Archives

Write to us at:

![]() (not clickable).

(not clickable).

Please include your full name, and omit attachments.

|

Daily Speculations |

|

|

| |

Archives

Write to us at:

|

December 1-13, 2005

12/13/2005

Heel and Toe, from George Zachar

Keeping its foot on the brake, but lifting its heel ever so slightly, the Fed artfully teases that the end of the rate hike process just might be on the horizon: "some further measured policy firming is likely to be needed." But my focus is here: "possible increases in resource utilization as well as elevated energy prices have the potential to add to inflation pressures." So series like unemployment and capacity utilization will now be viewed as (potential) leading indicators of inflation, and deconstructed with an eye toward forecasting price pressure.

12/13/2005

Posts on India and Nepal in Our New Section

Notes from Abroad

12/13/2005

Bear Corner: The Latest from the Senior Weekly Financial Columnist

A perspicacious spec sent a trenchant post today about an easily refuted lie, and it set me off on a tangent. The weekly financial columnist, in his Monday, Dec. 12 piece, has a beautiful example of a perfect lie, one that is impossible to refute but that serves to enhance the believability of related self-serving inexactitudes in the rest of the corpus.

After going into the usual 25 reasons that he is bearish for 2006, which we have chronicled often and systematized in Practical Speculations,* he states that he is not always a perfect forecaster of the market. This is like saying that Christian Guzman of the SS Nationals, generally regarded as the worst player in Major League Baseball, with a batting average of .219, does not always get on base.

The columnist says the reason he's not a great forecaster is that he still believes in things like sales, earnings and book value. This is true, of course, but what he doesn't say is that he has been consistently bearish for 40 years. Indeed, Collab was unable to find one counterexample, though she performed a content analysis on all of his columns from 1990 to 2002, and read almost all of the others. The columnist became bearish circa Dow 600 in 1964 and has consistently been trotting out these same 25 reasons, "an excess of enthusiasm" or "lack of a true selling climax," ever since.

As I was chuckling over his latest, Collab said to me, "What about his venerable and savvy friend who's very bearish now?" Sure enough, next in the column was a technical analyst whose record has been brilliant. He caught the entire Japanese rally, but frankly is not so bullish on it now. He sees a major technical catastrophe shaping up in the market for 2006 but sees a buying opportunity on any significant break. The friend is given anonymity, as is appropriate, for to be joined with a personage such as the financial weekly columnist, who perhaps has the worst record of forecasting in history, why, that would be tantamount to professional opprobrium.

However, to finish up the perfect deflection, the financial weekly columnist lets you know that he agrees with his venerable friend completely.

*A disturbingly unanimous expectation among professional forecasters for 4% GDP growth next year; the possible dark consequences of an end to the housing boom; a bleak prediction by the UCLA Anderson Forecast; Detroit's woes; the federal deficit; inflation that "continues to rear its insidious head"; high energy costs; high gold prices that "likely bode ill for the economy."12/13/2005

A Perspicacious Spec Reads the Newspaper, a Continuing Feature

Cl#nton on Stronach: I never advised that woman

By The Canadian Press

MONTREAL � Former president Bill Cl#nton says he was just as surprised as everyone else when former Conservative MP Belinda Stronach defected to the Liberals last spring. Cl#nton, a friend of Stronach�s, says he had no prior knowledge of her stunning decision last May, which helped the governing Liberals barely survive a non-confidence vote. He says he had nothing to do with her decision, though he later concluded she had a "principled reason" for doing it.

What struck me about this piece was the unnecessary lie at the end, where Cigarman said Stronach jumped parties for "principled" reasons. Even the dimmest political bulb knows she switched for only one reason: a ministerial post in return for her tipping-point vote to keep the uber-corrupt Liberals in power. Cigarman could have plausibly denied talking to her ahead of time, but why throw in the gratuitous falsehood?

12/12/2005

Ephemera, by Victor Niederhoffer

Today's rise in the Nikkei to the 16,000 area, a five-year high, emphasizes again that ephemeral and predictable factors that cause declines are great buying opportunities. The ephemeral factor in the Nikkei was the fat-fingered trader at Mizuho Securities who sold 41 times too many shares of the IPO J-Com Co. But one might have predicted that the decline would be temporary, because the loss was part of a zero sum game. Also, fat fingers were a predictable tendency of many fingers, and the fact that it occurred was a realization of a known probabilistic phenomenon.

Larry Harris gives, as an example of an ephemeral phenomenon, the undue rise in Occidental Petroleum following the death of Armand Hammer, which led everyone to think that now the company would be run better. But his death was anticipated once he hit 90, and it shouldn't have caused such a reaction. Harris notes the stock fell the next day.

Recently, Jon Markman predicted that the decline in stocks in early October in conjunction with the R#fco crisis would be reversed imminently, and it was. A notable sidelight during that period has been the astonishingly high coterminous correlation between the daily returns of R#fco and the general market, approximately 30% during the heat of the fray. If only one knew where R#fco was going to close during that period, even though it traded at less than $1.20 a share the whole time with a market value of less than 150 million, one would have had the open sesame to the whole market.

Another example was the supply situation of British Petroleum during the October 1987 crisis. Every nuance of the situation caused ebullience of distress in the US markets. After all, the white shoe brokerages might lose more money if they were called on to make good on their commitments.

The Long-Term Capital collapse and the Barings debacle were other examples of ephemera where the market cratered for weeks before the announcement on the rumors and not one legitimate buyer surfaced until all the supply was requited. Of course, in both situations, indeed in all such situations, the situation was exacerbated by interested parties with inside information of the coming surplus of supply who front-ran the actual selling, thereby precipitating and exacerbating the decline. Many such organisms specialize in such activities in all major biota systems, and despite the useful redistribution function served by such detritovores as vultures, worms, maggots and bacteria, and their counterparts in the markets, I look upon them with a certain revulsion.

The general question remains how to quantify ephemera on a prospective basis and know when they've caused a temporary market decline or rise (in those without a positive drift), and take advantage of it with reasonable sangfroid?

In researching ephemera I find myself in strange company, as almost all the 82,000 entries for "ephemera" "stock market" on Google are to very bearish commentators who state that any market rise is due to ephemeral factors. Another strange phenomenon is that almost all the "ephemera" labels were from very old articles. For instance, my friend Charlie Minter wrote on the "ephemeral" nature of the P/E ratio, and how it's much too high, in 2003, circa S&P 950, decrying the predictive properties of the Fed Model, as is common among practitioners and academics.

Shui Mitsuda adds:

This is a breakdown of the Mizuho disaster.

A Human resource service company "J-com" went to public listing on 8th Dec.

Mizuho Security (subsidiary of Mizuho bank) receives a SELL order from a customer:

SELL 1 SHARE of J-com @ 610,000 YEN

and then disaster happens the Mizuho operator keyed in:

SELL 610,000 SHARES of J-com @ 1 YEN

# of J-com shares offered public on 8th Dec was only 14,580 shares which meant 44 times volume of the shares issued went for short sell.

The trade caused low limit of the day 572,000 yen from its opening 672,000 yen. 85 seconds later the operator's colleague realized the miss-input and tried to cancel the trade but large # of trades were already locked in. One of them who bought the sell order was no mercy Nikko City Securities.

8th Dec final trade.

Open 672,000 yen, High 772,000 yen, Low 572,000 yen, Close 772,000 yen. Volume 708,124 (for tiny 14,580 issued) ($3.5 billion worth of trade)

As of today 13th Dec, there are outstanding 96,236 shares unsettled 6.6 times of totally issued #, that Mizuho Security is unable to deliver. Today the stock commission have decided to force settle the trade at 912,000 yen as substitutes for delivery of shares. This will result in 40bil yen (= US$ 336 million) loss for Mizuho Securities in just a single trade.

Very unfortunate incident for the operator but knowing this can happen to any electronic traders (who are a little careless or tired), it reminds us spending extra time ensuring what we have entered for the trade is worth spending. (or may be nice old fashion of tel or e-mail trades might be better.)

Following is what I am doing now for trading.

