Archives

Nov.

16-30, 2006

Write to us at:

![]() (not clickable).

(not clickable).

Please include your full name, and omit attachments.

|

Daily Speculations |

|

|

| |

Archives Write to us at:

|

30-Nov-2006

Incongruity Theory of Humor and Markets, from John De Palma

I have a couple thoughts related to your recent writing on the Humor of the Markets ... There was an article in The Economist last year on theories of humor:

One description of how laughter is provoked is the incongruity theory ... This theory says that all written jokes and many other humorous situations are based on an incongruity -- something that is not quite right. In many jokes, the teller sets up the story with this incongruity present and the punch line then resolves it ...

With the "incongruity theory" of humor, I'm reminded of something that interest rate analyst James Grant wrote a few years ago in Forbes when he was commenting on how he approaches the markets:

... I look for financial non sequiturs -- ideas and prices that apparently make no sense ... [The market] is not so efficient that it doesn't propagate, occasionally, titanic errors and absurdities.

On a separate note, the stadium indicator is being flagged again. A nuclear waste disposer will follow Delta Air Lines as the sponsor of the arena for the Utah Jazz

Gary Rogan adds:

I also believe that success in dealing with the markets and telling jokes is based on the common theme of incongruity. In my opinion though, there are substantial enough differences between the two areas to warrant very different approaches.

Punchline-based jokes rely on the following property of human brain that is becoming better understood with the latest research: people are always predicting the very near future when seeing, hearing, etc. Therefore, perfect timing in telling jokes depends on waiting just long enough for the setup to register and the non-humorous version of the punchline predicted, and then surprising the listener.

Market "jokes" tend to be not jokes at all but fairy tales. They work by suspending disbelief and lulling the "listener" into a false sense of complacency with what starts to seem like a perfectly natural state of affairs. There is no general sense of timing, as the "punchline" is revealed after a fairly unpredictable interval.

While a good sense of incongruity is useful in both areas, dealing with humor involves quick and obvious surprises, and with markets, digging out the non-obvious ones.

30-Nov-2006

Briefly Speaking, by Victor Niederhoffer

It is hard to believe that the moves of the Nikkei on Wednesday and Thursday overnight, before the US stocks opened, were not indicative of the imminent break through from below of the round 1400 by the S&P, but this must be tested.

| NIKKEI (NI1) | S&P (SP1) | |||

| Date | Open | Close | Open | Close |

| 1-Nov | 16375 | 16380 | 1386.1 | 1372.9 |

| 2-Nov | 16395 | 16350 | 1368.8 | 1371.3 |

| 3-Nov | 16350 | 16330 | 1375.8 | 1368.5 |

| 6-Nov | 16320 | 16380 | 1372.8 | 1383.8 |

| 7-Nov | 16385 | 16420 | 1385.0 | 1389.0 |

| 8-Nov | 16420 | 16235 | 1382.5 | 1391.6 |

| 9-Nov | 16235 | 16245 | 1392.5 | 1384.0 |

| 10-Nov | 16240 | 16080 | 1383.5 | 1384.8 |

| 13-Nov | 16085 | 16020 | 1384.0 | 1388.0 |

| 14-Nov | 16025 | 16295 | 1391.3 | 1397.7 |

| 15-Nov | 16300 | 16260 | 1397.0 | 1401.5 |

| 16-Nov | 16270 | 16170 | 1405.4 | 1405.1 |

| 17-Nov | 16175 | 16065 | 1400.2 | 1404.8 |

| 20-Nov | 16065 | 15735 | 1403.2 | 1405.3 |

| 21-Nov | 15740 | 15720 | 1404.8 | 1406.2 |

| 22-Nov | 15720 | 15855 | 1407.0 | 1408.4 |

| 23-Nov | #N/A | #N/A | #N/A | #N/A |

| 24-Nov | 15800 | 15725 | 1401.6 | 1402.9 |

| 27-Nov | 15725 | 15860 | 1401.9 | 1383.6 |

| 28-Nov | 15860 | 15865 | 1381.2 | 1388.6 |

| 29-Nov | 15855 | 16080 | 1392.7 | 1402.2 |

| 30-Nov | 16080 | 16310 | 1402.5 | 1402.9 |

An Earnest Spec replies:

On a related note regarding moves in the East, I was wondering if you might critique this Kindergartner's effort in the quantitative world. What is worthy? What is worthless? What to add? What to omit?

IF was up 9.5% yesterday, completing a five-day percentage gain of more than three standard deviations above the average five-day percentage change measured over the last 30 trading days. I queried IF's history for like moves while trading over the 200sma. The table is expressed as percentage change, T+(X) days out from yesterday's event.

| Date | t+7 | t+8 | t+12 | t+28 | t+30 |

| 04/23/1992 | -7.1 | -7.1 | -5.9 | -2.4 | -1.2 |

| 05/28/1993 | 2.3 | 0.0 | 2.3 | 3.5 | 3.5 |

| 12/27/1993 | -11.1 | -15.3 | -21.7 | -22.8 | -24.9 |

| 05/11/1995 | -6.1 | -7.1 | -6.1 | -8.2 | -8.2 |

| 04/25/1996 | -5.7 | -3.8 | -2.8 | -5.7 | -6.6 |

| 07/08/1997 | -11.1 | -11.1 | -16.2 | -29.3 | -33.3 |

| 01/06/1999 | -11.9 | -3.0 | -14.9 | -9.0 | -10.4 |

| 06/08/1999 | -4.5 | -3.6 | -1.8 | -5.4 | -11.6 |

| 08/23/1999 | -8.6 | -10.8 | -14.0 | -8.6 | -11.8 |

| 04/09/2002 | -4.0 | 0.0 | -0.4 | -6.0 | -5.2 |

| 05/09/2003 | -6.7 | -6.7 | -1.8 | -0.9 | 0.9 |

| 10/13/2003 | -1.3 | -2.9 | -4.0 | -5.1 | -6.9 |

| 12/26/2003 | -14.1 | -14.2 | -16.8 | -23.7 | -22.0 |

| 11/29/2006 | NaN | NaN | NaN | NaN | NaN |

| Avg | -6.9 | -6.6 | -8.0 | -9.5 | -10.6 |

| AvgPos | 2.3 | NaN | 2.3 | 3.5 | 2.2 |

| AvgNeg | -7.7 | -7.8 | -8.9 | -10.6 | -12.9 |

| PctPos | 7.7 | 0.0 | 7.7 | 7.7 | 15.4 |

| PctNeg | 92.3 | 84.6 | 92.3 | 92.3 | 84.6 |

| Maximum | 2.3 | 0.0 | 2.3 | 3.5 | 3.5 |

| Minimum | -14.1 | -15.3 | -21.7 | -29.3 | -33.3 |

| StdDev | 4.5 | 5.0 | 7.7 | 9.7 | 10.6 |

| Avg/SD | -1.5 | -1.3 | -1.0 | -1.0 | -1.0 |

| Date | t+7 | t+8 | t+12 | t+28 | t+30 |

| 01/06/1999 : 1 Obs. | Min. :-14.100 | Min. :-15.300 | Min. :-21.700 | Min. :-29.300 | Min. :-33.300 |

| 04/09/2002 : 1 Obs. | 1st Qu.:-11.100 | 1st Qu.:-10.800 | 1st Qu.:-14.900 | 1st Qu.:-9.000 | 1st Qu.:-11.800 |

| 04/23/1992 : 1 Obs. | Median : -6.700 | Median : -6.700 | Median : -5.900 | Median : -6.000 | Median : -8.200 |

| 04/25/1996 : 1 Obs. | Mean : -6.915 | Mean : -6.585 | Mean : -8.008 | Mean : -9.508 | Mean : -10.59 |

| 05/09/2003 : 1 Obs. | 3rd Qu.: -4.500 | 3rd Qu.: -3.000 | 3rd Qu.: -1.800 | 3rd Qu.: -5.100 | 3rd Qu.: -5.200 |

| 05/11/1995 : 1 Obs. | Max. : 2.300 | Max. : 0.000 | Max. : 2.300 | Max. : 3.500 | Max. : 3.500 |

| Other : 7 Observations | |||||

t.test(Dataset$t.7, alternative='two.sided', mu=0.0, conf.level=.95)

One Sample t-test

data: Dataset$t.7

t = -5.492, df = 12, p-value = 0.000138

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-9.658867 -4.171903

sample estimates:

mean of x

-6.915385

t.test(Dataset$t.30, alternative='two.sided', mu=0.0, conf.level=.95)

One Sample t-test

data: Dataset$t.30

t = -3.6192, df = 12, p-value = 0.00352

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-16.969087 -4.215529

sample estimates:

mean of x

-10.59231

30-Nov-2006

Henry Carstens Reviews Dr. Brett's

Latest Book

Dr. Brett Steenbarger has written a new and wonderful book, Enhancing Trader Performance, that has kept me thinking about trading, performance and niches since I got it.

