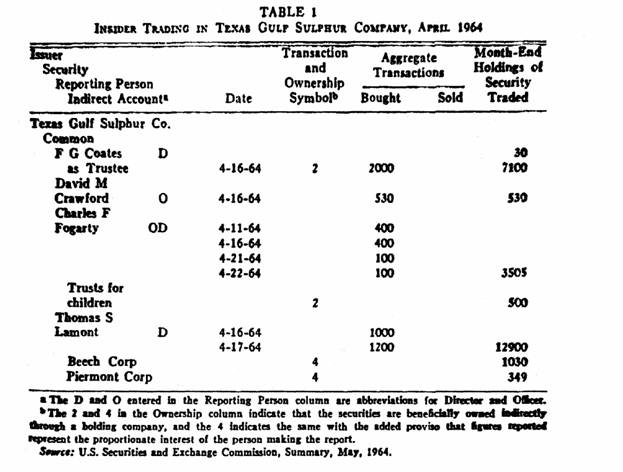

transactions by insiders of the Texas Gulf Sulphur Company in April, 1964.

Recall that on April 16, the company announced a major mineral discovery. Some

key dates and closing prices are: October 1, 1963—16 4/8; December

2, 1963—19 1/8; February 3, 1964—22;

April 1, 1964—26; April 13, 1964—30 7/8; April 16, 1964—36 3/8; April 30,

1964—52 7/8; and December 31, 1964—51 7/8. The Summary indicates that four

insiders and some associates just prior to, at the time of, or shortly after the

announcement of the discovery made purchases which proved highly profitable.

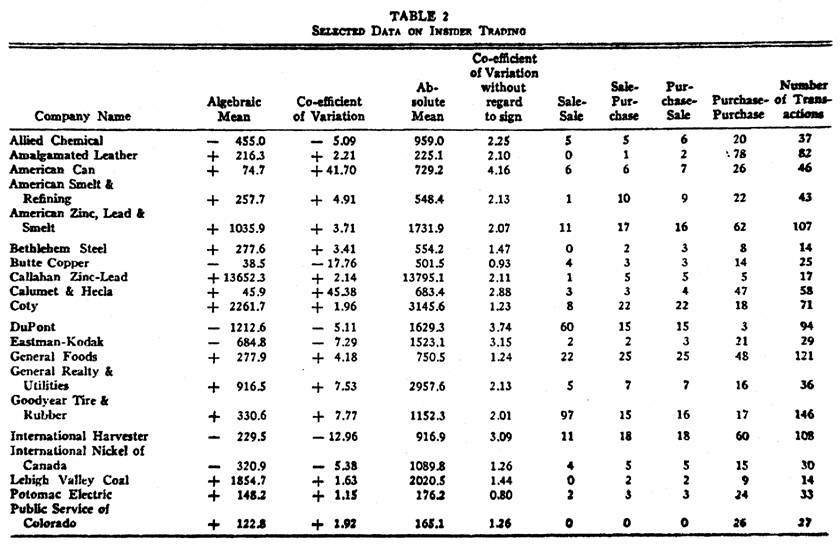

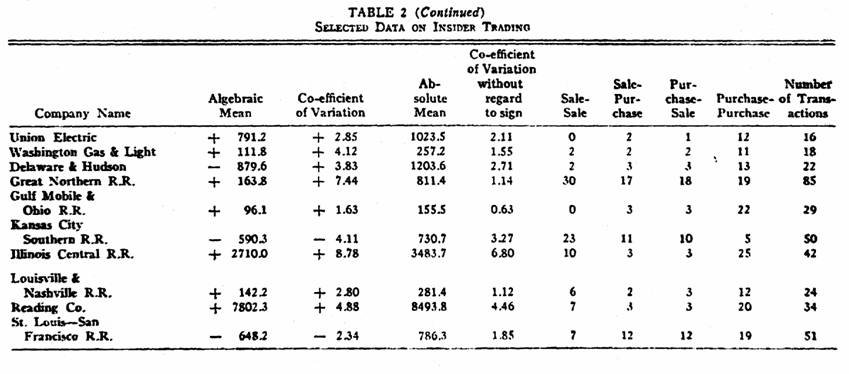

The most striking statistical property of

insider trading is the extremely great variation in the number of shares bought

and sold. This can readily be seen from means and variances of the algebraic

size of insider transactions in each of the 105 companies. The ratio of the

standard deviation to the mean (the coefficient of variation) ranges from 1.1 to

45.4 with a median of 11.3. By contrast, the coefficient of variation of the

monthly volume of trading of the industrial companies in the Dow Jones averages

is typically about 0.4.