12/12/2005

Pikers, by James Lackey

After a few years of reading Daily Speculations, I find a couple of things remarkable. One is the reaction to the dumb-bomb that Mr. E. drops on the young and the brilliant. They lash out like they never heard anyone call them stupid before. Pure emotion fires out from their pride.

Marcellus Wallace to Butch the Boxer, "Pulp Fiction":

The night of the fight, you may feel a slight sting. That's pride $@#%ing with you. Forget pride. Pride only hurts, it never helps. "You see, this profession is filled to the brim with unrealistic mothers. Mothers who thought their ass would age like wine. If you mean it turns to vinegar, it does. If you mean it gets better with age, it don't.

The second remarkable thing is how insecure traders are about their position size. Everyone wants to be bigger. That is as bad as those spam e-mails how to increase your size by taking a magic pill... Read the whole post

12/12/2005

Integrity: In Memory of My

Father, by Joe Hughes

12/12/2005

Beauty: In Memory of

My Mother (July 10, 1924-Dec. 12, 2004), by Laurel Kenner

12/12/2005

Jeff Rollert on Dollar Cost Averaging

Many planners find that getting each client to make a decision on when to invest requires too much communication time. Dollar averaging is a time management technique as it doesn't require large amounts of client contact time.

My greatest sources of alpha have come from watching what methods people use to leverage their time. Many techniques have outlasted their usefulness and leave a few breadcrumbs of profit as a result.

Jeff Sasmor adds:

Dollar-cost averaging is one of the investing parables that stockbrokers like to tell their clients. Others I have heard include:

I'm sure we all have our favorites.

12/12/2005

Islands, from Alston Mabry

I know a few people who rode the market down from March 2000, bailed out at the bottom, and have stayed "safe" in cash ever since. The triple whammy: catching the market ride down, missing the market ride back up and watching their cash seriously devalued against real estate.

The Sage was worried about his 'two islands' situation where eventually the industrious island owns the lazy island, but the Fed has quite strategically devalued the US$ so vigorously against real estate that the industrious islanders can't afford to buy our island any more than they could five years ago. No matter how many T-bonds they have!

12/12/2005

The Senator Writes from India

From the 12/9 Hindu Times, here in New Delhi (where there has been a Gargantuan bull market and P/E's are still low):

Siju Jose, perhaps the first Keralite to go through the routines of an American jail in occupied Iraq, is a free bird. And if his words are true he had a nice time in a Baghdad jail, in the custody of "highly courteous and concerned" U.S. soldiers... "The Americans cared for me, gave me the Bible and a rosary to pray... I was treated quite well."

You guys see this in any paper back home? I'll bet not.

12/12/2005

The Emperor's New Clothes, or How High Priests at Delphi Stay High, by

Jim Sogi

The market's slavish attention paid to the temple of the Fed is too obsequious. The market standstill before the oracular pronouncements and the panicked gyrations and stratospheric reactions on the announcement do not lend to a belief in market rationality. While the central bank carries weight and the governors are competent and serious people, they do not appear to have much if any more information than is available to the public, nor are they superior in intelligence or analysis to the market participants, nor does the announcement carry commensurate new information to justify the typical overreaction, nor do they directly control the longer end directly.

Fed day is one of those trigger points that give the market an excuse to break out of its normal routine. Remember Robert DeNiro in Taxi Driver when he is standing in the mirror, "You talking to me? You talking to me?" Well the normally well behaved market wants an excuse to cut loose and do the stuff it is normally too embarrassed to do. Some in the crowd that are just all wired up, especially with the tense build up all day before and even the day before. It's all so silly, but that is the landscape. Alice didn't have any choice in Wonderland. Dorothy had to go along with the Wizard in the Oz. Harry Potter has his world. So must we.

There is the "wait and see gang." There is the "wind up gang" and then the "itchy finger gang" and the "bait fish" that run and turn with the bait ball. The press calls it "knee jerk" which implies some sort of built in function. It seems to be the same itchy finger gang at first, and then when they are done, the crowd stampedes and surges on its own weight. Then there are the "predators" that follow or even herd the bait ball or the confused stragglers. One spear fishing technique is when approaching the fish, the fish sees you, panics, turns one way, then habitually turns the other, and as its turning back from the first turn, shoot it just as it turns - usually good for a dinner. Then again the last few meeting were followed by 40-100 point moves. All based on the turn of a few phrases, a few words. "Ignore that man behind the curtain! The great and powerful Oz has spoken!"

12/12/2005

Theater Review, from

Jeff Sasmor

Yesterday I went to see The Odd Couple starring Matthew Broderick and Nathan Lane after having bought the tickets last June. I have always been a fan of the film version, somewhat less so of the TV series, but if you can get tickets to the play it's definitely worth seeing. Lane makes a great Oscar Madison; Broderick uses a whiney voice and is good, but not great, as Felix Unger. But then that's my Tony Randall bias showing.

The theatre is one block away from Times Square. I don't ever recall seeing so many people in that area on a Sunday before. This time everyone was carrying jammed-full shopping bags. It was crowded!

12/11/2005

Thoughts on Why Today's Market is So Tough, by Scott Brooks

I was thinking of my senior year in college and playing poker. I paid for that entire year of school, bought some nice things, took a few fun short trips and still walked away with around $35,000 in my pocket. I did it all playing poker.

The thing that I learned when playing was to figure out who the good players at the table were and which players were not so good. I simply left the good players alone. We could sit there all night and try and take money from each other, but playing against other "players" was just too much work and not enough reward.

I concentrated on the two to four guys (or gals, I was an equal opportunity player) at the table who should not have been there. These were the people who were the "gamblers." I remember walking into a house to play poker, and all these guys would be sitting around the table. Every once in a while one of the hosts would walk in and say, "Larry, Notre Dame is up by three at the half," or "Bob, your horse placed at Fairmont," or some other such statement. That let me know that these guys were gamblers.

When I would sit down to play, my goal was to identify who I was taking money from that night (the gamblers) and who I was leaving alone (the players). One of my other goals was not to take too much money away from the gamblers. I wanted to take just enough money to keep them coming back. If you took too much, you scared them away for awhile, or maybe forever. If they were scared away, I would end up having nothing but other "players" to play against. And remember, I don't care how good a player you are, it is much more difficult to take money away from other "players" than it is from gamblers.

It was also important for me to make the gamblers feel good about losing to me. It was important that they win a nice hand now and then, but something that I found to be even more important, was to let them off the hook once in a while. For instance, if I knew I had the winning hand occasionally I would say something like, "Larry, I've got the nut hand" (translation, "I've got the winning hand"). Larry knew that when I said that I meant it. (You never wanted to be caught being a liar. It's OK to bluff, but not to lie) Larry would appreciate it when I did that, as it saved him throwing away good money for bad. What he didn't realize was that I was only trying to keep him in the game and keep him coming back so I could maximize my winnings.

I would like to submit a theory to the list as to why it is so hard to make money in the markets right now.

The reason is because the markets have scared away all the "gamblers." Everyone was making too much money in the '90s -- the gamblers, especially, were making too much money. The market corrected too much, thus scaring away the gamblers. They didn't mind playing when they were winning big, but they are emotional, illogical beings, and will run away like scared, confused rabbits when they lose big.

We need the gamblers. They are the ones that make it so easy for the rest of us to make money. We simply need to figure out where the gamblers are going, and then capitalize on their lemming-like moves." Gamblers move like a school of fish. It's just like watching synchronized swimming. Gamblers also move on emotion. Very little logic or thought goes into their decision-making process, and if there is any, it's usually very superficial. The market has scared away the gamblers.

The market also committed another terrible sin. It lied. It lied about the hand it was holding. How did it lie? It cooked the books. The balance sheets of Enron, WorldCom, Global Crossing and Adelphia were a pack of lies. And to top it off, the lies were confirmed by the likes of Arthur Andersen.

It was OK for the market to bluff the average investor (gambler); they could accept that as long the market threw them a bone now and again. The market does this by giving them an occasional good year or a good trade, and even lets them make a decent return over the long haul if they stick with it.

For instance, if you look at the return of the average mutual fund and then compare that to average return of average mutual fund shareholder you will see a serious disconnect. For instance, the average mutual fund may have had a 15% return in the '90s, but the average mutual fund investor only got around a 6% return (I'm just using those numbers for illustrative purposes. I don't recall what the real numbers were, but they were not that far off of my example). The average investor could live with that, because they had the occasional good year and they never really lost big in the process. The market lied and scared away the investors (gamblers) at the same time.