The book starts with four composite traders built up by personality type. It's just so fascinating to see oneself illuminated that way. Next, the book takes each composite trader through a series of hurdles before he discovers his trading niche. Again, quite illuminating and it sets the stage for the second part of the book which provides sound, proven tools and techniques for performance enhancement.

The book is beautifully written, easy to read and worth orders of magnitude more than the price of admission. A psych book for quants -- imagine that!

30-Nov-2006

Barron's Roundup, from Professor Gordon Haave

Abelson: The O.J. episode happened. A handy chart tracks the number of times the press uses the word "goldilocks". It is up lately, which might mean people are using that as a reason to stay bullish in the face of bad news. (Of course, a simple look at the chart shows basically zero correlation between the number of times goldilocks is used in the press and later stock market action.) The dollar has gone down, it will go down further, which will hurt the economy. Miracle of miracles, there is some good news: The world is awash in liquidity. In other news, the sky is falling.

Page 18 (follow-up section): We were wrong about B of A. The US Trust purchase was smart, and B of A stock is doing well. Avon stock is up despite lack of improved fundamentals, plus there are a lot of clouds on the horizon. Snap-On Tools has been doing great.

Page 21: One of the reasons there has been so much buyout activity is that corporate managers are risk adverse compared to the LBO guys. With debt financing so readily available, the LBO guys have been willing to load up their targets with debt... something that corporate and/or strategic buyers aren't willing to do. This has given the LBO guys an upper hand in the buyout game. The Private Equity boom will end badly if the economy weakens.

Page 22: The Schwab Equity Ratings system has been doing great. The guy who designed it doesn't focus on forecasting earnings, rather he looks for factors that help to predict earnings surprises. Free Cash Flow is the most important factor. He also compares inventories to sales. Profit margins have no correlation with future stock returns.. rather FCF to equity does. Another good indicator is comparing rates of change in sales vs. assets. The higher the capex rate, the lower the return over time, for various reasons. Tracking short selling in a stock also had predictive ability.

Page 25: Lots of people have Hepatitis C, and there is no cure. Wall Street is betting on Vertex to find one. However, the doctors think you should be looking at IDIX, ITMN, ACHN, VPHM, XTLB. You can read the rest of the article to learn about Hep. C, or you can just google it.

M3: For those of you cruising the Gulf of Bothnia last week, there were a lot of big buyout deals, Dell did well, and the dollar declined, resulting in profit-taking by Kirk Kerkorian and insiders in general. It was a good week for copper stocks, and it could get better. The Phelps bid could move higher. KFC has a new logo, and a nice start in China. Large cap stocks are finally outperforming small caps.

M6: Lots of reasons to worry about Google, mostly that we haven't really seen any sort of big payoff to its non-cores businesses yet. Fred Hickey things consumer spending, which will hurt Google advertising.

M7: There are lots of people in China who don't have mobile phones yet, so buy China Mobile and China Unicom.

M8: M&A activity is going crazy, and bondholders are taking it on the chin. It used to be you could buy the bonds of big, safe, companies and be ok. Not anymore. Deal sizes are huge, and getting bigger. Bondholders are fighting back, asking for better covenants.

M9: It used to be that options markets predicted takeovers, but that didn't happen on the big deals last week. The reason is two fold: 1. The prevalence of all cash deals (that makes no sense to me whatsoever, the stock will still go up if the cash is at a premium), and perhaps there is so much option volume it is not as obvious that there are inside traders. The new technique for insiders is selling calls that go out more than a year.

M11: Air France-KLM is silly for even thinking of buying Alitalia. So silly, that people are speculating that there are political reasons behind the deal.

M14: Gasoline futures have been clobbered lately, but they should do well through the winter, better than crude oil.

Page 27: It used to be that philanthropists gave their dough to popular causes like hunger relief. Now people are tailoring their giving in a much more narrow manner where they feel they can have a greater impact and more personal meaning. There are 4 pages of various example of this, if you care.

Page 32: You don't have to give away cash, you can give away stuff like rare books. You should talk to a lawyer to figure out if you should give them directly, or give them to your family foundation and then sell them, etc.

Page 34: A Mellon activist hedge fund wants ASM International to break up. ASM doesn't want to. This is ironic because Mellon is having the same problem with its shareholders. Either way, ASMI shareholders should be winners.

Page 35: The Human Genome Organization needs help naming new genes. The CEO of Cyberonics stepped down.

Page 36: There is a pretty cool Wine service called Vintrust. You buy wine, and store it at their facility. Then, you can trade wine back and forth with people, and all it does is require the moving of the barcode on the bottles. They have about 2 million bottles under management.

Page 37: Buying insurance online is pretty cool, but you still want to take your time and know what you are getting. With a lot of these sites, after you enter all your info, etc. you get phone calls from insurance agents, which is a pain.

Page 38: The AMT was designed to snare people who used every trick imaginable to avoid taxes. However for a few reasons, including inflation, it is nailing all kinds of people. It is not fair, and needs to be changed.

Page 39: Hedge fund Roundtable. blah blah blah. Overview of strategy returns. Going forward, M&A activity will continue. A way to hedge against geopolitical events is to go long volatility by buying VIX options. If Volatility goes up, equity markets will sell off, credit spreads will widen, and the dollar will strengthen. Where are we in credit cycle? Defaults low but rising, when will it really head up - who knows? 50% chance credit cycle goes bust next year. Interesting take on Amaranth: Investors were screwed because the creditors were running the show with nobody looking out for the investors.

Page 44: Joe Queenan went to the $99 dollar wealth Expo at the Javits center that Trump spoke at. The two pages can be summed up as: "As you might have expected, it is one big fraud, and the people who pay many for this thing are idiots".

Page 45: The democratic congress is going to try to force net neutrality, which is the dumb idea of forcing the fiber providers to charge the same thing to everybody, when really they should be able to charge more to access bandwidth clogging sites.

Page 46: Interview with Will Chester of the Westcore Select Fund. It is a midcap growth fund. He oversees $2.8 billion. He thinks midcap growth stocks are great. He likes DOX, CSE, ERTS, STZ, DVA, GHCI, DOV, OSK, TPX, COH. Also, CAL and AMR. He just sold TROW because of valuation. The playstation 3 and Nintendo Wii will help Electronic Arts and Gamestop. He has a positive outlook on health care.

Page 47: Everyone tells you to diversify, but if you want to build wealth you need to concentrate and leverage your investments. You also need to be a hard-core contrarian investor. For example, you should like GM and F better than Toyota or Honda. Sometimes, of course, beaten down companies stay beaten down, like Kmart. Take a look at the Forbes 400, most got there because of large concentrated bets.

Page 48: Silicon breast implants are back on the market, and Mentor and Allergan, who make them, are up, and could go higher.

Page 51 Editorial: Airlines lose lots of money in general, despite there being lots of travelers. They keep buying lots of new planes during the good times, and receiving them in the downturns. The US Air and Delta merge will be bad news, and synergies are never realized. The bankruptcy judge should liquidate Delta.

30-Nov-2006

Ken Smith Contributes to the Department of Self-Improvement

Vocabulary brings the world to an individual. Without words we are reduced to surviving by non-verbal signs and gestures, primitive. Basic survival.

Some have expressed irritation when I write about incarceration, convictions, and whatever is associated with penal servitude, but any convict can vastly improve his life if while serving time he takes up the task of building his vocabulary.

My grandmother sent me a Webster's Dictionary and a thesaurus at my request when I entered Walla Walla State Penitentiary without more than a 9th grade education. I took a liking to words and began reading just the dictionary.

In adult life I carried a pocket thesaurus, in my shirt pocket, and whenever a moment was idle I would read it.

A pocket thesaurus, maybe leather bound, would be perfect gift for any occasion, as a birthday for a child with some basic language skills to evolve with.

One word can lead to another, to an association. One association leads to another, until the student has gone into another dimension and left others behind.

I did not however, leave my street vocabulary behind and I cherish the way it can embellish a conversation with exclamatory frills.