Table 2

contains in columns 2 to 4 some measures of variation for 30 stocks in our

sample. Notice that 15 of the 30 coefficients of variation are greater than 5.

The average absolute variation between consecutive transactions is greater than

three times the mean absolute size of transaction in 22 cases.

One cause of variability is that different

kinds of insiders typically trade in significantly different numbers of shares.

Thus, during the period covered by this study, directors made 1305 transactions

with a mean purchase of 244 shares. Principal stockholders of more than ten per

cent of the outstanding shares made 1077 transactions with a mean purchase of

863 shares. Comparable results were noted by Smith using data from 1936-1938;

thus these differences are apparently stable.[8]

Transactions are heterogeneous in character.

There are 100 instances of gifts with an average size of 2195 shares. There are

326 exercises of rights with a mean “purchase” of 1001 shares.

Statisticians recommend stratification for

reducing the variance of estimates when the component groups are heterogeneous.

Such techniques at best might reduce the variance by a factor of five. It would

still be next to impossible to say anything useful about what constitutes an

unusual volume of insider trading in stocks.

Investment advisers have dealt with the problem

by analyzing the number of different buyers and sellers rather than the volume

of trading. Thus, the Value Line Investment Survey measures insiders’ interest

by cumulating the difference between the number of insiders who bought and sold

in the month.[9] This figure is divided into the number of officers and

directors in the company to compute the “Index of Insider Decisions.” The

Consensus of Insiders relies on a “one-man-one-vote theory.” They periodically

report the ten stocks for which the number of insiders who were net buyers

exceeded by the largest number those who were net sellers.

Since certain trading schemes based on the

number of transactions will be examined below, it seems desirable to consider

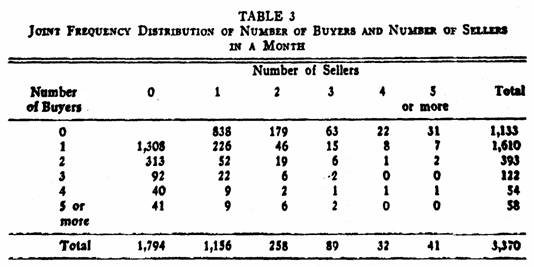

the statistical properties of the distribution of buyers and sellers in a month.

Table 3 contains the joint frequency distribution of the number of buyers and

the number of sellers in a month for the 3,370 company months in the sample. By

adding entries in the table, it is possible to construct the distribution of

total insider transactions in a month. In

2,146 company months,

there was only one insider transaction; in 718 months, there were two

transactions; in 253, there were three; and in 118, there were four. One insider

transaction during the month is 2.99 times as likely as two transactions, which

is 2.84 times as likely as three transactions, which is only 2.14 times as

likely as four transactions.

By subtracting entries, it is possible to

calculate the frequency distribution of the number of net buyers or sellers

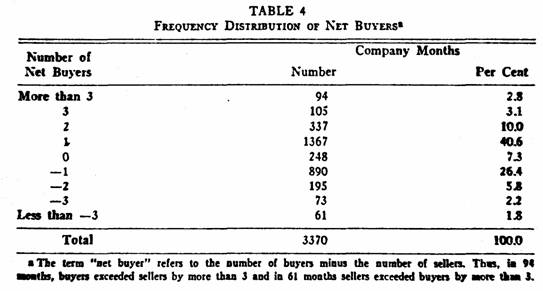

(Table 4). It is apparent that there were three or more net buyers in

approximately 5.9 per cent of all months when there are non-option and non-gift

transactions. There were three or more net sellers approximately 4 per cent of

the time. These numbers allow us to construct control bands that will filter out

unusual instances of insider trading for further scrutiny.

We shall follow this approach in some of our

own work reported in Section 3-B.