The people that make it easier for us to make money have left the market in droves. Those left in the market are players. It's hard to make money from players, no matter how good you are. I don't know who the best trader is, but I know it's not I. But I know that no matter who he is, he's going to have a much easier time making money against an average Joe than he is against me. I may not be as good as he, but I am certainly not the one you want to "play" against. We all need the average investor back. When the lemmings, the schools or fish, or those that live on emotion come back to the markets, then our jobs will all be a lot easier.

12/11/2005

A New Story from Bo Keely: "The Rails Sing, Eh?"

12/11/2005

One-Sided Volatility? from Alston Mabry

GOOG 409.20 GOOG Jan 08 560 Calls: 52.00 GOOG Jan 08 260 Puts : 16.00 Beta = -0.17Source: MSN Money

12/10/2005

Clustering Analysis and Financial Performance, by Victor Niederhoffer

In the course of studying the applicability of the use of clustering methods to financial markets, a field with several hundred thousand methodological and application papers, I came across an interesting line of studies applying qualitative clustering methods to determining companies' future financial performance from the content of their past quarterly reports.

The studies by Kloptchenko from Abo Akademi University take 10 years of annual reports and classify the companies into bad, neutral and good return on equity improvements in the next year. He then takes the words used in each of the three categories of annual reports and sees if there are differences between them in the three categories that the words appear in. He was able to come up with 60% accuracy versus 33% random after the data mining. Good words were admissible: approach, award, career, vary, wealth. Bad words were: burgeon, chance, collapse, complex. uncertain, undergo, unforeseeable.

For example, "discreet, stockholder, intelligent, profit, diverse, extraordinary, innovative and succeed "were positive in the positive class but negative in the negative predictive model. Similarly, "stress, cumulative, losses, unknown, doubt" have positive weight in the negative class predictive model and negative weights in the positive class predictive model.

By looking only at words that appeared a certain threshold of times, an improvement in accuracy was possible". The author in another paper has applied this work to analyzing future performance from past quarterly reports the author concludes: "Before a dramatic change occurs in company financial performance, we see a change in the written style of a financial report. If a company's position is worse during next quarter, the report of the current quarter gets more pessimistic, even though the actual financial performance remains the same."

There are so many variables, so many differences in company performance, so many implicit hypotheses, so much correlation and interaction of the content of the financial numbers with the future results, that with the small sample size of company years considered, possibly less than the number of hypotheses implicitly considered, it is a wonder the author didn't come up with 100% accuracy.. The results are completely useless for practical current work. However, the effort, the type of strategy employed, seems well worth improving upon by specinvestors.

12/10/2005

Sentimental Beta, from Dr.

Kim Zussman

Denys Glushkov constructs a pretty good sentiment measure from Investors Intelligence, CEF discount, IPO's, and dividend premium. He finds that stocks with high "sentiment beta" (smaller, more volatile, and with higher analyst coverage) have lower returns than those with low SB. High SB stocks grew in popularity with institutions in the 1990s (along with everything else). So much for loving your stocks.

12/09/2005

Will Goetzmann's History, by Victor Niederhoffer

Will Goetzmann is a Yale scholar (currently on leave for a year at Harvard Business School) who studies the history of markets. Some of the historical references and books on his Web page have timeless lessons. I particularly like the analysis of "The Perils of Wall Street Speculation" based on William Worthington Fowler's 1870 book Ten Years in Wall Street. Goetzmann reports the wary threat to stock market speculators with a link to the cartoon below the caption. This is similar to the Louis L'Amour story about the gold prospector who risks the whole mountain's falling on him with each blow of his axe that is memorialized in Practical Speculation by Susan Slyman's painting .

"Drive the plow and reap the grain, sail over the sea, sweep the streets even, chose any honest calling, no matter how arduous, anything but speculation. Even if endowed by nature with gifts and favored by fortune, and you rise to be one of the money kings, your name will then only go down among the gigantic but disreputable shadows which flit through the traditionary landscape of Wall Street."

Goetzmann comments, "Don't take the threat seriously. Our culture has always had a love-hate relationship with finance. The same people who depend upon professional investors for their future well being at the same time decry money managers for not doing real work. If you go into finance, you will have to live with this cultural duality."

I feel that quantification of the degree of acceptance of the sentiment that investing in the stock market is likely to end in disaster is one of the best indicators of future return. Whenever all my relatives call to ask whether they should get out of the market, and all my readers send me hate mail because the market went down and I said something bullish in the last few months, or whenever the academics write books or articles saying that one should disregard the returns of the 20th century reported by the Triumphal Trio and realize that there were periods when you actually could have lost money in the market, and they are imminent and relevant now, so get out, why then I know that it's even a better time than usual to reach for the canes.

Such fear can be quantified even more readily by runs of declines of parts of the day as suggested by Goetzmann's poignant non-quantitative take on "Three Days after Black Monday: The Crash of 1987."

After reading the erudite, sharp and practical historical vignettes and analyses of Goetzmann, including references to many of the books that only I have in my library, and learning that he is teaching, indeed heading an important center at Yale, I wondered we be so nearby yet not be in close contact. Then I realized that the lecture I gave at his class with Laurel and Liz Callaway, the article he wrote about my tally sticks, and the many times that he has been at my house for historical research must be augmented imminently.

Jim Sogi adds:

Look at some of the great company names from Dr. Goetzmann's NYSE data reflecting the technology of two centuries ago: rail, coal, canal. As Dr. Fitzsimmons described, the technology of the 1800s and the industrial revolution were more revolutionary and disruptive than current developments, and impacted life even more than current technological wonders. It is a primacy/recency phenomenon that gives us the illusion of the importance of recent inventions. You want some real out-of-sample data to crunch? You want revolutionary disruptive technology? Look to the 19th century:

Many prices above $100. If you had to settle trades in paper certificates, you would want as few positions as possible.

12/09/2005

A Risk-Free Rate Question, from Jason Schroeder

I look at the frequently offered definition of government bonds' being risk free and really wonder how that abstraction helps me evaluate other financial products.

Holding a government bond is akin to one young child's inviting another to his birthday:

What part of this kind of risk is supposedly free of risk? There is a difference between Zero and the Empty Set.

The introductory books begin just pricing a bond and proceed to the funkier functions of time and money which I am capable of analyzing.

What happens when I do not believe what I read? The functions make sense when justifying a payment schedule as a payer. But as a payee, I have questions about the symmetry.

12/09/2005

We Can't Disagree Forever, by Dr. Alex Castaldo

There is a result in Game Theory called the We Can't Disagree Forever Theorem. As a game is played, the players will learn about the situation by observing the other's move and eventually they will converge on a common understanding or as it is called 'common knowledge': every player knows certain things and knows that the other players know them. This is a difficult area of Game Theory.

John Allen Paulos gives a complicated and somewhat artificial example involving two investors who have partial and non-overlapping inside information about what is going on at a startup company. By observing whether or not the other has dumped their stock yet, they are able after a few steps to reconstruct the full inside information even though each only has half of it.

I believe it has no practical application, but is interesting conceptually: people in a market can figure out a certain number of things by watching the market reactions.

12/09/2005

Jim Sogi Goes Fishing

Three important pilot fish in the last two months:

12/08/2005

A New Collection of Stories from Bo Keely

12/08/2005

Our Monthly Buyback Update

12/08/2005

Iron, Steel and Trading, by Dr. Rod Fitzsimmons Frey

The industrial revolution holds fascination for me. The period was one of great inventiveness and entrepreneurial spirit, where a man could, by development of his hands and mind, create a fortune for himself and for the world.

Even more than that, the industrial revolution was a bootstrapping process. For thousands of years society had existed in a more-or-less technological stasis, give or take a Leonardo or two. As the revolution got underway, a new meme took hold: one of building on ideas; one of unsatisfied ambition; one of desire to progress combined with belief progress was possible. The result was a series of interlocking technical innovations that brought us from plowshare to space shuttle.