Stefan Jovanovich comments:

Ken would have been right at home in 1780. In the 18th century nine out of ten Americans could read and understand the King James Bible, and all who could afford it owned a copy. (Today only an optimist would argue that the number was higher than three out of ten.) The extraordinary exception of the American Revolution and the Federalist Papers comes from the fact that the "average" American of that time had a larger vocabulary than present day college graduates. That fact also explains the lethality of Continental marksmanship that the British Army so justly complained about. The use of rifled barrels has been the conventionally accepted academic explanation, but the far more likely one is the extraordinary literacy of the "ordinary" American soldier, who carried a musket (not a rifle). The ability to read and write and think correlates directly with the ability to shoot, as Scott Brooks' postings and hunting skills amply demonstrate.

Those of us who hate the draft do so for two simple reasons: it is a reminder of how far we Americans have gone on the road to serfdom, and dumb conscripts make lousy soldiers. The two best memoirs of "ordinary" American soldiers were written by Joseph Plumb Martin and E. B. Sledge. The first was an 18th century farm laborer; the second a 20th century biology professor. Both were volunteers.

29-Nov-2006

Dr. Kim Zussman Flirts with Evolution

A very cute 26 year young lady was temping at the office recently and told of her experience at a convalescent home where she had just quit. It seems there is an 87 year old Romeo who, just as she turned around, planted a big wet one right on her lips.

Another lady who works there and is pregnant is telling this guy, who has some Alzheimer's, that the baby is his.

From a Darwinian view, a man of any age should construe any attention from a woman as an invitation (evolution occurred before lawyers); the goal is maximum projection of genome into the future, and you have to risk refusal to get it there.

In Russia flirting, sexual innuendo, and fondling, which used to be legal here between opposite sexes, is alive and well. Funny thing is, most of it is in jest (a Russian aphorism: "Every joke has some truth to it") and women crave the attention tremendously. In fact, even married Russian women become quite furious if they cast a furtive glance at a man and he doesn't respond. Even though they are busy poisoning their enemies, they haven't yet polluted the soul.

29-Nov-2006

Towing Icebergs, by Victor Niederhoffer

The main point of Towing Icebergs, Falling Dominoes, and Other Adventures in Applied Mathematics by Robert B. Banks, is that mathematics is a language that can describe, measure, and help inform us about everyday points of human activity. The book uses mathematics such as differential equations, integro differential equations, the calculus of variations, and some physics (mainly the laws of motion and free body diagrams) and statistics (least squares regressions). Using these methods Banks explains many events such as; the impact of objects falling from the sky, the shape of a sagging flexi-cable, the shape of a jumping rope, how to throw a curve ball, how strong waves are, oscillations in the records of football teams, how fast one can run and how high and efficiently one can jump, how strong bridges and buildings are, how fast epidemics spread, how far it is possible to tow an iceberg... and how fast dominoes fall.

Like all good books, this one can be read on many levels and many times over. I read it because I want to see how math could better prepare me to understand the physical and market factors that move. I found it very interesting in this context, and particularly liked the many uses of the Logistic equation to explain such as the spread of rumors. I also enjoyed seeing the various estimates of pi that simple geometric diagrams like inscribed circles in a square can generate.

Unfortunately the author is woefully uninformed about statistics. Indeed it does not look like he knows how to compute a standard deviation from individual observations, as he classes observations into groups and intervals and then computes the standard deviation based on the numbers in each group rather than the individual observations. Nor does the author know about the common limitations of regressions, when such factors as multi-co-linearity appear, and why one should hesitate to use squares and cubes in some regressions. The chapters where he applies mathematical methods to deficits and debts contains numerous omissions and errors of analysis. His discussion of predicting the future height of a child based on the child's percentile height at an early age, which is the kind of thing that market people think about all the time, is terribly naive and misleading. Indeed on all the subjects that I have even a rudimentary knowledge of, such as those that touch on economics, I find the discussions and models painfully inadequate. But they are suggestive.

The author is a professor of fluid mechanics and he is not sheepish about believing that the lay reader has some expertise in that field. Within the first eight pages he develops a mathematical model of a baseball that assumes the reader knows about functional relations between viscosity, roughness, velocity, the Reynolds number, the velocity of sound in a gas, and such things as the Fronde and Weber numbers. Admittedly , my physics knowledge is deficient, having had only a college level course in the field and dabbling in electronics as a hobby, but it would have seemed that the author could have chosen a subject for his introductory chapter that the educated layman who he is writing for, might have had more familiarity. Indeed, most of the chapters suffer from either being much too technical for a reader not familiar with physics and accustomed to using such things as free body diagrams, or, when the author deals with economics, being much too naive and out of date to have much import.

Despite this, the topics covered raise many interesting ideas and tests for the market speculator. Some that sprang to mind after reading the book the second time were: What is the area of a chart that is covered by points, and lines, relative to randomness? How long can one market tow another along for? What is the time to travel a certain distance in a market that is showing parabolic growth? What is the price limit of how much a soybean oil can sell for when it is limited by the size and price of the soybean crop itself -- perhaps according to a logistic relation? What is the easiest and most effective path for a price to take from one level to another a'la a pitcher throwing a curve ball to the plate? How high can a stock go, based on its initial ascent during a year or a day?

The author is apparently an old timer who likes to use puns and jokes, and I believe that his persona and style is captured by the following quote:

I decided to be a bit light hearted in the analysis of some of the problems. It just seemed like a good idea to not always be entirely serious about everything.

I recommend this book to all market people who have a reasonable interest and background in physics, and to all others who like to gain insights from other fields and other methods of analysis that might help them to improve their feel for the markets.

Rick Foust adds:

For anyone seeking a practical compilation of engineering formulas and methods, the books engineers use to prepare for Professional Engineer exams are hard to beat. These are available at most university book stores.

Or If you prefer a high tech approach Mathcad is the tool of choice. And then there are various widely accepted topical references, such as Crane Technical Paper 410, Flow of Fluids.

But as in statistics, it is essential to understand the assumptions implicit to the formula.

A standard engineering calculation follows the format: Problem Statement, Data, Assumptions, Formulation, Calculation and Conclusion. Of these sections, "Assumptions" is the most important. Assumptions are the cornerstones for calculations ranging from bridge to nuclear reactor design.

The worst calculations I have seen were generated by engineers having excellent memories yet poor understanding. As an example, such a fellow engineer once asked me to verify his perfectly logical three page calculation that proved a long bolt can take more torque than a short bolt (it can't, of course). Fortunately, important calculations are typically verified by a second engineer, and engineers like to find things wrong with the works of other engineers.

29-Nov-2006

A Book List, from Victor Niederhoffer and Laurel

Kenner

Our readers often ask what suggestions we have to generate new ideas and improve knowledge. We have a book list of essential reading as a background for everything else, but often supplement these books with current texts in related fields that we find at good book stores on our visits to bookish cities (like London, where we prefer Hatchards and Blackwell). Here are the books we purchased on recent trips to Chicago and Austin:

29-Nov-2006

Prehistoric "Jaws", from Dr. Kim Zussman

The fossil record of life on earth can be read as sequential ecological dominance. It is interesting how formidable species at the top of then-current food chains often become extinct.

Dunkleosteus terrelli is a fish which bit with 11,000 pounds of force (twice that of great white shark), which along with other big-biters (T. Rex) are dodos of other eons.

When this creature terrorized oceans full of big prey, what were eminent forces that would end his reign? Temperature change? Small prey? Disease?

Species success and dominance appears to require risks of commitment and inertia, which pay off competitively but increase vulnerability to unforeseeable environmental shifts.

Dylan Distasio comments:

An interesting creature for sure ... This type of fish (Placoderm) was wiped out in one of Earth's great mass extinctions in the late Devonian period. It is rather startling to look at just how many species died as a % of the total on Earth during any one of the given recorded mass extinctions.

28-Nov-2006

The Joy of Soft Landings, from George Zachar

| Quarter/Quarter Activity Annual Returns | 3rd Quarter 2006 | 2nd Quarter 2006 |

| GDP | 2.2% | 2.6% |

| Goods | 3.7% | 3.6% |

| Services | 3.0% | 2.4% |

| Quarter/Quarter Annualized Prices | ||

| Market based PCE | 2.2% | 4.2% |

| PCE Price Index | 2.4% | 4.0% |

| Market PCE Core | 1.9% | 2.7% |

| PCE Core Prices | 2.2% | 2.7% |

| Year/Year | ||

| Market based PCE | 2.6% | 3.2% |

| PCE Price Index | 2.8% | 3.3% |

| Market PCE Core | 2.0% | 1.9% |

| PCE Core Prices | 2.4% | 2.2% |

Note: This moderate and modest report will no doubt be seen on Constitution Ave. as validating both the Fed's pause and the markets' dampened vol readings.