Throwing away completely the magnitude of the transaction, however, seems to us

to be inefficient. One solution is to weight transactions of different sizes by

scaling factors. For example, a purchase of between 100 and 500 could be

weighted by 1 and a purchase between 500 and 1000 by 2, etc., with an upper

limit of 10, say, for purchases above 4500. Transformations based on the

logarithm or square root of sizes of transactions may also be appropriate. On

the other hand, it is necessary to take with a grain of statistical salt such

headline reports as “Insiders Buy 5.1/2 Times More Stock Than They Sell During

the Hectic Three-Day Period in May.”[10]

Such reports are also suspect at some times,

since they fail to take account of a strong seasonal tendency in options. There

was a total of 916 option transactions in our sample and 408 of these

transactions occurred during the first three months of the year. This number is

6.8 standard errors away from its expectation of 229, if option transactions

were distributed uniformly. It turns out that option buying accounts for 70 per

cent of the total purchases in our sample. Therefore, in compilations treating

the exercise of option as purchases, we should expect the early months of the

year to show relatively greater buying.

The predictive implications of the exercise of

insider options have never been explored. This appears to us to be an oversight,

since other convertible securities such as warrants, convertible bonds, stock

rights, and call options have been studied in some detail. In most of the models

presented in these studies, the value of the convertible security depends on the

expected price of the common stock into which the security can be converted in

the future. When expectations concerning the future price worsen, the value of

the convertible security will decrease. For example, we would not pay much for a

one-year option to purchase the common stock of a company at 100 when we expect

the price of the company to move from 20 to 10 in the next six months.

Regulations throughout the period of the study require that an insider hold the

common stock he obtains through exercising the option for at least six months.

If an insider felt that the price of his stock six months in the future would be

permanently greater than the stock price prevailing thereafter, he would tend to

exercise the option.

Reasoning similar to this leads us to conclude

that the exercise of an option is a bearish event. But this view apparently is

not accepted on Wall Street or by the academic community. For example, Perry

Wysong treats options as equivalent to purchases in his Consensus of Insiders.

The Investors Statistical Laboratory lumps purchases and options together in

their aggregate figure for total insider trading in a month. And Glass, in his

suggestive Ph.D. thesis which we consider below, takes a similar tack. [11]

To test an implication of our theory that

options are bearish, we examined all occasions in our sample when the same

individual made both option and non-option transactions in a company during the

same month. It is very rare for an individual to be both a buyer and a seller in

the same month. In fact, in our sample, the odds were about 5 to 1 that an

insider with two transactions in a month made two sales or two purchases rather

than a sale and a purchase or a purchase and a sale. Thus, if insiders with

option trading tended to make purchases during the month in which he exercises

his option, we would conclude that options are similar to purchases.

In the entire sample of 8277 transactions,

there were only 31 company months in which an insider’s option transactions

coincided with a purchase or a sale by the same person. On 25 of these

occasions, the non-option transaction was a sale, on 6

occasions

it was a purchase. Although the sample is small, the results are

significant.

Finally, we can extend the test by comparing

the number of non-option purchases and non-gift sales by other insiders in that

company month when one or more individuals makes option transactions. There were

1688 sales and 1104 purchases on these occasions. There are significantly more

sales than purchases in conjunction with option purchases. Thus we conclude that

these two tests tend to corroborate our theory that options are more similar to

sales than to purchases.

We turn to a striking property of continuity in

insider trading. The successive insider transactions tend to be either purchases

or sales. Long runs of consecutive insider purchases or sales in a company are a

frequent occurrence. In our entire sample of 3973 purchases and 3277 sales, the

odds in favor of a purchase followed by a purchase were three times as great as

a purchase followed by a sale. Furthermore, the odds in favor of a sale after a

sale were twice as great as after a purchase, even though the unconditional odds

in favor of a purchase were 1.2:1.

A breakdown of the number of purchases

following purchases, sales following purchases, and sales following sales is

contained in columns 5 to 7 of Table 2.

Since the number of sales following purchases is within 1 of the number of

purchases following sales, the reader can calculate the odds of continuation of

purchases and sales for each of the 30 companies. For each of these 30

companies, a purchase is more likely after a purchase than after a sale.

The importance of this phenomenon is that one

purchase indicates that other purchases are likely to follow. The first purchase

tells more than subsequent ones. A change in direction from selling to buying

tells us the new fact that future purchases are to be expected, whereas a sale

followed by a sale merely confirms our preceding expectations concerning the

direction of insider activities. Therefore, the change in direction of activity

probably is of importance in deducing insiders’ expectations concerning their

stocks.