This great societal venture can serve as a macrocosm for the individual process of bootstrapping. There are many similarities between an individual trader's education and society's industrial launch. There is no roadmap for traders, no school program in how to make a living in the market, just as the early industrialists were in uncharted territory. Traders face a society that is uncomprehending of their daily tasks, and even hostile toward them; industrialists challenged aristocracy and peasantry both to accomplish their goals. Ignorance of the role of speculators approaches what industrialists faced in the Luddites and others. And most of all, trading is solitary: the only motivation comes from within, and strength to continue will not come from others.

I set out to reproduce the major steps of the industrial revolution. My goal is to create an internal combustion engine from scratch. (This goal is considerably less challenging than learning to trade). I initially made several false starts by trying to move too fast. I eventually returned to first principles, and once they were mastered, my progress has been smooth. The principles were:

With these two first principles understood, progress has been smooth: I've built a lathe, which can in turn build other machine tools, and the engine will become a reality.

So what are the first principles for somebody learning to trade? Two candidates that follow (and perhaps stretch beyond tolerance) my analogy are the economic cycle (energy), and probability theory (geometry). But the link from those fields to actual practice of trading is nowhere as clear as the link between charcoal and molten iron. What are some other candidates for "cornerstones" of market participation?

12/08/2005

Heart of a Champion, by

Jim Sogi

I compete for surf with the 20 and 30 year olds in the water everyday, and they don't cut me any slack, and neither do the waves. At 50+, I'm one of the few old guys still out there. My good friend Makalawena Bob surfs at 70. One of things that gave me the most inspiration was age bracket competition and I won the Island Grandmaster division, a local division. No big deal, but it felt just great! A lot of the swimmers do age bracket competition as do the triathletes. The old guys train hard, but still have a chance because the other guys the same age have the same limitations. The young guys give a little respect, not much, but some. They know they will be old one day too.

It's big wave season now, and your life depends on being in top shape. You can't go out in the 15-20 foot waves with big currents without wind, strength, flexibility, stamina and knowledge. In the bigger waves, age isn't such a handicap as it's not so much about speed, it's more about knowledge, strength, courage. It takes as much guts to drop into a big 20 footer as it does to enter and hold a big position at what seems the trickiest point. Fear is inversely proportionate to one's current level of strength, wind, flexibility, stamina and knowledge. Its good to be in top shape physically as it helps with trading. Both sports and trading can push one to the limits of courage and stamina, so they complement each other in many ways.

12/08/2005

Some Lessons From a Trading Story, by Victor Niederhoffer

When I was 11, I read a book that seemed good at the time on how to win at poker. The book recommended that you play only low hands because you could win either way with them, in hi-lo games, and that in hi limit games you should only play when your hand was the highest and best showing. I followed this advice and beat my neighbor who was a tenant in my grandmother's apartment out of his rent money which was $20 for the month. I heard his wife beat him up, screaming at him all the while, that he was a no-good gambler and had ruined their life. Shortly thereafter my grandmother told my father of what I had done and he demanded that I never play cards again with the tenant or anyone else for that matter as all gamblers die broke.

The first thing I learned from that is there is a tendency to lose everything when you gamble. And when I made $20 million on $100,000 in about six months in my first foray into commodity speculation in 1979, and then lost $15 million of it, I remembered the wife screaming at him next door. I stopped before I went under and have always tried to keep that lesson in mind since. It worked many times since that time but didn't in 1997 but that's another story. I hope I learned from that.

Someone else learned something from that also. It was the boy wonder, Shawn Andrews. He is in with all the big casino owners in Vegas and is invited to the celebratory dinners for the world champions of poker. When the conversation dies down, he tells my story and says "Vic's father says all gamblers die broke, and they're lucky if they don't end up as degenerates like all the system boys he had to carry to the morgue from the Bowery." At first there is great disbelief and disapproval. When no counterexamples are forthcoming, brooding ensues. The next day he invariably gets a few calls, and he has a few new customers.

I used this story at the recent fund-of-funds conference I spoke at. I told them they should pay me to speak at all their conferences because they could use me as an example of why diversification and vetting and the bear side were necessary. To emphasize the emotional content of the message in a way that mere words can't, I was accompanied by two outstanding musicians playing the piano and singing. My message was a great hit, and I was offered several jobs after the show by risk management firms. I like to make fun of myself because it keeps me humble and helps me to avoid the fate of my next door neighbor.

12/08/2005

A

Letter on Poker, the Markets and Finding Success, from Steven Leslie

12/08/2005

A

Story on Flat Tires and Loyalty, A

Story About Day Trading and On

Welding and Trading from Jim Lackey

12/08/2005

"Oops," from

George Zachar

JPM has a chart "showing" that it would take $800 billion in 5y10y swaption straddles to "hedge the vega" of outstanding mortgage backed securities. What does that mean? It means the optionality of the mortgage universe is at an all time high, and along with it, "oops risk."

12/08/2005

A Letter from

Don Boudreaux to The Christian Science Monitor

To the Editor:

Henry Kaufman and Thomas Johnson wisely support science education, but they go overboard when insisting that "America's economic well-being hinges on our pre-eminence in science and technology" ("Send Future U.S. Business Leaders Abroad", Dec. 8).

If a people's well-being depended upon their nation leading all others in science and technology, then only one nation in the world, at any time, would be prosperous. More importantly, economic freedom and free trade -- not science education -- are the ultimate keys to economic well-being. Economic freedom unleashes entrepreneurship while free trade allows people in technologically less-advanced countries to benefit from the knowledge and skills of people in technologically more-advanced countries.

Sincerely,

Donald J. Boudreaux

Chairman, Department of Economics

George Mason University

12/08/2005

Defeating Failure and Failing at Success, by Sushil Kedia

Ali is the movie from amongst innumerable ones on the battles of Cassius Clay. What stands out vividly is Clay's/Ali's overwhelming stamina and systematic obsession at defeating failure. The movie captivated me in its portrayal of his failure at handling the subsequent success as well. The movie handled the contrast remarkably but could have spared its lingering at the treatment of the twilight and the transitory phase.

The fine portrayal of how Ali fought with himself rather than the enemy, ruled the ring with his mind as apart from his footwork and punches, and beat all odds is here to see. The disintegration of a champion, the overtaking of emotions and the ultimate weakness of the achiever, is breathtakingly clear as well. I am preserving the copy I chanced upon a couple of years ago to hand over to my kids as they grow to the age where evaluating and understanding success and failure may be better facilitated with this digital story.

12/08/2005

Rabbit Huntin' and Trend Followers, by J. T. Holley

We got our first snow of the year in Richmond, VA yesterday early morn. It was a nice blanket though a little slushy. This for some reason got me thinking of going hunting with my Pa Pa for rabbit. This is something of a dying thing hunting for squirrel and rabbit. The hunting seasons of other game are short now that when you do go into the woods you aren't going to waste your time looking for either of the aforementioned. You don't really plan to go rabbit hunting either. It is something that you just get accustomed to after it snows.

Rabbit hunting is something when I think about it very similar to trying to find trend followers in data. They leave footprints in the snow. They tend to be active in the morning and late in the afternoons most of the time except if it is dreaded cold then they come out in the middle of the day. A good place to find a rabbit in the snow is on the Southern side of a hill like finding a trend follower on the other side of a 10 day or 20 day moving average. Like trend followers placing stops, rabbits when chased out of a burrow seem to come back as if in full circle. That circle or burrow is the average where you can shoot a trend follower too. Rabbits like trend followers don't move much and maintain their positions and when scattered usually return to the point of anxiety, easy prey. The shot of choice is a 20 gauge because they are thinned skinned and easy to kill, much like getting a trendy out of a position!

Rabbits for those who haven't tasted them are nothing like chicken. You gut them in three parts: front legs, saddle, back legs. Place these in salt water over night then rub butter and breadcrumbs then fry like chicken, but it doesn't taste like chicken! Mess of greens and caramelized carrots are good sides, no puns intended.

Don't know what a trend follower taste like?

After growing up huntin' rabbit and squirrel it makes watching ole' Elmer Fudd more of a comedy. You know that it is the foil opposite in real life between the human and the rabbit. For a young man coming of age rabbit hunting is one of the first introductions to the sport of hunting, maybe for counting purposes hunting trend followers and taking profits from them oughtta be the first exercise?