28-Nov-2006

Balderdash, from Robert McAdams

Over the holiday my family and I played a board game we've played many times before named Balderdash. The game is pretty straightforward. A dealer pulls a card containing several categories ... a name, a date, an acronym etc. The entries are almost entirely unknown to the players. The goal then of each player is to make up a trivia fact that is believable to the other players. These fake facts are added to the real one and read by the dealer to the table. Points are awarded for picking the truthful fact, as well as getting other players to pick the one you conjured. The dealer scores by convincing the other players not to pick the correct one.

This got me to thinking about the markets, life and bluffing specifically. When prices change, people wonder why. The truth is always that the supply/demand relationship has changed, but there are many people willing to fill in the "answers". What are the motives of those supplying the answer.

In the game, one of the strategies employed is to pick the answer that you made up in an attempt to convince other players to do so. Do market participants ever do this? Generally, the more believable the fact you make up, the better. But sometimes, a preposterous answer works wonders. People simply can't believe its made up. When several answers have equal believability, the ludicrous answer stands out. The players almost talk themselves into believing it. Do we ever talk ourselves into things we know are bold faced false? When I was the dealer I always read the true answer somewhere near the middle. I know that in any list, the first and last thing a person hears sticks in their mind. Is the first explanation given for a market move the one that will be believed going forward, even when a better truthful answer comes along? I would like to hear more about bluffing from your readers.

Steve Wisdom adds:

Santa brought us a game called Blokus last year, and, as mentioned by Tom Ryan, kids are eerily capable at it. Like Checkers and 9-Ball and (circa 1982) Space Invaders, it has a beautiful simplicity that hides much depth.

Also, Blokus can easily be 'handicapped' by a simple rule such as 'adults must play their pieces from smallest to largest' (i.e., starting with the 1-square piece). I like to play the kids even-steven, subject to a some such simple constraints or rules-changes, but I find that not all games lend themselves to this. (Though many do: e.g. at Go Fish, I play level with the kids if I enforce on myself 'wait one full turn before asking for a card I just picked up!')

Another great game to play with kids is Mille Bornes, though it seems not to be as widely circulated nowadays. They do make a new version, but I bought a 1970s set for a few dollars on eBay. It is self-handicapping because the kids gleefully gang up on Dad, taking delight in fixing my wagon again and again... until they get close to 1,000 miles and need to turn their attention to each other.

28-Nov-2006

Market Swings, by Victor Niederhoffer

In the office we were talking about the repeated action of the S&P's move to a certain level, and then it's falling back from this level, that occurs on a day like today. This repeats until the potential energy of the market is converted to kinetic energy, and the market rises higher. We were looking for analogies for this, such as power lifting where you bounce the weight before extending it to maximum lift, or pole vaulting where you can take up to three tries to get over the bar. In the process of this we were also considering the energy transfer involved in making a child's swing set go higher with each swing. The following brief explanation was found but I would be interested in any ideas people have on a proper model for the back and forth; the trying to get there but failing, that happens so often in the markets.

Each time the swing moves forward and then returns to its starting position counts as one cycle. Using a stop watch determine the length of time a swing needs to complete say 20 cycles. Divide 20 cycles by the time and you have the swings frequency in cycles per second or Hertz (Hz).

Since a swing is basically a pendulum it's possible to calculate its resonant or natural frequency using pendulum equations as follows:

Note that the natural frequency of the swing is not influenced by the mass of the person in it. In other words' it makes no difference whether a swing has a large adult or a small child in it. It will have the about the same natural frequency. Slight differences can be caused by slightly different locations of the person's center of mass. This is located about two inches below the navel. When people are sitting the center of mass is in about the same place relative to the seat of the swing regardless of whether the person is an adult or a child.

If a forcing function is applied to a swing at the natural frequency of the swing it will resonate. The amplitude of the swing will increase during each back and forth cycle. The forcing function can be provided by a second person pushing on the swing. In this case even a small child can make a large adult swing by pushing in sync with the swing's back and forth cycle. The forcing function can also be provided by the person in the swing. In this case the person in the swing shifts her center of mass very slightly by changing the position of her legs or torso. This creates a slight pushing force which makes the swing go higher and higher. It takes a very small force but it has to be timed perfectly.

The big question is what keeps the swing from flying apart or spinning over the top of the swing's frame and subsequently killing its rider? After all, if it is a resonating system then it should be very dangerous to keep applying force in time with the swing's frequency. The answer is fairly simple. The equation given above is only good for small angles. When the swing goes beyond a certain height it is no longer possible for the person in it to apply the necessary small force in sync with the natural frequency because the natural frequency changes. In other words the motion of the system is naturally limited.

Jim Sogi offers:

The apparent back and forth motion around the round number is a chart artifact, and as with so many chart artifacts is an illusion. The motion is in three dimensions and only appears on the chart in two. The model is a tether ball, like at summer camp. It has circular momentum from whacking it, and tightens, then rebounds off and unwinds. The angle of the wind depends on the angle of the whack. Circular math a'la Newton might work.

The other model is a guitar string. It has harmonics and standing waves along its length as the axis of vibration meet along the string, similar to price action harmonics. The higher harmonics are recreated in the higher and lower price levels.

Gary Rogan comments:

I also view the market gyrations as something similar to a swing, except it's nothing like a physical, earthly swing because there are two forces involved, and one of them is "unusual" for a physical-world system. In the physical world, there is only gravity (other than a small amount of friction) involved in the dynamics of a swing that results in a simple differential equation describing the motion for small deviations. I see two basic "forces" involved in market motion: "momentum" and "value pricing". Positive momentum is the force that causes people to buy when the market is moving up (buying interest proportional to market velocity), negative momentum is the force that causes people to sell when the market is moving down. Thus momentum is a force proportional to velocity, sort of like inverse friction that doesn't exist in the real world. Value pricing is what causes people to buy when prices are "too low" and sell when they are "too high".

Of course all of this exists in the environment of slow upward drift and real-world-like friction of various trading costs as well as news events and money-supply formations that are not completely dependent on the immediate market dynamics. The relative amplitudes of the two forces also change with time.

Normally the two forces are balanced enough to keep the market gyrating around some sort of a temporary equilibrium that itself is slowly drifting. However, when the momentum force gets too high (as in 2000) it will break the swing.

Jeff Sasmor adds:

Another thing to consider is inertia. There is a nice article on this in Wikipedia and other sources.

The principle of inertia is one of the fundamental laws of classical physics which are used to describe the motion of matter and how it is affected by applied forces. Inertia is the property of an object to resist changes in velocity unless acted upon by an outside force. Inertia is dependent upon the mass and shape of the object. The concept of inertia is today most commonly defined using Sir Isaac Newton's First Law of Motion, which states:Every body perseveres in its state of being at rest or of moving uniformly straight ahead, except insofar as it is compelled to change its state by forces impressed. [Cohen & Whitman 1999 translation]

Perhaps this explains the recent upwards moves in stocks in spite of multiple discouraging memes. Humans have a lot of inertia, we've probably programmed a lot of it into the machines that do a lot of the trading these days.

It's odd that this came up today, I was mulling the concept last night before falling asleep. Interesting questions that came up are:

It is a system with a lot of inputs and time-varying coefficients. Maybe it's a reverb chamber?

David Wren-Hardin mentions:

Swings and oscillations are found throughout nature where systems on different time courses interact with each other. One obvious relationship is the classic predator-prey population dynamic. As prey animals increase in number, predator numbers rise on a lagging basis. A peak in prey animals is followed by a crash as they consume their resources, dragging the numbers of predators with them. One can cast value investors in the role of rabbits, with their steady grazing on low-calorie fare, and the momentum investor in the role of the coyote, waiting for concentrated packets of dense nutrients. Or one could place the casual investor in the role of rabbit, and the average financial professional in the role of coyote, but I'll refrain from that comparison so not to risk defaming the coyote.

Animals also use oscillations to find out information about their environment, much like the technical analyst or trading-surfer surveying their charts. The weakly electric fish, Eigenmannia, emits an electric signal as a sort of radar to find objects in its surroundings. The problem arises when another Eigenmannia is nearby, sending out a signal at a frequency near the first fish's signal. This results in a "beat" frequency equal to the difference of the frequency of the two signals, composed of amplitude and phase modulations. Much like the market, when the agendas of different market participants collide, the result is confusion and little information for anyone. The fish responds by moving the frequency of its signal away from the other, a process known as the Jamming Avoidance Response. The fish doesn't know if it is higher or lower, and has to solve the problem based on how receptors spaced over its body are receiving the phase information of the two signals. In essence, each receptor "votes" on whether it perceives the signal to be leading the other, i.e., it's at a higher frequency, or lagging, i.e., a lower frequency. Any one neuron may be wrong, but in the aggregate, the animal arrives at the correct conclusion. In classic research, the late Walter Heiligenberg termed this organization a "neuronal democracy".