Some additional confirmation of this inertia

can be seen from Table 3. Consider a situation in which you know that there have

already been x buyers and y sellers in a month. The chances that the next

transaction will be a purchase increases as the ratio x/y increases. For

example, if there is already one buyer and one seller in a month, the odds that

the next transaction will be a purchase are 52/46 = 1.13. If there are two

buyers and one seller, the odds in favor of a purchase are 22/19 = 1.16. If

there are three buyers and one seller, the odds are 9/6 = 1.5. By focusing on an

entry high in any column in Table 3 and calculating the ratio of the number in

the same row but one column to the right to the number In the same column but

one row below, the reader may verify the phenomenon for other initial values of

the buyer-seller ratio.

Now that we know some salient features of our

insider trading data, we turn to several analyses of the predictive power of

data on trading by insiders. In all cases, we exclude from consideration the

exercise of options or rights and gifts.

SECTION 3-A.

INSIDER FORECASTS OF LARGE PRICE CHANGES

Do insiders buy before the announcement of good

news and sell before bad news? There is controversy about the answer. West

points out examples in which “because of new management, new products,

diversification, favorable legislation, technological advances, etc., a

successful metamorphosis was taking place. Meanwhile, prior to public

recognition of such transformations, insiders were quietly accumulating their

own stocks in the open market.”[12] There were numerous other examples in which

insiders sold near the highest prices reached by a “growth” stock.[13] After the

sales by insiders, we are led to surmise that a violent price decline inevitably

follows.

Fischer rejects this view in his 706-page

thesis. He finds that “specific corporate developments and important news

releases have apparently little, if any, influence on overall insider

transactions.”[14] And Driscoll in his careful M.B.A. thesis found “a lack of

speculative interest of insiders in connection with unfavorable dividend

action.”[15] Our own limited study of mergers, dividend reductions and

increases, and earning increases, etc., also failed to uncover systematic

exploitation of confidential information by insiders. For example, insiders were

net buyers in the six months previous to 17 of 30 randomly selected dividend

omissions during 1961-1964. Unfortunately, analysis of insider trading around

such events in isolation from the price movements of the company can never

reveal whether insiders profited from their information. For example, the price

of a stock frequently increases consistently before and after the announcement

of a dividend reduction and a decrease in earnings.

To resolve this problem, we have analyzed

insider trading before large price changes in a stock, defined as changes of 8

per cent or more. The frequency of these changes obviously varies with the

volatility of the stock. In our sample, approximately 10 per cent of all monthly

changes were 8 per cent or more and these changes accounted for approximately 30

per cent of total absolute variation in prices.

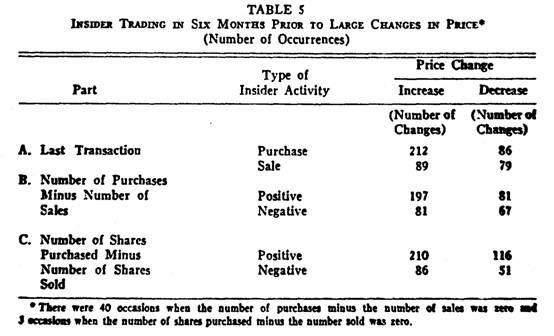

Insiders are superior forecasters of large

changes (Table 5). An investor choosing randomly between buying and selling

stocks would find that the ratio of large increases to large decreases following

his purchases (ratio A) was equal to the ratio of large increases to large

decreases following his sales (ratio B). We analyzed in three ways insider

transactions before changes. First, we analyzed the last transaction in the six

months before a large change. If the last transaction was a purchase, the

chances of a large increase were 71 out of 100. If the last transactor sold

stock, the chances of a large decrease were 53 out of 100 (Table 5-A). In other

words, the odds in favor of a large increase were 2.5/1 after a purchase and

1.1/1 after a sale. Differences between ratios at least as great as those

observed would occur in a sample substantially less than 1 in 10,000 occasions

if the universe from which it was selected had ratios of equal magnitude.

The second kind of analysis was of the number

of purchases and sales hi the six months prior to the large price change. The

odds in favor of a large increase were about 2.2 times as great when the number

of purchases was greater (Table 5-B).

The third inquiry dealt with the volume of

purchases and sales in the six months prior to the large price changes. The

evidence is much weaker than for the other two kinds of data, but again the

skill of insiders in forecasting large price changes is demonstrated (Table

5-C). There is a loss in information from aggregating the volatile figures on

the volume of purchases and sales.

SECTION 3-B.