Remember don't shoot just for fun, respect the game for what it is: nourishment. Equally respect trend followers for what they are: potential profits.

12/07/2005

In Pursuit of the Initiative, from

GM Nigel Davies

I'm not sure how it is for other GMs, but whenever I stretch my position to pursue the initiative I'm painfully aware of the holes I might be leaving in my ranks and the strain put on supply lines. Lasker advised that the attack should be in proportion to the amount of advantage you have, but applying this tenet in practice is fraught with difficulty. First off it can be very difficult to know how much advantage is there, and many games are lost because players overestimate their chances and play far too much aggression for their position to reasonably tolerate.

Despite my thirty years of competitive chess I can't say I've found an all-embracing solution to these issues. If you play it safe your opponent is under less pressure whilst if you go for the jugular it can rebound. Perhaps the bottom line lies in the kind of tournaments in which someone competes; bold play leads to more ups and downs which are good for Swiss tournaments (many players, few prizes) but less effective in round robin event and matches. But any change in style must also be within one's comfort zone.

12/07/2005

Inefficient Markets, by Prof. Gordon Haave

Different markets are inefficient for different reasons. Usually, I conclude that the reason for a market inefficiency is that people do not conform to the theoretical ideal of their being rational consumers.

As someone who enjoys putting thoughts to paper, on my mind this morning is why the market for financial commentary is so inefficient. By inefficient, I mean that bad ideas and writers are seemingly not weeded out over time in favor of good ideas and writers.

A piece of market commentary necessarily contains two components. The first is the ideas being conveyed in the commentary, the second is the style of the commentary. My comments relate primary to bad ideas being conveyed in financial commentary, which right off the bat suggests that financial commentary consumers might value the style of commentary much greater than they do the correctness of the ideas being conveyed.

Now, there is always going to be vast disagreement in the financial community over certain ideas, so I am not going to use this space discussing growth vs. value investing, the true value added by hedge funds, or whether or not there is a real-estate bubble.

Let's use my own situation as an example: I live in northwest Oklahoma City. The area is booming. Just three years ago much of the land around my neighborhood was farmland, and now the developers are building thousands of homes. The schools are good, and northwest Oklahoma City is the easiest direction for future economic growth (due largely to oil prices) to expand to, as the west is bordered by Midwest City, the South by Moore and Norman, the West by Yukon, and the North by Edmond.

Real estate in my neighborhood is hot. I am going to create investment interests in my house, and you should buy one. The cost? Only $3,500 per Haave housing unit. It does not matter how many investment interests I am selling, how large my house is, or what condition it is in.

Who here wants to buy an investment unit in my house?

Why is it that every day the vast majority of investment recommendations (outside of technical investment recommendations) mention the quality of an investment that you should buy without mentioning the price of the investment?

Possibilities as to why the investment commentary industry does not weed out bad idea/authors:

Dr. Phil McDonnell replies:

What this apparently assumes is a definition of efficient writers as being able to predict the market better than their peers. If we accept the premise that most markets are reasonably efficient and by definition unpredictable, then it is only reasonable that financial journalists as a group would have no better track record than random guessing.

However I think Prof. Haave's point is that the type of logic employed by many financial journalists is inadequate. In a sense I agree. I would always prefer as much information as is reasonable, including the usual financial ratios with respect to price. However I also know the most popular ratios often do not work or even operate in a manner contrary to what is popularly supposed. For more on this see the discussion of the P/E ratio fallacy in Practical Speculation.

Naturally this leads us back to the random walk. The latest price includes the value of all previously known information. Then the usefulness of a media piece comes down to the novelty of the ideas presented therein. As a reader I look for ideas which I have not seen before and those which represent new trends or information. To the extent that a given media piece does not have new information then I would have to agree with Prof. Haave's underlying point: it is just more random noise on the financial landscape.

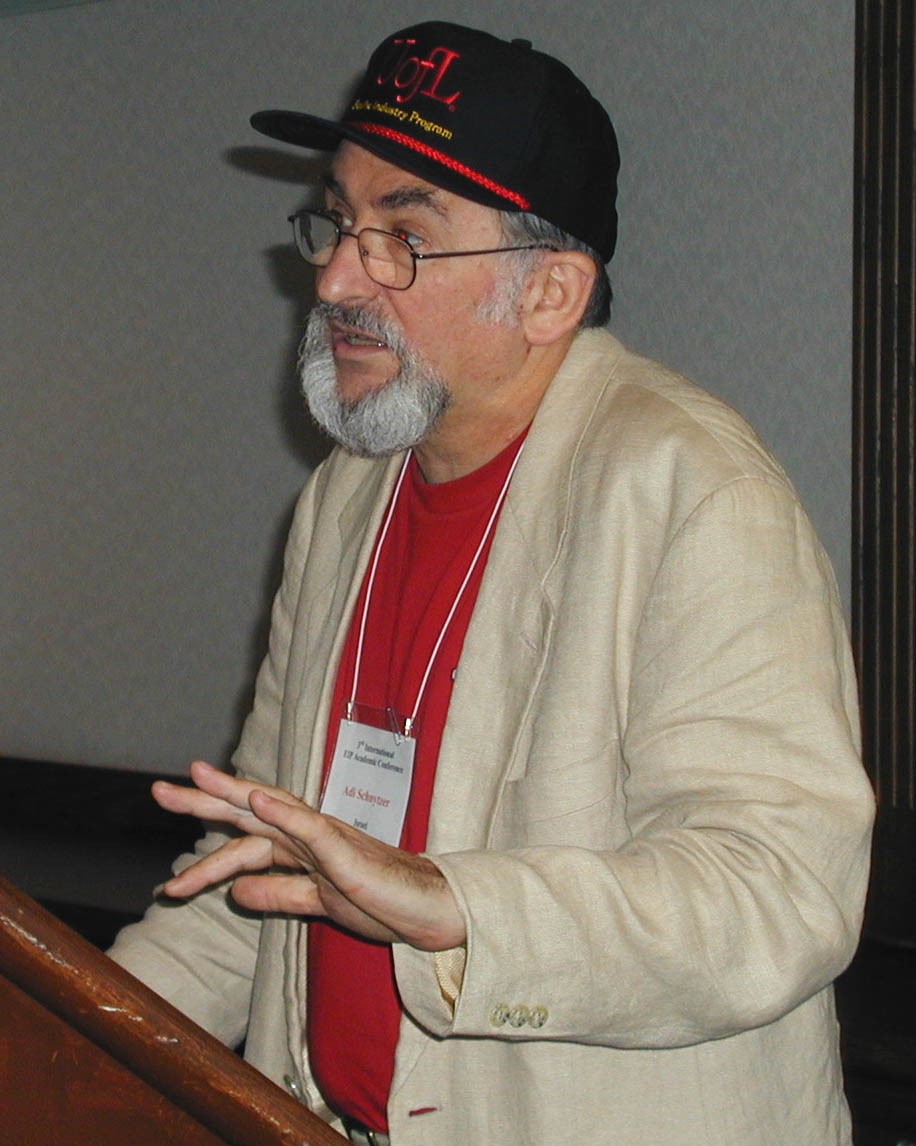

Prof. Adi Schnytzer responds:

If you are spending 80 hours a week trying to find non-random inefficiencies, why stick to a silly textbook definition of inefficiency? I would define a market as inefficient if I am able, any which way, to regularly get a greater return than the risk-free rate of interest, plus something for the risk, assuming I'm risk-averse. We know that inside information allows such profitability so that part of your search is implicitly for signs that insiders inadvertently provide when they trade illegally. Then there are the frictional inefficiencies that may or may not exist to an extent sufficient for exploitation. Finally, there is the obvious and unquestionable myopic nature of the market. Every time oil changes direction, the market goes nuts. Likewise, when a large firm produces exceptional news, either good or bad, or when something unusual happens in the world arena.

Can this be used to make money? Sure, if you know how to predict where oil prices, the US economy, the world economy, and I guess the world in general, will be in six months' time. So we are talking about information gathering (easy today) and processing (never easy). Why define inefficiency at all?