As traders, individual neurons awash in the market's oscillations, we are faced with the same problem. Are we leading? Are we lagging? It may come as little comfort that the market will eventually get it right, even if we are wrong.

GM Nigel Davies offers:

In chess this would be quite a typical scenario. Often when you inflict some kind of permanent damage (structural or material), there is a temporary release of energy from the other side's pieces. The 'trick' is to balance the gains against the likely reaction, and this is also necessary. To improve a position you often have to allow some temporary (hopefully) counter play, kind of like a wrestler letting go of an opponent temporarily so as to get a better grip.

Dr. Michael Cook adds:

Gary comments that market gyrations are "nothing like a physical, earthly swing" because there are two forces involved. How about the case of a damped oscillation, which has physical analogues? Using this analogy, momentum investors are "damped" by the "restoring force" supplied by value investors.

And what happened in the bubble was the disappearance of effective value investors, which led to an un-damped oscillation, which, when driven at the appropriate frequency, leads to wider and wider oscillations which no physical -- or financial -- system can sustain.

The collapse of the Tacoma Narrow Bridge is the canonical example, and here is an illustration of the math behind the phenomenon.

Rick Foust contributes:

Imagine a ball rolling down a slight incline that has a crown in the middle and rails on the sides, similar to a highway with guard rails. The ball seeks the nearest rail, bounces repeatedly and eventually stays on the rail as it continuous forward.

Now imagine that the roadway has an irregular surface and rough rails. The ball will once again seek a rail. But this time, it will do so in a careening fashion that depends on the roadway surface. As it encounters a rail, it will briefly run down the rail, bouncing as it goes, until it eventually hits a point of roughness large enough to kick it to the other side. The amount of roughness required to cause a change in state depends on the slope of the underlying surface.

In the market, the rails are accumulations of large and small limit orders. Rail roughness is created by variations in order size and position. The roadway surface is formed by underlying market orders that create a natural drift. The roadway surface may undulate in a rhythmic fashion, similar to the Tacoma bridge, if market participant psychology is undecided. Or it may consistently lean in one direction if there is a prevailing sentiment.

At some point, limit orders at one rail or the other are exhausted, pulled or merely absent. At that point, the ball is free to discover the location of other rails. Stops are now run, creating new market orders. New participants are drawn in. If the new rails encountered are small and scattered, the ball will plow through them and may even gain momentum until it eventually encounters a rail large enough to stop it. Until this rail is reached, the underlying roadway slope will likely increase as sentiment is self-reinforced.

28-Nov-2006

A Wealth of Experience for New Speculators? from

Greg Rehmke

I thought there were a couple interesting aspects of Steve Leslie's Nov. 22nd post. He concludes: "Success in poker is like success in life. It is attainable but not easy and it requires lots of work. That is why so few attain it." Yet if everyone, or a significant number, were to follow professional advice, the quality of poker play could jump nationwide without any change in levels of success (though perhaps many would gain by feeling less stupid about losing, since bad luck rather than bad play would be responsible).

Similarly with sports. Every NBA or NFL team could raise their quality of play 20% with no change in levels of success.

Except in international competition. NBA teams and players, as well as gamblers, might do better in world competition following a popular U.S. book, lecture tour, or movie that somehow inspires competitors to higher quality play.

Unlike gambling and sports, which are zero-sum games, (apart from the mental or physical pleasure gained through competing), investing is a positive-sum game. Higher quality investing directs funds to higher quality projects. Insight into foolish corporate or commodity projects and positions, provides both returns to winners and instruction to losers. Losers don't just lose pots or games, if left alone they continue to misdirect and waste capital and labor resources. "Capital" belongs to people and "labor resources" are people. Misdirecting them wastes the time and money of people in production, and deprives consumers of goods and services that could have been produced with better "play" by investors (assisted by speculators).

The question arises whether there might be a similar difference in the quality of play across cultures. If the game is basketball, U.S. beats China. If the game is ping pong, China beats U.S. (for now, at least). I don't know how good the Chinese are at poker, though I hear gambling is very popular. As hundreds of millions of everyday Chinese gain enough wealth for everyday gambling, there will be some thousands or tens of thousands wealthy enough for big-time gambling as well as big-time investing and speculating.

As these newly minted big-time speculators jump into the game, will they make systematic "newby" mistakes? I don't know enough about Chinese culture to know what to expect. But with commodity prices jumping up and down in front of tens of millions of gambling-prone newly capable investors what might we expect? (Plus, thousands of local government officials seem able to gamble and speculate illegally with local bond revenue.) Markets will draw in an influx of low-skill, limited-experience players, flush with success from one culture and range-of-experience (wealthy Chinese manufacturers), trying their hand with commodity speculation.

28-Nov-2006

A Piece on Milton Friedman, sent in by

Susan Niederhoffer

The following is from Gary Becker and Richard Posners' Blog. It is a piece by Becker on Milton Friedman, who sadly passed away this month. [Read the NYTimes Obituary]

I will not dwell here on what a remarkable colleague he was. However, I do want to describe my first exposure to him as a teacher since he enormously changed my approach to economics, and to life itself. After my first class with him a half-century ago, I recognized that I was fortunate to have an extraordinary economist as a teacher. During that class he asked a question, and I shot up my hand and was called on to provide an answer. I still remember what he said, "That is no answer, for you are only restating the question in other words." I sat down humiliated, but I knew he was right. I decided on my way home after a very stimulating class that despite all the economics I had studied at Princeton, and the two economics articles I was in the process of publishing, I had to relearn economics from the ground up. I sat at Friedman's feet for the next six years-- three as an Assistant Professor at Chicago-- learning economics from a fresh perspective. It was the most exciting intellectual period of my life. Further reflections on Friedman as a teacher can be found in my essay on him in the collection edited by Edward Shils, Remembering the University of Chicago: Teachers, Scientists, and Scholars, 1991, University of Chicago Press......

To conclude on a more personal level, I was most impressed by Milton Friedman's sterling character--he would never soften his views to curry favor--his perennial optimism, his loyalty to those he liked, his love of a good argument without any personal attacks on his opponents, and his courage in the face of prolonged and virulent attacks on him by others. I cannot count the number of times I participated with him in seminars, nor how many visits my wife and I shared with Milton and Rose, his wife of almost 70 years. Rose, a fine economist, would not hesitate to differ with her husband when she believed his arguments were wrong or too loose. When I spoke on the phone with him last Monday, he sounded strong and a bit optimistic about his health, even though he had just returned from a one-week hospital stay with a severe illness, an illness that a few days later took his life. Although his ideas live on stronger than ever, it is hard to believe that he is not here. I can no longer seek his opinions on my papers, but I will continue to ask myself about any ideas I have: would my teacher and dear friend Milton Friedman believe they are any good?

Steve Wisdom adds:

I also like these vignettes from Ben Stein:

When I was a Columbia undergrad in the early '60s, Friedman taught there for a year and was a good friend to me. He even used applied statistics to save me from romantic desperation when I was worried about replacing a girlfriend. If there were only one right woman for every right man, he advised, they would never find each other. Another time, he stopped me from crossing against the light on Broadway and 116th Street, telling me, "Why risk your whole life to save 10 seconds?"

28-Nov-2006

Bernanke: Profits or Prices?, from

George Zachar

There was a nice overview of Bernanke's current thinking on the economy in today's speech. There were No bombshells, with both the rhetoric and the conclusions between the 40 yard lines of recent Fedspeak and Centralbankese.

One passage struck me as being modestly noteworthy:

What implications does the pickup in labor costs have for price inflation? One possible outcome is that increases in labor costs will largely be absorbed by a narrowing of firms' profit margins and not be passed on to consumers in the form of higher prices. The fact that the average markup of prices over unit labor costs is currently high by historical standards suggests some scope for this outcome to occur. If higher labor costs are mostly absorbed by firms and not passed on, then workers will see the gains in their nominal compensation per hour of work translated into greater real compensation per hour; in the process, workers would capture a greater share of the fruits of the high rate of productivity growth seen in recent years. The more worrisome possibility is that tight product markets might allow firms to pass all or part of their higher labor costs through to prices, adding to inflation pressures. The data on costs, margins, and prices in coming months may shed some light on which of these two scenarios is likely to be the better description of events.