PRICE MOVEMENTS AFTER INTENSIVE INSIDER ACTIVITY

We have already alluded to the theory that the

number of different insider purchasers or sellers in a month serves as a measure

of the extent of interest by insiders in a stock. Here, at last, we find

agreement. Investment adviser West states: “Insider accumulation deserves

further investigation if it consists of persistent purchases by several insiders

over a period of time.”[16] Rogoff, in his Ph.D. thesis, reports: “The

probability of a successful forecast of direction of price change of a stock

seems to be related to the number of its net buyers or sellers in a month.”[17]

Finally, Glass concludes: “Through the criterion of extensive insider

accumulation, an investor could have determined a limited group of

securities for which a fair probability existed that sufficient price

appreciation would occur to cause the group as a whole to significantly

outperform the Dow Jones Industrials over the near-term…”[18]

Rogoff reports on a study of all stocks which

in 1958 met the following criteria:

(1) They were purchased by

three or more insiders within one month.

(2) They were sold by no insiders in the month of intensive purchasing.

(3) At least two purchasers increased their holdings by more than 10 per cent.

The 45 stocks meeting these criteria

outperformed the market by 9.51 per cent in the six months following the period

of “intensive” purchasing.[19]

Rogoff also considers the number of occasions

that companies in which there was an excess of two or more buyers or sellers

outperformed the market. The odds in favor of an advance relative to the market

during the next six months are approximately 2.1 times as great in months in

which there were two or more net buyers as when there were two or more

sellers.[20] Differences this large would occur by chance less than 1 in 10,000

occasions.

Glass calculated for 14 selected two-month

periods the relative performance of companies for which there was intensive

insider buying during 1961-65. Glass included options as purchases rather than

excluding them as Rogoff did (or counting them as sales as we might advise).

Instead of choosing companies in which there were two or more net buyers or

sellers, Glass chose the eight companies for which there was the greatest excess

of buyers over sellers. Glass found that the companies he selected outperformed

the market by an average of about 10 per cent during the next seven months.

Despite these differences in coverage, definitions, and technique, he reached

conclusions similar to those of Rogoff.

The results of Rogoff and Glass are suggestive

but not decisive. The stocks meeting their criteria may have been more volatile

than the stocks in the Moody Index, and this greater volatility could have

accounted for their superior performance in a rising market.

Furthermore, Rogoff assumed that the insiders

executed their transaction at a price prevailing on a mid-month Friday, and

Glass used the first trading day in the next month. But under the present system

of reporting, the earliest an investor could be confident of finding out about

insider trading would be six trading days after the end of the month. As we

reported in Section 1, however, the insider actually buys at more favorable

prices (tower) than this latter price on about 75 per cent of all occasions.

Assuming that transactions are made with equal frequency throughout the month,

the price on a mid-month Friday is an average of 14 1/2 days closer to the

actual date of the transaction than is the sixth trading day after the end of

the month. A similar argument limits, though not as severely, the utility of

Glass’s conclusions.

To test the importance of the relationship

between intensive insider trading and subsequent price movements in stocks, we

chose 30 stocks at random from those included in Rogoff’s thesis. Calculations

of month-end prices from January 1961 to June 1964 were made for these stocks

and for the Dow Jones industrials on all occasions on which there were two or

more insiders buying or selling. There were 315 such occasions. During this

period, intensive buying and selling, as measured by Rogoff’s procedure, were

not useful predictors of stock performance in the subsequent six months (Table

6, Part A).

To gain further information concerning the

possibility of utilizing data based on insider trading, we studied a sample of

stocks for a period for which the exact dates of purchase and sales were

available.[21] For each transaction, the price on the exact date of the

transaction and the price six trading days into the next month were determined.

Percentage changes in price were computed over the next six months. These

changes were compared to changes in the Dow Jones Industrial Average over the

same period.