12/07/2005

They Held Tightly to the Things They Knew Best, by Victor Niederhoffer

*See below -- Letter from the President of the Old Speculators' Club Defending Old Ways

Never at a loss for a reason to be bearish, the chronics are clinging to their old ways and coming up with one reason after another to be bearish. The main themes these days appear to be that the yield curve is close to inverting, the pension fund liabilities are becoming increasingly ruinous, the earnings growth is going to be much worse next year, the bull market has gone on longer than its norm, (or the bear market is confirmed by the absence of a break through of the 2000 high), and consumer debt is going to cause a recession. As the Sage says, "We do not think the general ownership of equities is going to be very exciting over the next 10 to 15 years."

Now the usual model to analyze those in denial of a failed prophecy is the Keech cult studied by Leon Festinger. Like the chronics, they predicted the end of the world. And when it didn't come, that only confirmed their belief that they were right. Festinger reported five conditions necessary for such a confirmation:

Okay, now the bears:

Yes, but there's a better analysis of it, a better reflection of it all. And as usual it's by a woman of deep insight, one of the greatest observers of human nature in our day, Margaret Mitchell in Gone With the Wind, a book well worth reading as one of the greatest historical novels ever written, rivaling some of the best by Patrick O' Brian.

Something had gone out of them, out of their world. Five years ago, a feeling of security had wrapped them all around so gently they were not even aware of it. In its shelter (Nasdaq 1000) they had flowered. Now it was gone and with it had gone the old thrill, the old sense of something delightful and exciting just around the corner (Dow 5000), the old glamour of their way of living... Their faces were little changed and their manners not at all but it seemed to Scarlett that these two things were all that remained of her old friends. An ageless dignity, a timeless gallantry still clung about them and would cling until they died but they would carry undying bitterness to their graves, a bitterness too deep for words. They were crushed and helpless, citizens of conquered provinces. Everything in their old world had changed but the old forms. The old usages went on, must go on, for the forms were all that were left to them (the prices are not sticking to the moving averages). They were holding tightly to the things they knew best and loved best in the old days, the leisured manners, the courtesy... the traditions in which they had been reared. They had nursed the wounded, closed dying eyes, suffered war and fire and devastation, known terror and flight, and starvation.

Now if that doesn't express it perfectly, I'll eat crow.

Pamela Humbert responds:

I think it's the aging of the baby boomers (I blame all bad things on them). They are suffering from the realization that:

While there is no way of testing my theory, it doesn't seem implausible that the bearish meme in the face of otherwise good things is about so many people facing menopause, middle age crises, ennui, and fear of death all at the same time. In my opinion Bill Cl#nton's heart condition had a bigger impact on peoples' outlook than 9/11.

P.S. I'd like to avoid an influx of emails from 55+ year olds telling me that their s#x life is better than it was when they were 30. And for seniors who feel obliged to share the details of their amazing s#x lives -- don't. It may be great now but the reality is that you'd pay $1 million, if not more, to be 30 again. Viagra does only so much for the experience.

A Letter from the President of the Old Speculators' Club Defending the Old Ways

Wrong, wrong, wrong.

First, you dabble in fiction: "S#x not as good when you're 55+..." There is no s#x after 55.

Death is further away, not closer. See Ray Kurzweil's The Singularity is Near. Of course, life is not a straight line up. There are too many delightful back alley diversions to even want to adhere to a straight line.

And you know what's left after the kids are out of college?

Nothing! We're absolutely flat, stone broke, in debt, and with ever diminishing prospects. Whatever cash assets we had went up the chimney when we clung to the promises of the chronic bulls and held onto our tech shares after the turn of the new millennium. And now that Kurzweil tells us immortality is on the horizon, we learn we'll have to work forever. Of course, if we had put our money back into the market we would have regained chunks of what was lost. But we are a generation that despises risk. We embrace security and a market that always trends up and a guaranteed comfortable retirement.

Victor wishes us to cast our few remaining shekels into a market that could once again turn into a bonfire. Some of us have done so, but only because we always watch CNBC, "where never is heard a discouraging word." I would love to read the thoughts of the weekend permabear, but I can't afford it. Most of my free cash goes toward purchasing necessities -- thank G-d for low inflation. I used to think I was spending substantially more for food than the government was stipulating. However, once I recalculated my expenditures properly, I learned I had created a straw man. By merely placing meat, fruits, and vegetables in a "highly volatile" category, I discovered my core expenditures were, indeed, almost unchanged. I just don't have much cash - nor do most of my peers -- and that's why we're cranky.

Why the Chair rants about the chronic bear, the Palindrome, the Sage and others I'll never figure out. Just who does he think is constructing that "wall of worry" that must be climbed? You certainly won't find many contributing builders on Daily Speculations - although they might be quite able to construct a temple to Pangloss. Another item I pass over at the grocery store, which the Chair never foregoes, is the Enquirer. You ask, Why? Well, other than the unnecessary expense, the Enquirer is permanently bearish on people! Admittedly, the celebrities and other worthies who fill its pages may not be the world's finest human beings; but isn't it just a touch vindictive to watch them suffer - and suffer again and again week after week. Appears old-hearted to me.

So forget about laying the blame off on menopause or ennui. We can tolerate things like that as long as we have a gated community, a good tee-off time, no slovenly neighbors, a convenient Nordstrom's, and good Chinese carryout. But the government won't give that to us. So the market offers our only opportunity. But, forgive us, we're scared to death especially with the resurrection of Goldilocks and "don't worry, be happy."

We've been down that road and were lucky to get out with loose change. You see, unlike Mitchell's fictional characters, we never possessed fine manners or experienced a flowering. We went straight to seed in the late 60s and early 70s when 420 was cheap, s#x was free, and the only thing exciting around the corner was the draft board office, which we torched regularly. We spit on our wounded, cheered their deaths, and were indifferent to the fire and devastation that the victors visited on our former allies. Gimme Shelter was more than another Stones triumph; musically and cinematically it became our blueprint for life. And we feel betrayed.

James Sogi avers:

One of the sad problems is the lack of respect for age, the elderly and their wisdom. There is a pernicious cult of youth. The Hawaiians revere and respect their kupuna (elders) for their wisdom and knowledge (mana'o). Slavish worship of beauty and wealth and their mimicry is a parody that causes dissonance. It is an misguided offshoot of commercialism.

The are many benefits that come with age and wisdom.... independence, a level of comfort, freedom from many youthful anxieties and self destructive urges. Health can and should be pursued at any age as the top priority.

Part of the answer is to keep moving and active. Check out Surf for Life, it's a movie about old surfers 93, 84, 70 still surfing, still stoked on life. Health: it's worth a million bucks.

J. T. Holley rebels:

Well not exactly my friend. Great book and somewhat good metaphor, but please may I beg of you not to have the Ableprechtuffets compared to my beloved South. Much of the Civil War history is untrue. Like most history it is written by the victor. The Bulls continue to write the economic history of our land and this is based on empirical fact, but the South didn't send its men to War over an issue that affected only 6% of the population, such absurdity is readily made available in text. The deception is there. There was no Union Army fighting for the sake of ending slavery nor was there a Southern Rebel Force fighting to preserve it. After the South declared its independence the Union forcefully invaded, leaving the South no choice but to defend themselves. The South obviously surrendered and gave way to Progress and Industrialization.

Some would say that the South has become an economic colony of the North used and exploited like Colonies around the World. That might be a little metaphoric to the Bull vs. Bear struggle but it ain't similar at all in the characters and integrities of whom make up the fight? The only similarity is that progress and change are shared in the story and plotline for the sake of economic advancement. The South like the Bears just don't like change! The South at least eventually embraced and is continuing to change, albeit slowly. Chivalry, dignity, respect, individual liberties, and gallantry are what Mrs. Mitchell wrote were Scarlett's feelings and reflections.

Now Vic, not one of those characters in the Bear Camp possess any of those traits? They have had their brains good and scrubbed to seek total destruction and eventual devastation so that they can say "I told you so", do you think General Lee would have even thought such? Sure Buffets words sound sympathetic, certainly not empathetic, but would you think for one minute he would nurse the wounded or close dying eyes?