Bernanke echoes his predecessor in calling attention to the rise in profit margins, and implying it is business' slicing of the wage/profit pie that is central to inflation pressures. This plays perfectly in the rhetorical framework of the labor union-backed Democrats who will be holding the gavels on Capitol Hill.

28-Nov-2006

(Anecdotal) Updated Macro Information, from

Dr. William Rafter

I find that at this time there is no evidence from the Monetary Base numbers suggesting a change in policy. Additionally there is no change in the job growth numbers as evidenced by the payroll tax receipts.

George Zachar adds:

This morning William Poole observed that the MZM and M2 monetary aggregates "are chugging along at pretty steady rates." Year over year, he noted, MZM is up 4.3%, while M2 is up 4.9%.

Although they have accelerated in more recent months, Poole said those money supply growth rates "are pretty close to the growth rate we've got for nominal GDP" and are "consistent with the growth that's being forecast for next year."

Since real GDP growth is expected to be "a little below 3%," he said, "if you take a 2% inflation target that adds up to 4 1/2% to 5%, which is really very close to where money growth is right now." So he said, "money growth is not telling you that monetary policy is tight or easy, just in line with GDP growth.

Bill replies:

If you think of the Monetary Base as a window on Fed policy, then the data makes the case that there has been no change in policy. Since the beginning of 2005 that policy has been moving from accommodative to restrictive. Thus there is no deviation from a restrictive policy, which at this time is very restrictive (more below).

George Zachar's comment was more insightful. George pointed out how the Fed's statements on M2 and MZM growth were contradicted by my data. The boys at the Fed think that they are walking the narrow line between restrictive and accommodative. The data suggests otherwise.

At this time the Monetary Base is in excess of 4 percent below the long-term mathematical fit of that data. This is more restrictive than in 1998. Perhaps our "planners" wanted to be more restrictive in 1998, but had to back off because of (a) Asian contagion, (b), Russian bond default and (c) Long Term Capital Management. In any case, the current data shows the present to be more restrictive, and there is no anxious moment to force a change. The period of 1990-92 had the most restrictive policy. Remember that as the period of "It's the economy, stupid".

Monetary Base is an interesting number, consisting of currency and deposits at Federal Reserve Banks. Breaking the Base down into those two components does not give you as complete a picture as the two together. For example, look at the two spikes: the earlier one was the Y2K spike caused by excess currency (the ATMs were all going to fail). The later spike (9-11) was caused by the Fed goosing the bank reserves. Only if you look at the Base data do you see both spikes.

I'm looking forward to Diebold next week.

28-Nov-2006

Read our Movies Page, with new reviews from Scott Brooks and Marion Dreyfus

28-Nov-2006

An Alternative Use For Canes, from Arthur Cooper

Monday's Barron's (p 32) describes the efforts of a collector to donate her collection of over 1,000 walking sticks (some dating back to the 1500s) to charity. If you can't use them for investing, you may as well get a tax deduction for them.

28-Nov-2006

FNMA Delinquency Rates, from George Zachar

This table is the latest FNMA delinquency data ... contra popular doom, it shows a declining loan problem.

27-Nov-2006

100 Largest Declines, by Victor Niederhoffer

Below is the distribution of months between the chronological record of the 100 largest declines in S&P futures from January '01 to date. Starting with the January 2, 2001 decline of 27.1 points and ending with today's, decline of 19.3 points, they range in size from a 57.0 point decline on 9/19/2001 to a 17.3 point decline on 8/28/2001.

| Months Between Consecutive Declines in Top 100 | |

| Number of Months | Number of Observations |

| 0 | 61 |

| 1 | 28 |

| 2 | 03 |

| 3 | 03 |

| 4 | 02 |

| 6 | 01 |

| 14 | 01 |

The average duration between each of the top 100 declines was 1.5 months. A time series of the durations between consecutive large declines however shows that the average duration between them was 1/3 of a month in 2001, 1/4 of a month in 2002, 1 month in 2003, 1 and 3/4 months in 2004 , 14 months in 2005, and 2 months in 2006.

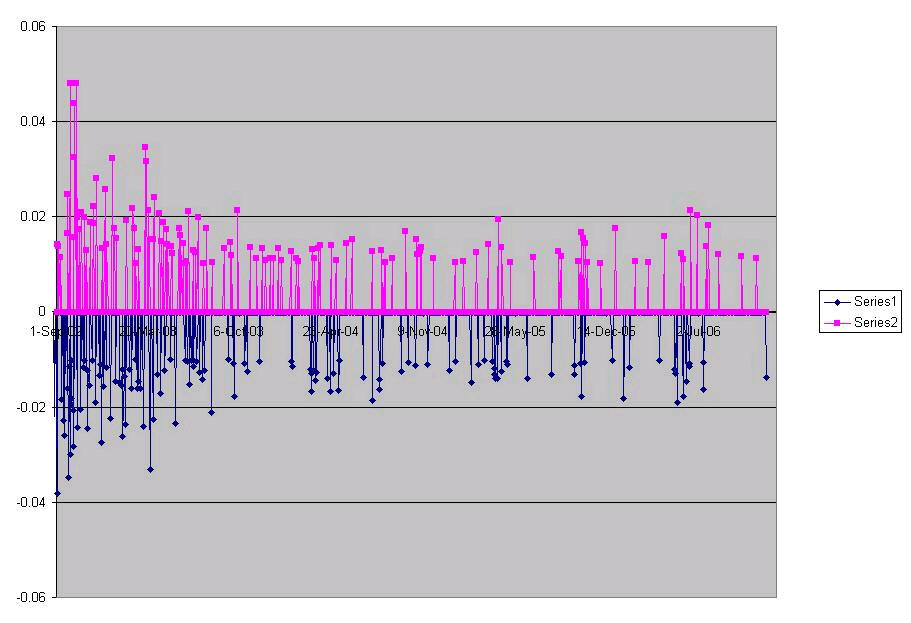

Kim Zussman adds:

The attached graph is a plot of big daily moves of SPY since January 2003 (up or down more than 1%) by date. Since late 2003, big daily moves look to be less frequent, as well as smaller, which fits with the secular decline in volatility. The frequency change is shown by counting moves per year:

| Year | Down | Up | Up/Down |

| 2006 | 13 | 13 | 1 |

| 2005 | 21 | 16 | 0.76 |

| 2004 | 22 | 23 | 1.05 |

| 2003 | 38 | 42 | 1.11 |

The ratio of up/down is 1 or more for all years, except for 2005 (Which fits with other studies suggesting interval-returns scale contemporaneously to count down days).

Another observation is that yesterday's decline is the first in a while, whereas big advances have been more evenly spaced. In fact when ranking gaps between big declines, yesterday's was the longest hiatus dolor of any since January 2003.

27-Nov-2006

An Ongoing Thread Entitled Greed and Healthcare

27-Nov-2006

Some Thoughts on December, by Victor Niederhoffer

The biggest decline during this stretch came in 2002 with a 7% decline, which had been

preceded by a 20% decline over the previous 11 months, and the next biggest decline was of 4%

coming in 1980, following a 30% rise over the preceding 11 months. The biggest rise came in 1991

which was 11%, and followed a 10% rise over the preceding 11 months. The second

biggest rise of 6% came in 1987, which was preceded by a big decline of 4% in the

preceding 11 months. Thus, big declines come after big rises and big declines,

and big rises came after big rises and big declines -- in aggregate there is

certainly not a linear relationship. All one can say about the extent to which this is non-random is that

about half the moves were approximately 1% rises, and there were a

few outliers that followed enormous rises and declines from the preceding 11

months.