Data based on this procedure indicate a strong

relationship between insider trading and price movements (Table 6, Parts B and

C). Furthermore, there appears to be an opportunity for investors to profit from

knowledge of trading by insiders. Thus, when the number of buyers exceeded the

number of sellers by at least two, the probability was about 0.60 that the stock

would outperform the Dow Jones Industrials during the six months after

|

Table 6

PRICE MOVEMENTS RELATIVE TO THE MARKET

OF STOCKS WITH INTENSIVE INSIDER TRADING

(based on Price Changes During Six Months Subsequent to Insider Trading) |

|

|

|

|

|

Price Movements

Relative to Market |

|

Part |

Period |

Prices as of

Specified Date |

Type

of Intensive

Insider Activity |

Advance

(Number of Cases) |

Decline

(Number of Cases) |

|

A

|

1961-1964 |

End of

Month |

Excess

of 2 or More Buyers

Excess of 2 or More Sellers |

52

77 |

82

104 |

|

B

|

1963-1964 |

Exact

Date |

Excess

of 2 or More Buyers*

Excess of 2 or More Sellers** |

36

43 |

19

81 |

|

C

|

1963-1964 |

Six

Trading Days

After End of Month |

Excess

of 2 or More Buyers*

Excess of 2 or More Sellers** |

34

45 |

21

79 |

* Months with 2 buyers and

0 sellers are excluded

** Months with 2 sellers

and 0 buyers are excluded

the sixth trading day following the end of the

month in which the trading took place. When sellers exceeded buyers by two or

more, the probability was about 0.64 that the stock would perform worse than the

Dow Jones Industrials in the following six months. The probability that such

relative frequencies would occur by chance is substantially less than 1/100,000,

assuming that intensive insider buying and selling transactions were independent

of future price movements of individual stocks. Insider transactions were

slightly more successful when measured from the actual date of the transaction

than when measured from six trading days after the end of the month (Table 6,

Parts B and C).

During 1963 and 1964, the market rose

substantially. The possibility exists that companies in which there was

intensive insider trading were more volatile than other companies. More volatile

companies would be expected to perform better than the averages during a market

rise. To test this theory, we measured the volatility of each stock in which

there was intensive trading in 1963 or 1964. The measure of volatility we chose

was the regression coefficient in the regression relationship between the rate

of return on an individual security and the rate of return on the Fisher index.

This number measures the expected ratio of the companies’ percentage change in

price to the market’s percentage change in price. This measure of volatility is

highly correlated with other measures such as the mean absolute deviation and

the variance.

The median regression coefficient for all

companies on the stock exchange is approximately 0.95. If the companies in which

insiders made intensive transactions were more volatile than the market, more

than half of the coefficients for these companies should be greater than .95. In

fact, the results show that during 1963, 41 had coefficients greater than 0.95

and 43 had coefficients less than 0.95. Thus, we would conclude that the

volatility of the companies in which there was intensive insider trading was not

significantly greater than that for all listed companies and that the higher

rates of return for those companies apparently were not attributable to their

volatility.

SECTION 3-C.

DIFFERENCES AMONG COMPANIES IN THE CONSISTENCY

OF PROFITABILITY OF TRADING BY INSIDERS

In the preceding sections, we discussed the relationship between different

measures of insider trading and subsequent price movements in stocks, In this

section, we consider differences among companies In the profitability of trading

by their Insiders. Such differences might arise from differences in the

volatility of prices, policies concerning trading by Insiders, the Importance of

options or other things. It would be profitable for outsiders to be able to

identify companies whose insiders consistently trade on the basis of apparently

superior prescience regarding developments in their companies. To test the

existence of such companies, we again draw on work by Rogoff.

For

each of the 98 companies in his sample, Rogoff presented several measures of the

performance of insiders. For each company, Rogoff gave (a) the proportion of

months during which stock bought by insiders performed better than the market or

stock sold by insiders performed worse, (b) the probability of observing an

equal or greater number of successful predictions if the chances of a successful

prediction were 0.5, (c) the mean rate of return relative to the market of stock

bought by insiders, and (d) the mean rate of return relative to the market of

stock sold by insiders. Rogoff’s data cover the period from 1957-1960.

Using data from 1961-1964, we calculated

numbers comparable to Rogoff’s for each of 30 companies chosen at random. We

compared the profitability of trading by insiders in the same companies in both

periods. As far as we can detect—and we tried many approaches—there is no

tendency for insiders of individual companies to trade with superior success

during consecutive time periods. For example, the rank correlation between the

proportion of correct predictions in the two periods is —.01. Only 8 of the 15

companies with the highest proportion of successful forecasts in 1957-1960 were

among the 15 most successful during 1961-1964.

We also studied differences between the

predictive power of purchases and of sales. Successful forecasts of changes in

one direction only could occur because of a strong trend in the price of a

stock. Successful forecasts of changes in both directions are stronger evidence

of forecasting ability. There were 11 companies in which both selling and buying

insiders outperformed the market in 1957-1960. Six of them were among the 15

companies whose insiders traded least successfully in 1961-1964.