Kim Zussman adds:

Perhaps in addition to boomer aging, we should consider how much trading is now controlled by 30ish physicists and engineers at quant funds with horizons similar to particles from colliders.

It's hard to understand how, if trading/investing is approximately zero-sum, everyone can be rich. But of course this is neither the message of libertarianism nor statistics. For there to be rich there must be poor. To be rich you need to be smart or lucky, and usually both. The non-random element after the dice are thrown is intelligence, or persistence at learning, and it is available here and now.

Here in sunny Westlake Village, there are plentiful queues at tee-time, chock-a-block McMansions, and too many Timmys toning at tony healthclubs. And it is surprising how many are on anti-depressants in the face of such plenty. Maybe it has less to do with absolute possessions than potentials, and the defining moment of age-related depression is the abandonment of hope for a better future.

Dr. Rod Fitzsimmons Frey offers:

When I was helping to distribute investors' money to the community by hiring programmers, I had a decided bias in favour of university graduates over technical college grads. Not because one was smarter or more ambitious: rather, it seemed the probability of a university grad's understanding of the importance of "why" versus "how" was higher. (The probability was still quite low, I note.)

The preference of "how" over "why" seems to be genetically encoded in us. It's easy to see why: in a Hobbesian world of the quick and the dead, they "hows" are well fed and surrounded by little how-asking bambinos long after the "whys" have been eaten by sabre-tooth tigers.

Like so many traits useful in the jungle, our how-bias is no longer serving us quite so well. Big Macs are so abundant that our jungle-born urge to store them on our midriffs has become injurious. Likewise, prosperity is so abundant that serious attention to the "how" is all that is needed to attain the starter castle and matching Hummer.

But in attainment, as in all other endeavors, success goes to the "why" askers. Those who know why they want material prosperity are likely to harvest no end of good from it. Those who attend only to the how will meet with disappointment and despair. This is not a revolutionary point: it is repeated over and over by all great religions, all lasting philosophies, and all wise uncles at weddings. Yet by-and-large most people miss it. I'm personally inclined to forgive them: "why" is very hard.

I know my own "why" for chasing prosperity. I'm turning to y'all for the "how".

A Ribald Spec adds:

"There is no sex after 55"... miles per hour! Any faster, and you really do need to concentrate on driving.

From an Anonymous Contributor:

Margaret Mitchell would be proud.

For the poetry version, it's time to chase down a copy of Joni Mitchell's "Hissing of Summer Lawns" album [which I consider her best work, ever], which has this fine track in it. Grafting in the trading analogies is a straightforward exercise.

Joni Mitchell, Shades of Scarlett Conquering lyrics:

Out of the fire like Catholic saints

Comes Scarlett and her deep complaint

Mimicking tenderness she sees

In sentimental movies

A celluloid rider comes to town

Cinematic lovers sway

Plantations and sweeping ballroom gowns

Take her breath away

Out in the wind in crinolines

Chasing the ghosts of Gable and Flynn

Through stand-in boys and extra players

Magnolias hopeful in her auburn hair

She comes from a school of southern charm

She likes to have things her way

Any man in the world holding out his arm

Would soon be made to pay

Friends have told her not so proud

Neighbors trying to sleep and yelling not so loud

Lovers in anger Block of Ice

Harder and harder just to be nice

Given in the night to dark dreams

From the dark things she feels

She covers her eyes in the X-rated scenes

Running from the reels

Beauty and madness to be praised

'Cause it is not easy to be brave

To walk around in so much need

To carry the weight of all that greed

Dressed in stolen clothes she stands

Cast iron and frail

With her impossibly gentle hands

And her blood-red fingernails

Out of the fire and still smoldering

She says A woman must have everything

Shades of Scarlett Conquering

She says A woman must have everything

(repeated refrain) A woman must have everything

12/07/2005

Low Tax States and Stock Performance, from

Dr. Alex Castaldo

Performance of stock indexes for 6 low-tax states since 1999:

SPX

Start StartDate Cur CurDate PrcChg PrcChg

Arizona 229.94 12/31/1999 514.94 12/05/2005 123.95% -13.90%

Nevada Not available

North Carolina 100 1/02/2002 125.70 12/05/2005 25.70% 9.56%

South Carolina 100 12/31/2001 148.33 12/05/2005 48.33% 10.19%

Florida 100 12/31/1999 131.82 12/05/2005 31.82% -13.90%

Texas 178.89 12/31/1999 347.52 12/05/2005 94.26% -13.90%

All five available indices have substantially outperformed the S&P.

Data: We used stock indexes provided by Bloomberg that track the performance of each state. The companies are headquartered in the state (or have a substantial portion of their operations there) and have a minimum market cap of $15 million. We used 12/31/1999 as a start date or the first date the index is available. The indexes include from 45 to 400 companies and are price-weighted indexes.

12/07/2005

A Perspicacious Spec Reads the Newspaper, a Continuing Feature

Quadriga's Baha Comments on Performance Outlook for Main Funds

Dec. 7 (Bloomberg) -- Christian Baha, chief executive of the Quadriga Investment Group which has $1.6 billion under management, comments on the outlook for the performance of the company's main funds and assets under management. He made the remarks in German in a television interview scheduled to be broadcast tomorrow.

On the performance outlook: ``For 2006 we are expecting 20 percent to 30 percent growth for our three main funds. That's the long-term average. With the more aggressive Superfund C statistically we could even see up to 40 percent growth, especially because this year wasn't that great. ``I'm not worried about a negative year, it's a good time to start buying.''

On funds under management: ``These will rise to about $2 billion to $2.5 billion, with a bigger part coming from our performance -- $400 million to $500 million -- and the rest from new clients.''

When Rastfarianism was in vogue, I remember reading about studies of people who smoked every day, a lot. They lost the ability to discern the difference between reality and their dreams, and developed a religious belief system that included the notion that dreams and reality were not all that different.

12/07/2005

A Methodological and Romantic Note from the

Assistant Webmaster

"How do you combine the large number of contracts traded for a particular futures market into one series?" is a hearty perennial. I think 'best practice' is to save two series: 'raw' prices, simply concatenated, one contract after another, and 'adjusted' prices, with all the data till contract i back-adjusted, difference-wise, by the rollover amount from contract i to contract i+1. The 'adjusted' series preserves correct point-wise/dollar-wise changes, and to get correct %age changes, you can use 'change in adjusted' as the numerator, and 'raw' as the denominator.

The question of when to roll from contract i to contract i+1 is complex; Prof. Corso (who runs APL on his cellphone) has written about this. It doesn't matter much for financial futures but can be important in energy/metals/ags/softs.

An alternative is to keep just the 'adjusted' data, along with the rollover dates and amounts in a 'footnote' database, to be used when/if %age changes need to be calculated. This takes up less space than two full series, but is harder on the brain.

The splicing of futures contracts is usually handled automatically by the many vendors of realtime and/or historical market data, typically with many methodologies (including several that are "wrong") for contract rollover offered as user choices. E.g., on Bl##mberg: PDF(Go) 2 (Go) 13 (Go) brings up:

Generic Futures Rollover: Roll Include Serial

Type Day(s) Month(s) Adjust? Futures?

Price : B 0 0 N N

Individual share data are another issue entirely. "Fixing" splits/spinoffs/dividends is straightforward, but the big problem is finding survivorship-free universe information "as of" a date in the past. The realtime vendors, (including Bl##mberg), are unsatisfactory as "research" databases for this reason.

Prof. Miller points out that his peers don't worry about such things, but instead assume the existence of clean, accurate data. I'd suggest this is because the "plumbing" work is handled by the grad students under their tutelage (the students insufficiently comely to serve as romantic prospects, that is).

12/07/2005

John Lamberg contributes to the Dept. of Scientific Breakthrough

It sounds like science fiction: a brain nurtured in a Petri dish learns to pilot a fighter plane as scientists develop a new breed of "living" computer. But in groundbreaking experiments in a Florida laboratory that is exactly what is happening.

12/06/2005

Diffusion of Innovations, by Victor Niederhoffer

The diffusion of ideas, markets, industries and companies that involve innovations is one of the most fruitful areas for the spec-investor to study. The approach should start with a good book on methodology and in this context I have found the 86 page book Models for Innovation Diffusion by Vijay Mahajan and Robert Peterson very helpful. Another outstanding resource is the website of Roger Clarke, devoted to all manner of research on how technology, ideas, artifacts, and techniques "migrate from creation to use."