The biggest decline during this stretch came in 2002 with a 7% decline, which had been

preceded by a 20% decline over the previous 11 months, and the next biggest decline was of 4%

coming in 1980, following a 30% rise over the preceding 11 months. The biggest rise came in 1991

which was 11%, and followed a 10% rise over the preceding 11 months. The second

biggest rise of 6% came in 1987, which was preceded by a big decline of 4% in the

preceding 11 months. Thus, big declines come after big rises and big declines,

and big rises came after big rises and big declines -- in aggregate there is

certainly not a linear relationship. All one can say about the extent to which this is non-random is that

about half the moves were approximately 1% rises, and there were a

few outliers that followed enormous rises and declines from the preceding 11

months.| Year | Adjusted Futures Move for first 11 Months (%) | Adjusted Futures Move in December (%) | Start of Year S&P Index |

| 1980 | 30 | -04 | 108 |

| 1981 | -09 | -03 | 136 |

| 1982 | 13 | 01 | 122 |

| 1983 | 15 | -01 | 141 |

| 1984 | -03 | 01 | 165 |

| 1985 | 20 | 05 | 167 |

| 1986 | 20 | -03 | 211 |

| 1987 | -04 | 06 | 242 |

| 1988 | 10 | 01 | 247 |

| 1989 | 25 | 01 | 278 |

| 1990 | -10 | 01 | 354 |

| 1991 | 08 | 10 | 330 |

| 1992 | 03 | 01 | 417 |

| 1993 | 08 | 01 | 435 |

| 1994 | -02 | 01 | 466 |

| 1995 | 30 | 01 | 459 |

| 1996 | 25 | -02 | 616 |

| 1997 | 25 | 01 | 741 |

| 1998 | 15 | 05 | 971 |

| 1999 | 12 | 04 | 1229 |

| 2000 | -10 | 03 | 1469 |

| 2001 | -15 | 01 | 1320 |

| 2002 | -20 | -07 | 1148 |

| 2003 | 15 | 04 | 880 |

| 2004 | 06 | 03 | 1112 |

| 2005 | 05 | -0.5 | 1211 |

| 2006 | 09 | 1248 |

Dr. Kim Zussman adds:

Looking further at the same monthly data, December moves seem large compared to the prior 11 months. To check this (and eliminate effects of sign), for each year I looked at the ratio of absolute values:

|Dec ret|/|J-N ret|

One would expect each month to contribute something like 1/11 of the return of the prior 11 months. But Decembers are larger, as shown by the data:

| Year | Jan-Nov | Dec | |Dec|/|j-n| |

| 2005 | 0.031 | -0.001 | 0.031 |

| 2004 | 0.056 | 0.032 | 0.583 |

| 2003 | 0.203 | 0.051 | 0.250 |

| 2002 | -0.184 | -0.060 | 0.327 |

| 2001 | -0.137 | 0.008 | 0.055 |

| 2000 | -0.105 | 0.004 | 0.039 |

| 1999 | 0.130 | 0.058 | 0.445 |

| 1998 | 0.199 | 0.056 | 0.283 |

| 1997 | 0.290 | 0.016 | 0.054 |

| 1996 | 0.229 | -0.022 | 0.094 |

| 1995 | 0.318 | 0.017 | 0.055 |

| 1994 | -0.027 | 0.012 | 0.450 |

| 1993 | 0.060 | 0.010 | 0.169 |

| 1992 | 0.034 | 0.010 | 0.296 |

| 1991 | 0.136 | 0.112 | 0.819 |

| 1990 | -0.088 | 0.025 | 0.281 |

| 1989 | 0.246 | 0.021 | 0.087 |

| 1988 | 0.108 | 0.015 | 0.136 |

| 1987 | -0.049 | 0.073 | 1.487 |

| 1986 | 0.180 | -0.028 | 0.158 |

| 1985 | 0.209 | 0.045 | 0.216 |

| 1984 | -0.008 | 0.022 | 2.733 |

| 1983 | 0.183 | -0.009 | 0.048 |

| 1982 | 0.130 | 0.015 | 0.117 |

| 1981 | -0.069 | -0.030 | 0.434 |

| 1980 | 0.035 | -0.034 | 0.966 |

The attached plot depicts |Dec|/|J-N| vs. date, and though variability in this fraction has damped out over time, it still seems high. Even discarding two out-lying years of '83 and '87, the mean ratio is 0.26; almost 3 times 1/11.

Rick Foust comments:

I suppose that there are two major factors (amongst other smaller ones) that cause the December effect.

The first is money flowing into IRAs prior to the end of the year. Someone on the retail side of the business could confirm or refute this.

The second is large fund rebalancing. Some funds operate on the basis of maintaining a fixed ratio in various asset classes (percent stocks to percent bonds...). Periodic rebalancing of the ratios forces them to buy the asset class that has done poorly and sell the asset class that has done well. It seems that rebalancing predominantly takes place towards the end of the year. Surely there is someone here that could confirm or refute this.

Scott Brooks offers:

IRA fund flow is bigger towards the end of March thru about April 20th or so than it is in December (I say April 20th because the envelope the IRA deposit check is mailed in need only be post marked April 15th).

One can also look at index reconstitution as issues are dropped and others added to the indexes. However, this has the greatest effect on the smaller issues (smaller in terms of cap weighting). Most larger capitalized stocks are going to stay in the index and could be bought in an effort to rebalance a portfolio fund back into the index weighting.

As a result, the index funds have to go thru a flurry of rebalancing, selling the issues dropped from the index and buying those that are added....and proportionalizing those stocks that stick (again, mainly the largest capitalized issues).

Something else to consider (for both money managers and individuals) ...

Stocks that have a loss are often sold to realize capital losses to offset the fact that ...

Stocks that managers or individuals feel have run their course and have a gain are sold.

Another phenomenon that occurs are RMD's (Required Minimum Distributions) for those with qualified money that are over 70. This is a forced sale for no other reason than realizing taxable income. What's interesting is that this now becomes money in motion and as a result, opportunity to invest in other areas. As the baby boomers age, this will become more and more of a factor ... especially since such a large number of boomers bought into the myth that they will retire in a lower tax bracket than when they were working.

I'm sure there are are many other reasons that our resident bond mavens and options experts (as well as anyone smarter about the market than I) could add to this discussion

An Anonymous Contributor says:

In his post Kim Zussman wrote that:

Looking further at the same monthly data, December moves seem large compared to the prior 11 months. To check this (and eliminate effects of sign), for each year I looked at the ratio of absolute values:

|Dec ret|/|J-N ret|

One would expect each month to contribute something like 1/11 of the return of the prior 11 months.

No, one wouldn't. Since you already have all the data, go ahead and look at every month relative to the other eleven months of the same year (or to the preceding eleven months, it won't make much of a difference). My own back-of-the-envelope calculations with unadjusted data show a mean of about .22 over all months, with December being somewhat below average.

27-Nov-2006

Give thanks for Pilgrims -- and McDonald's, by Victor Niederhoffer and Laurel Kenner

Thanksgiving is about sharing prosperity, and it's a good time to think about where prosperity comes from. The Pilgrims figured it out in 1623. We'll retell that story as we celebrate the way it lives on in countless U.S. families and companies today. And in particular at one company, McDonald's (MCD, news, msgs), that in its humdrum way beautifully demonstrates the source of prosperity and the American way of life.

The Pilgrims started with so little. They had to hide in England because the authorities considered them dangerous. They fled to Holland but found themselves compelled to take menial jobs. On the way to America, many of the company died. They lost their way to Virginia and landed in Massachusetts just as winter set in. The Virginia Co., their backers in London, went bankrupt and couldn't send relief supplies.

To cope with want, the Pilgrims made the same mistake that so many countries do even today: They divided all their land, efforts, supplies and produce in common, to each according to his need.

As always in such systems, need surpassed supply.

The Pilgrims spent their first three years in America suffering from hunger, illness, cold and infighting. People stole from the common stores "despite being well whipped," according to William Bradford's "Of Plymouth Plantation."

Bradford, governor of Plymouth Colony, records what happened next: "They began to think how they might raise as much corn as they could, that they might not continue to languish in misery. After much debate, the Governor decided that each settler should plant corn for themselves."

Under the Land Division of 1623, each family received one acre per family member to farm. That year, three times as many acres were planted as the year before. Prosperity was not long in coming.

The Pilgrims turned from their Old World system of common ownership to incentives. They didn't go that way out of ideological conviction, but because they didn't have the luxury of waiting for support to come to them.

How many families in America tell the same tale? "When we came here, we worked hard and our lives were better."

But that wasn't the end of the story. Before the switch to incentives, the hungry settlers were at each other's throats. Hard workers resented receiving the same portions of food as those who were not able to do even a quarter of the work they did. Young men resented having to work without compensation to feed other men's wives and children. Mature men resented receiving the same allotments as did the younger and meaner sort. Women resented being forced to do laundry and other chores for men other than their husbands. Many people felt too sick to work.

But when they were allowed to farm their own plots, the most amazing thing happened. Everybody -- the sick, the women and even the children -- went out willingly into the fields to work. People started to respect and like one another again.

It wasn't that they were bad people, Bradford explained; it's just human nature. Adam Smith came to the same conclusion later, and Friedrich Hayek updated Smith's ideas for the 20th century. But we don't need to go back to New England for understanding. Similar outcomes can be seen at McDonald's every day.

For centuries, people on the lower rungs of the social ladder weren't able to eat meat. They ate grains and beans. But people like beef. And chicken.

When McDonald's started popping up in every neighborhood, all of a sudden there was an affordable place for families to eat. Previously, one of the main differences between the upper and lower classes was that the rich could eat out. Even if the poor could afford the tab, they couldn't hire baby sitters, and they couldn't bring their kids to the elegant establishments designed for the rich because they would have disturbed the other diners.

Most kids don't like fancy restaurants anyway. They want fries, not polenta with wild mushrooms. They want fried codfish, not turbot. They want burgers, not lamb chops.

How many people has McDonald's made happy? How many families has it brought together? How many Happy Meals have been eaten there? How many kids have enjoyed the playgrounds? How many tired workers have been able to catch a quick meal? How many women are able to pursue careers and other productive activities and dreams because McDonald's has freed them from the task of having to cook every night?

The Pilgrims might have served 200 or 300 American Indians at their Thanksgiving feast. McDonald's serves 26 million customers a day at 13,700 U.S. restaurants.

For the traveler, McDonald's is a home away from home, offering so much for so little. The restrooms are clean. And McDonald's serves hot strong organic coffee in smooth cups of some wonderful material that keeps liquids hot without burning the hand, shaped to fit into the cup holders that just happen to be in your car, with carefully designed tops that permit just the right amount to be sipped.

No regulator, no fascist dictator, no socialist planner decreed sip tops or cup holders. But how many late-night drivers have died for the lack of a good cup of coffee? What could be more munificent than saving lives?

And the story doesn't end there. Consider the employees of McDonald's. How many people have worked there and learned the most important lesson in America: The customer is always right?

The anti-this-and-that people who demonstrate against profit incentives and free markets like to single out McDonald's as a symbol of modern capitalism. (They don't mean that in a nice way.) As the McLibel Support Campaign puts it: "(McDonald's) has pioneered many business practices that have been taken up by others, and have come to represent a symbol of the way that society is going --'McDonaldization.'"

But when have you ever seen an unhappy customer at McDonald's? There couldn't be too many of them, because about 10% of America eats there each day. Given the choice of cooking at home or going to other restaurants -- and competition ensures that there are other restaurants -- people go to McDonald's because they trust they'll find good food, quick service and value for money. What could be more munificent, more representative of sharing the fruits of hard work than McDonald's?

McDonald's and the Pilgrims are the essence of America. The people work hard, motivated by the chance for profits. They provide a welcome to others, whether to Indians joining in harvest celebrations, or to customers looking to satisfy their hunger. Their work results in high quality, low costs and family togetherness.

Those humdrum, everyday attributes are what makes America great. That's what we should be celebrating. It's the source of all our munificence, from the first Thanksgiving to today.

27-Nov-2006

Thank the Pilgrims for eBay, by Victor Niederhoffer and Laurel Kenner

The story of the Pilgrims' first years in America shows how a change from common ownership to private property led to the feasting celebrated today at Thanksgiving. Similar tales of expanding harvests and benevolence are told wherever people can keep the fruits of their labor and trade them as they please.

The story illuminates why eBay and Chicago Mercantile Exchange Holdings, the owner of the Chicago Mercantile Exchange, were among the two best-performing stocks in their class during each of the last two years, and it provides a useful signal that other markets now preparing to go public might be good investments.

After landing at Plymouth in November 1620, the Pilgrims endured a cold, hungry winter during which half of them died. Promised supplies failed to arrive from London. The 1621 harvest wasn't as big as hoped, nor was the 1622 harvest. More famine seemed inevitable.

And then the colony began to talk through the problem. The London merchants who financed the Pilgrims' settlement specified "that all such persons as are of this colony are to have their meat, drink, apparel, and all provisions out of the common stock and goods of the said colony." In 1621, the Pilgrims planted 26 acres, according to Judd W. Patton, an economics professor at Bellevue University in Nebraska. In 1622, they planted 60 acres, but that wasn't enough to keep hunger away.

People began to steal by night and day, "although many were well whipped," Gov. William Bradford reported.

The system made no sense to anyone. The hard-working subsidized the slackers. The young and ambitious didn't want to do work for anyone else and get nothing for their trouble. The wives of some of the men objected to be commanded to wash clothes, dress meat or do other tasks for other men.

As Bradford would later write in "Of Plymouth Plantation 1620-1647," "At length, after much debate of things, the Governor (with the advice of the chiefest amongst them) gave way that they should set corn every man for his own particular, and in that regard trust to themselves, in all other things to go on in the general way as before."

In what's known today as the Land Division of 1623, each family was allotted land at the rate of one acre per family member and told to go out and produce. More than 184 acres were planted that year. And, Bradford reported, "This had very good success, for it made all hands very industrious, so as much more corn was planted than otherwise would have been by any means the Governor or any other could use, and saved him a great deal of trouble, and gave far better content. The women now went willingly into the field, and took their little ones with them to set corn."

What is apparent from this history is what we all know from our experience: When you can benefit from working hard, you work harder. Under the system of common ownership, there was stealing, shirking and malevolence. Under the incentive system, there was good feeling, hard work and benevolence.

News of the success at Plymouth and other settlements like it attracted more and more immigrants to the New World. And everyone who lives in America today has a personal story that is part of that great continuing tale.

The impulse to improve one's conditions through greater effort and trade is as natural as breathing, and this has been so since the beginning. New York University economist Haim Ofek, in "Second Nature: Economics Origins of Human Evolution, argues that trade helped spur the growth of the brain.

"Exchange requires certain levels of dexterity in communication, quantification, abstraction, and orientation in time and space, all of which depend on the lingual, mathematical and even artistic faculties of the human mind," Ofek writes in the introduction to his 2001 book. "Exchange, therefore, is a pervasive human predisposition with obvious evolutionary implications."

Relatively flexible and acute people had an edge in trading. They survived and prospered, they had bigger, healthier families, and their descendants became dominant.

The success of eBay since its founding in 1995 shares many similarities with the Pilgrim story. Now a public company with a market value of around $75 billion, eBay has created an electronic network of niche markets that takes account of the infinity of human tastes and aptitudes and specializations. The stock is up 72-fold since its September 1998 IPO, from a price-adjusted initial price of $1.50 to $109.42 as of Nov. 15. That is after a 77% drop in the tech crash of 2000.

Like the Pilgrims, eBay gives each of its sellers a piece of land (though in virtual space) to carry out his or her business. A spirit of benevolence is apparent in the company's feedback system; in almost half the transactions, both buyer and seller rate each other, with almost all them highly favorable. But to us, there is one overriding reason for eBay's success: It unleashes the desire and provides a forum for buyers and sellers to improve themselves by trade in a million ways every day.

The CME, odd as it sounds, also bears some similarities to Plymouth Colony. Founded in 1897 as a member-owned organization, the Merc started out as a market for the trading of foodstuffs. Its activities and goals were torn between the interests of the members and the interests of the public. A low point was reached in 1989, when a widely publicized sting operation uncovered conflicts of interest and failures to give the public a fair shake.

For years, the Merc had been content to play a sleepy second fiddle to the Chicago Board of Trade both in volume and number of products traded. In 1972, an inspirational governor -- in this case, Leo Melamed -- decided it was in everyone's interest to match members' interests with the growing public interest in financial products such as currencies, Treasury bills, Eurodollars and stock market futures. Growth exploded in 2000 as the CME prepared for the shift to public ownership by converting members' interests to shares. Since the Merc went public in December 2002 with its shares listed on the New York Stock Exchange, the stock has risen nearly six-fold, and it has stayed in the top 10 of NYSE performers.

In effect, the CME transformed itself from a tradition-bound club with the image of a raucous den where men shouted at each other to get an edge on the public in trading pork bellies. Instead, it became a pioneering company that lets hardly a week go by without introducing a new electronic product designed to give the public more ability to improve and hedge their ownership of stocks and debt.

The table below shows how acreage planted and revenues grew at Plymouth, the CME and eBay.

| The Plymouth, Chicago Merc and eBay experiences | |||

| Year | Plymouth acres planted | CME revenue* | eBay revenue* | (1621/2000) | 26 | $226.6 | $431.4 |

| (1622/2001) | 60 | $387.2 | $749.8 |

| (1623/2002) | 184 | $453.2 | $1,214.1 |

| (2003) | $526.1 | $2,165 | |

| (2004)** | $743.8 | $3,260 | |

| * In millions **Analysts' estimates | |||

The Pilgrims originally agreed with the London merchants who financed their settlement to hold their land and its products in common, a sort of forced socialism, much as the communists imposed on Russia after the 1917 revolution.