Further study is needed before we can reject

the conventional view of consistency of ability. It also might pay to examine

the transactions of individual insiders to see if any pattern of consistency

occurs. Our reported results, however, give no indication that these more

microscopic studies will be valuable.

CONCLUSION

This study indicates that proper and prompt

analysis of data on insider trading can be profitable, although almost all

previously published studies have reached the contrary conclusion. When insiders

accumulate a stock intensively, the stock can be expected to outperform the

market during the next six months. Insiders tend to buy more often than usual

before large price increases and to sell more than usual before price decreases.

We have been unable to find companies in which the insiders are consistently

more successful in predicting price movements than are insiders in general.

There is a pervasive continuity in insider

trading. Long runs of consecutive insider purchases or sales in a company are a

frequent occurrence. The odds in favor of a purchase followed by a purchase are

three times as great as a purchase followed by a sale. A change in direction of

activity from purchase to sale, or vice versa, is of importance in deducing

insider expectations concerning their stock.

There has been difficulty in previous studies

of insider trading in securing accurate in formation on prices and dates of

transactions. This lack of precision has tended to create the impression that

insiders are less successful in their trading than they actually are. In the

absence of an exact date of purchase or sale, the investigator has assumed that

the transactions were made at the average price for the month, or at the price

prevailing at the middle or at the end of the month. But, the price on the day

the insider actually made his transaction has consistently been more favorable

to him than the prices on the aforementioned date.

The Securities and Exchange Commission and the

stock exchanges should be encouraged to provide faster and more complete

dissemination of insider trading data.

Notes

* Funds to support this work came from the Center for Research In

Security Prices (sponsored by Merrill Lynch, Pierce, Fenner and Smith, Inc.) and

from the Ford Foundation. The authors wish to acknowledge the help of Lawrence

Fisher and Richard Zeckhauser.

[1] U.S. Securities and Exchange Commission, Official Summary of Stock

Transactions and Holdings of Officers, Directors, and Principal Stockholders

(hereinafter cited as Summary)

[2] The comparison was with the price six trading days after the end of the

month because “outsiders” could by that time have learned about virtually all

insider trading in the previous month.

[3] Henry Manne, Insider Trading and the Stock Market 164 (1966).

[4] Frank Percy Smith, Management Trading, Stock-market Prices, and Profits

141 (1941).

[5] Hsiu-Kwang Wu, Corporate Insider Trading, Profitability, and Stock Price

Movement 114-15 (unpublished Ph.D. dissertation in University of Pennsylvania

Library, 1963).

[6] Robert Shaw, Most Revealing Record of Buying and Selling by Insiders, 109

Magazine of Wall Street 498 (1962).

[7] Harriet West, In Encyclopedia of Stock Market Techniques 818 (1965).

[8] Frank Percy Smith, supra note 4 at

102.

[9] Letter from Value Line Investment Survey to

James Lorie, Oct. 19, 1965.

[10] Wall Street Journal, Sept. 24, 1962, at 6,

col. 3.

[11]

Gary A. Glass, Extensive Insider Accumulation as an Indicator of Near-Term Stock

Price Performance (unpublished Ph.D. dissertation in Ohio State University

Library, 1966).

[12] Harriet West, supra note 7 at

811-812.

[13] Id.

[14] Monroe Carl Fischer, The Relationship

Between Insiders Transactions, the Price of the Common Stock of Their Respective

Companies, the Standard and Poor’s Stock Price Index,

and Price

Stability 212-13 (unpublished

Ph.D. dissertation in American University Library, 1965).

[15] Thomas, E. Driscoll, Some Aspects of

Corporate Insider Stock Holdings and Trading Under Section 16(b) of the

Securities Exchange Act of 1934, ch. 6 (unpublished MBA thesis in University of

Pennsylvania Library, 1956).

[16] Harriet West, supra note 7 at 810,

[17] Donald L. Rogoff, The Forecasting

Properties of Insiders’ Transactions 100 (unpublished D.B.A. dissertation in

Michigan State University Library, 1964).

[18] Gary A. Glass, supra note 11.

[19] Donald L. Rogoff, supra note 17 at

15.

[20]

Id. at 96.

[21] To keep the computations manageable, we

did not consider those occasions on which 2 buyers and 0 sellers or 2 sellers

and 0 buyers made transactions.

[22] For a description, see Lawrence Fisher,

Some New Stock-Market Indexes 39, J. Bus. 191 (1966).

Read more by Victor Niederhoffer