The basic model is drawn from the spread of epidemics. A germ or idea is unleashed. Its diffusion is related to the number of susceptibles (S) in the population. But this number keeps getting smaller as the number exposed accumulates through time.

N(t+1) - N(t) = A + B ( S - N(t) ), where N(t) = cumulative number infected at time t.

The above equation is a good difference equation model of the process that leads to many insights for the non-random diffusions. A basic part of all such theoretical and empirical models in innovation diffusion (ID) is the familiar S-shaped curve with growth starting out slowly, speeding up at the ~20% of susceptible point and then leveling off at ~50%, with usually a symmetric descent to a 0% growth rate as the number of unexposed susceptibles approaches zero.

Preliminary study of the subject reveals a gold mine of applications with applications to predicting the whole stock market, industry rotation and impact studies of patent and research spending jumping right off the Googled pages on the subject. More generally, every day in the market there is some idea that seems to have the mojo. The idea gets adopted with a slow or fast start and then it either levels, explodes or recedes. Where does the pitch in the pinch come in?

Such thoughts revolve and enliven the creative process while sleeping and trading but are still very preliminary and I call on my readers for insights and lines of approach in this area.

The number of shares held per shareholder, or shareholding density, might be an interesting variable to evaluate the idea diffusion of owning a stock. High density would be visible in either low floating stock companies or those that have a universal or near bearish outlook consensus. Similarly a low density of shares per share-holder would be a case visible in large floating stock companies, or where a universal or near bullish outlook consensus exists.

Low and High density are descriptive terms. Maybe a beginning point is a study that evaluates a correlation between shareholder density, (over a reporting period), and returns over the same period.

If meaningful correlations are found on certain stocks then this indicator can be exploited further, even if leading to dangers of curve-fitting by identifying shareholder density ranges that have turned out to be bullish and bearish consensus territories. Instead of using these ranges as a trigger to trade or invest, it might be useful to have these at the back of the mind as the coming change in bias.

Alternatively, and possibly for the better, one could study the same data-sets to identify between what levels of share-holder density the most rapid move in prices happened, such that those levels would roughly correspond to 20%-50% of the idea stage. That would take care of blocked shareholding such as owned by managements or investment managers who never knew how to sell.

Two other similar variables of study on this paradigm could be defined as:

The beauty of the approach of diffusion of innovations appears to be the S curve that encapsulates roughly the 20% to 50% of the susceptible population.

The equation in a single expression harbors the aspirations of the trendists as well the contrarians. Turn either S or Sum of N(t) to zero and you have contrarians lapping up the situation while the trendists' endeavor remains to ride the 20% to 50% range of susceptibility.

12/06/2005

Letter of the Month Award

The material on this website is provided free by us, and by our colleagues, friends and readers. Because incentives work, each month we reward the best contribution or letter to the editor with $1,000 to encourage good thinking about the markets and augment the mutual benefits of participating in the Daily Speculations forum. Prizes are awarded at the end of each month by the Chair and the Collab.

November's winner is Exploring Fama-French in R: Visualizing the Difference between Traditional CAPM and the Fama French Three-Factor Model in Estimating Cost of Capital, by an Objectivist researcher who requests anonymity, Nov. 23.

12/06/2005

Crazy People, by Nigel Davies

It's a mistake to assume that crazy people are absolutely wrong about everything. Often they've got some great ideas but are missing balance and perspective. And they're always more interesting than sane people.

As for a crazy person with perspective, then you have genius.

12/06/2005

An anonymous contribution to Bear Corner

Credit Card Minimum Payments Set to Double Beginning January 1, 2006 Monday December 5, 4:15 pm ET

San Diego, December 5th: , from PR Newswire. City Mortgage Services, a California-based independent brokerage offering a full variety of mortgage products to the public, today announced that recent changes in credit card payment regulations could drastically affect consumer budgets, making it impossible for some families to keep up with increased minimum payment requirements.

Credit card companies will be increasing minimum payments right after the holiday as a result of new credit card lending guidelines set by the Board of Governors of the Federal Reserve System, Federal Deposit Insurance Corporation, Office of the Comptroller of the Currency, and Office of Thrift Supervision. This new guideline, which should potentially double minimum credit card payments, could drastically affect many household budgets.

"It's easy for people to sign their life away on credit cards but there's a price to pay at the end when the bill comes," said Don Marginson, President of City Mortgage. "For many that price is going up. In the past, most credit card companies required a minimum payment of 2.5 percent of the balance. The new regulation requires that amount to double. For example, if you have revolving credit card debt and the current monthly payments are approximately $300/$400 per month on a $15,000 debt you're soon to be looking at a payment of $600 to $800 per month. As a result, credit card and mortgage payment delinquencies are on the rise and going up daily. I am advising my clients, and indeed, all consumers, to act now to reduce their outstanding debt before this new regulation affects their credit standing."

Bank of America and MBNA have already raised their minimum payments, and Capital One is currently sending out their notices. Most companies will follow suit beginning this January. "This is going to cause people to take a look for alternative ways to get out from under their credit card debt," said Marginson. "One solution is to think about refinancing their home loan or perhaps arranging a line of credit, and paying off their credit cards and getting back on track with their finances."

12/06/2005

Do Rates Matter? Doubtful, from

Prof. Mark McNabb

While the body of research on rates has found extensive and exhaustive evidence of trends, economic impacts, etc there are numerous 'exceptions' to the rules.

For the non-debt traders:

Why care if the yield curve inverts, if the consumer is still financed at 5-7%?

GMAC still at 5%.

Why care if capital returns 8% or more in SE Asia?

Why bother if your trade horizon is intraday?

Why bother if your industry group grows at 15% and has low or lagged correlation

to the spread?

Why bother if energy replacement occurs at an increasing price curve?

It does permit Mr. E. to tantalize the weaker with the prospect of the

grail....

Most of the rate relations are built on 25 year old externalities and outliers that will not matter one bit to the semiconductor group in the next 2 quarters as they outperform, or to consumer driven data storage and video gamers with demographics independent of crusty old men wearing green eyeshades.

If one wants to look at credit factors and the market as an investor, (not a trader), look at its availability to industry not its cost when it is historically low. The new Fed governor little B is a non-factor unless the Fed reasserts its role in bank supervision. For example, if the yield curve inverts in 2006 and the long end remains cheap, the real estate game continues. The real banker in this economy should look at the musical chairs director in the Japanese-Hong Kong-Sino finance game.

A greater challenge in the future for dual-homeowning yuppies will be to whom and at what price do they unload the second home, when factors such as the ease of credit, (as opposed to price), don't support growth. Look at families in Midwest that hold on to the house of every dead relative and rent them for less now than a year ago, as populations dwindle. Families end up with several unwanted wasting assets, (even if owned outright), in that economic environment vs. seeing real estate double and rents increase along the coasts. Take away the availability of credit and willing buyers, the coasts will go to the plains.

Rudolf Hauser adds

There is little question that, as mortgage finance depends less on depository institutions that borrow short and lend long, the prospect of a yield curve inversion does less to impede mortgage financing. The crucial question should be of expectations as to future long-term rates. Why would anyone want to lend long if short-term rates were higher unless they expected long-term rates to decline in the future to a level equal or below that of current short-term rates, other than to the degree necessary to hedge their assumptions given the odds that they could be incorrect in that forecast of flat to rising long-term rates. After all, the sensible case would be to invest short until rates decline and then switch over to the longer-term instruments. As to yield curve interpretations see my earlier posts on this subject of some weeks ago.

12/06/2005

Football and Speculation, from James Fee

Among our friends there may be an aversion to the writings of Michael Lewis, who irresponsibly penned an awful review of EdSpec years ago. However, here he writes exceedingly well about a deeper understanding of sports, which can be applied to diverse other fields.

Victor Niederhoffer muses:

This offense at all times approach is a very interesting discussion point for specs. How to mix up the offense without suffering ruin? The optimum amount of leverage? Three times leverage for S&P futures?

Will Huggins adds: